Delcath Systems (NASDAQ:DCTH) announced that the FDA approved its HEPZATO Kit device as a treatment for a type of liver-dominant eye cancer. The stock shot up to over $7.00 in early afternoon trading on Tuesday as the device is expected to be launched by the end of the year. Fellow Seeking Alpha contributor TripleGate astutely called the FDA approval a few days ago, and is likely rolling in substantial and immediate profits thanks to it. While the assessment of the probability of FDA approval was well covered, one thing that the author did not account for or discuss was existing and coming dilution.

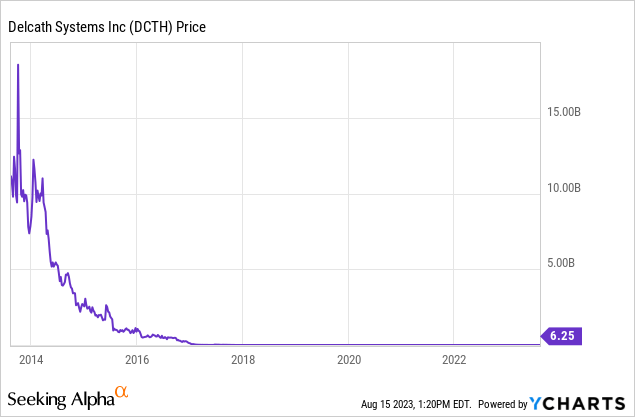

DCTH has had a history of disgracefully poor financial performance from years of dilutive financings and reverse splits. A common term for a stock with this level of toxic dilution is a “dilution scam”. TripleGate mentioned that the stock suffered for a decade from a lack of investor interest. But with charts like this, can you blame investors?

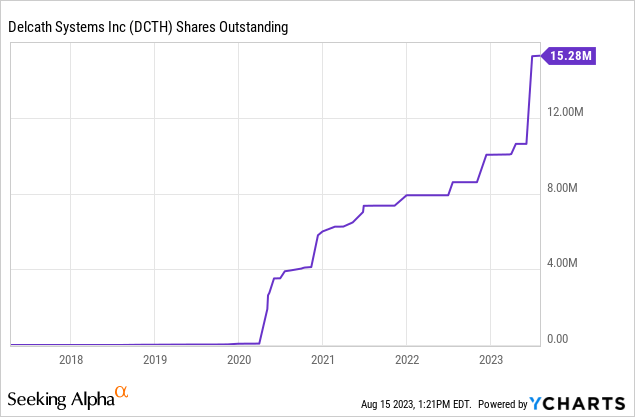

The stock has gone from a reverse split-adjusted price of billions to less than $10, essentially a 100% loss for anyone who bought and held for more than seven years. The share count has gone from near-zero to 15 million during that same time. I come from the school of thought that a leopard can’t change its spots. When I see history like this, I am very critical of the long term viability of the stock price, even if the company has achieved a significant milestone such as FDA approval.

TripleGate mentioned:

DCTH could easily be worth $10+, a modest multiple even to a mere $100m/rev peak sales number.

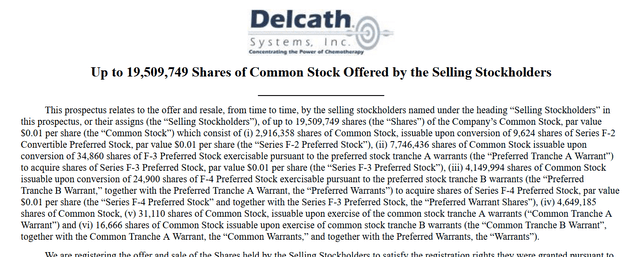

Which implies that they are using shares outstanding of approximately 10 million as shown on Yahoo Finance and other data providers. The problem is that it’s not 10 million, but over 15 million as shown in the chart above and other sources such as Dilution Tracker. The issuance of shares at such a lightning pace that the data providers can’t keep up with it is an indication that DCTH remains a dilution machine. A review of its SEC filings does not disappoint when it comes to finding more substantial dilution:

SEC.gov

Some of these shares mentioned in the registration filing have already been issued, while others are based on contingent warrants which will bring in cash. But when all is said and done, DCTH’s share count will increase from about 10 million to 30 million. If someone suggests that $100 million is a fair to modest valuation for DCTH, that leads to a $3.33 stock price, not more than $10.

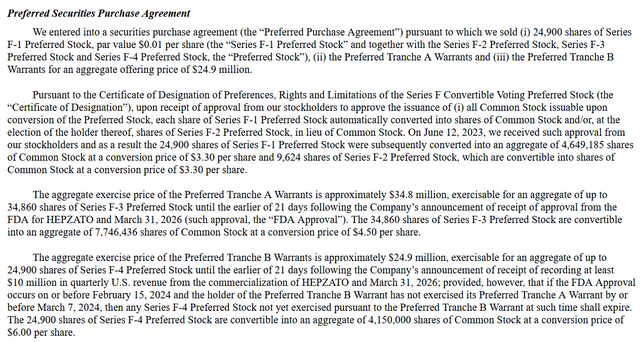

Diving into the details of the shares to be registered, we see that it’s not all bad news and empty dilution:

SEC.gov

4.6 million shares were already issued at $3.30 from the F-1 preferred share conversion, which looks to be the difference between some data providers reporting 10.6 million shares outstanding while others reporting 15.2 million shares outstanding. An additional 2.9 million shares from the F-2 preferred share conversion at $3.30 are to come. These transactions don’t bring any money into company coffers as DCTH already received the cash from the unregistered sale of these securities back in March.

7.7 million of the shares will be issued upon exercise of warrants at $4.50 per share. That would bring in nearly $35 million of desperately needed cash to the company. That’s the good news for bulls. The bad news is that these securities becomes exercisable 21 days following the FDA approval. Given the substantial size of the amount of shares relative to DCTH’s float, I expect the holders of these Preferred Tranche A warrants to short the stock over the next several weeks in order to lock in gains above the $4.50 exercise price. Deals like this are rally-killers. Retail investors and day/swing/news traders thrive on momentum. If there are a substantial amount of shorts looking to lock in profits from dilutive warrant transactions, they will sell into any rally. We saw that happening on Tuesday as the early pop over $7.00 was followed by an afternoon sell-off below $6.00. By the time these warrants are converted and the shares absorbed into the float, the short term momentum traders will have moved onto the next story.

4.2 million shares are issuable as a conversion price of $6, bringing in an additional $25 million. However, these warrants are not exercisable until March 2026 unless the company records $10 million in quarterly U.S. revenue from HEPZATO before then. So these shares, but also this cash, is not a concern any time soon. If one is to evaluate a price target based on future sales, they must include these shares in that analysis. But as far as analysis on near-term trading and float, using approximately 25 million shares is appropriate.

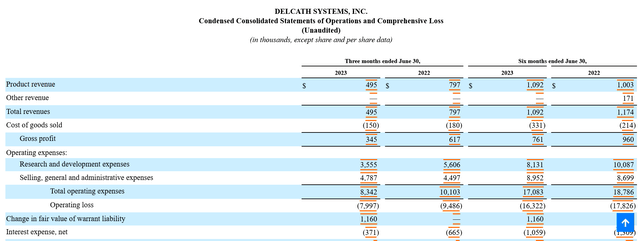

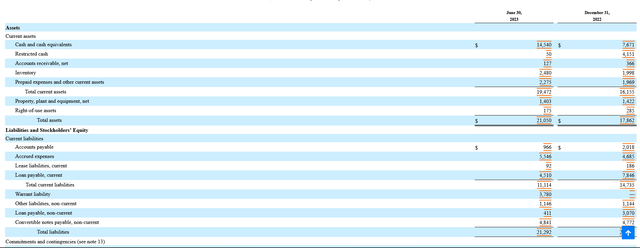

Having a look at the financial statements ended June 30, 2023, we see how badly the company needs that $35 million in cash from the exercise of the aforementioned warrants:

SEC.gov SEC.gov

The company has $15 million in cash, $8 million in working capital and negative shareholder’s equity while burning about $8 million a quarter. Without this FDA approval and cash injection from the warrant conversion, it would be insolvent by the end of the year. Costs will almost certainly ramp up as the company prepares for commercialization of the HEPZATO Kit by the end of the year. The $35 million in cash should extend the runway for three more quarters. If the company is unable to exceed $10 million in quarterly revenue by this time next year, the next set of warrants will not become exercisable and DCTH will likely need to finance at that time. Though it may not be at such a toxic level as previous financings.

Investors should be cautious chasing the FDA approval news. I think those who were smart to buy before the announcement as well as investors who purchased into the previous financing with convertible securities at $3.30 and $4.50 will be taking their profits. DCTH has a history of extensive dilution that has badly bitten long term holders of the past so the smart money will tend to be fleeting until DCTH proves that it’s no longer a dilution machine. While the FDA approval news is excellent, DCTH is not out of the woods yet as it has to prove that it can successfully and profitably market HEPZATO. Existing dilution implies at least 30 million shares outstanding with the potential for more equity raises a year from now. I expect the stock price to decline to around the $4.50 level over the next month as investors short the stock to lock in their profits and disappointed momentum traders sell at a loss and move on. Once the new warrants are absorbed into the float and excitement over the FDA approval has abated, that is the time for investors to evaluate the potential for a long position.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here