Moog Inc. (NYSE:MOG.A) manufactures precision motion and control systems. They operate in three segments, aircraft controls, industrial systems, and space and defense controls. Moog recently announced its Q3 FY23 results. I will review its financial result and analyze its technicals in this report. I think it is trading at a premium and is overvalued; hence I assign a hold rating on MOG.A.

Financial Analysis

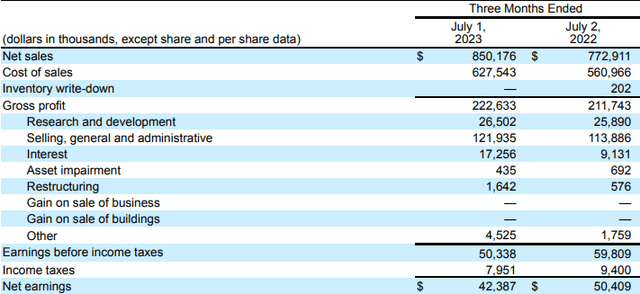

MOG.A recently posted its Q3 FY23 results. The net sales for Q3 FY23 were $850.1 million, a rise of 10% compared to Q3 FY22. I believe revenue increase in all three of its segments was the main reason behind the rise. The revenue from its aircraft controls segment grew by 12% in Q3 FY23 compared to Q3 FY22. I believe a 47% increase in its commercial OEM programs sales due to solid recovery in the business jet activity and a 14% increase in commercial aftermarket sales due to increased spares volume were the main reason behind the revenue rise in its aircraft controls segment. The revenue from its space and defense controls segment grew by 8% in Q3 FY23 compared to Q3 FY23. I believe the expansion of manufacturing on the reconfigurable turret program was the major reason behind the revenue rise in its space and defense controls segment. Now, talking about the industrial systems segment, its revenues grew by 9% in Q3 FY23 compared to Q3 FY22. I think the strong demand for flight simulation systems was the main reason behind the revenue growth in the industrial systems segment.

Seeking Alpha

Its operating margin for Q3 FY23 was 10.2% which was 10.5% in Q3 FY22. I believe the decline in margin was mainly due to additional space vehicle development charges. The net earnings in Q3 FY23 declined by 16% compared to Q3 FY22. I believe an additional $8 million of interest expense was the major reason behind the earnings decline. In my view, the financial performance of Moog was decent, and I think the decline in margins is not a big issue because the reasons for the decline weren’t serious and permanent in nature. The company had to spend an extra $14 million in the quarter on software development that was necessary to achieve success in its space vehicle development; the company has already completed most of its work, and I think we might not see such effects on the margins in the coming quarters because the additional costs which they had to incur in this quarter might not occur in the coming quarters because they have already completed more than 90% of the work in its space vehicle development work.

In addition, they faced supply chain challenges in this quarter, but management has bought some inventories to tackle this challenge. So, I think this might help them in improving the margins. In addition, their twelve-month backlog is up by 2% and has reached $2.3 billion, which shows strong demand in their business, and the management is spending heavily on the space vehicle and satellite program to boost revenues. I believe the space industry is a rapidly growing market, and the management’s effort to expand their business in this segment might prove beneficial for them in the future. The management has provided FY23 revenue guidance, which is 7% higher than FY22. Although the expected growth isn’t significant, positive revenue guidance is an optimistic sign, and looking at the management’s efforts to grow their business in the expanding markets, I think we might see good growth in their revenues in the future.

Technical Analysis

Trading View

Above is the monthly chart of Moog. It is trading at the $114.3 level, which is its all-time high. The stock looks bullish; it has broken the resistance zone of $100, which it has been trying to break since 2017. Since 2017 the stock has tried to break the $100 level several times but failed, but recently it has broken out of the $100 level, which shows that strength is present in the stock. But despite the bullishness in the stock, I would not advise buying it at its all-time high because, generally, when a stock breaks out of a resistance zone, it doesn’t shoot up instantly. It takes some time, and the stock consolidates near the breakout zone for some time before giving a fresh rally. Hence, I would advise waiting for the stock to return to the breakout level of $100 because I think buying the stock at the current level will not be a great risk-to-reward trade, so when the retest of the $100 level is done, one can start buying it.

Should One Invest In MOG.A?

Talking about valuation, it has an EV/EBITDA (TTM) ratio of 12.51x compared to the sector ratio of 12.23x. It has a P/E (FWD) ratio of 19.61x, which is higher than its five-year average of 15.81x and the sector ratio of 17.74x. It shows that it is currently trading higher than its historical average, and the sector median, which shows that it is currently overvalued. Taking its five-year average P/E ratio of 16.42x and its EPS (FWD), we get a share price of $94.5, which is way lower than its current price, so I think its current stock price is way higher and overvalued. In addition, it has a three-year revenue (CAGR) of 3%, which is quite low, and its FY23 estimated revenue growth is around 7%. So I think its past and future growth rate isn’t significant to justify its high valuation. However, the management is making several efforts to boost its revenue growth rate by expanding its business in the space industry by working on space vehicle development. But I believe these efforts will take some time to bear fruits. So I think we might not see a significant increase in revenue growth in the short term, and the company’s revenue growth in the short term might be moderate. When compared to its peers like Hexcel (HXL) and Spirit AeroSystems (SPR), the company has shown poor revenue growth. HXL has a revenue (YOY) growth rate of 15.4%, and SPR has a revenue (YOY) growth of 20.3%, which is higher than Moog’s growth rate of 7.4%. Hence, I believe it is currently overvalued, and I assign a hold rating on MOG.A.

Risk

A sizable majority of its sales go to the U.S. Government and its prime contractors and subcontractors. 42% of its total revenues in 2022 came from sales under U.S. Government contracts, especially in the aerospace and defense controls and aircraft controls sectors. 8% of its overall sales were to foreign governments. Government program funding can be divided into several separate contracts and relies on cyclical annual congressional allocations. When there are perceived risks to national security, U.S. defense spending may rise; conversely, it may fall at other times. Future defense spending levels are unclear and dependent on congressional discussion and budget allocation. Any future decrease in Department of Defense spending levels could have a negative effect on the company’s sales, operational profit, and cash flow. They have resources allocated to particular contracts with the government, and if any of those contracts are postponed or terminated, they may have to spend a lot of money redeploying those resources.

Bottom Line

Despite a moderate growth rate, the shares of MOG.A are trading at an all-time high. But I believe it is overvalued and not worth investing in at such high levels. Hence, I assign a hold rating on MOG.A for now.

Read the full article here