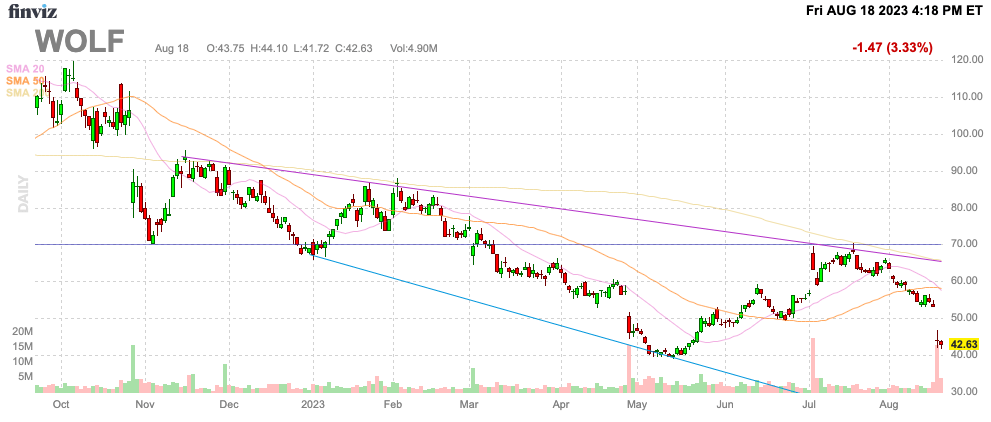

Wolfspeed (NYSE:WOLF) is forming a tradition of collapsing following quarterly earnings. The semiconductor company is busy building silicon carbide and related device facilities to meet surging EV and renewable energy demand, but the technology isn’t simple to implement. My investment thesis remains Bullish on the stock due to huge design-in wins, especially after these major dips.

Source: Finviz

Focus on Progress

Wolfspeed reported FQ4’23 results generally ahead of forecasts. The company definitely reported revenue above expectations at $236 million and the non-GAAP numbers were solid, though a shift in the reporting of facility start-up costs muddied the numbers.

The biggest issue remains around the ramp up of device output from the Mohawk Valley facility. Initially, Wolfspeed was hit with slow 200mm SiC crystal growth, leading to a pushback of scaling the facility.

The company entered the FQ3 earnings report with a goal for FY24 revenues reaching $1.3 billion, but the goal was cut to only revenues in the range of $1.0 to $1.1 billion. The biggest issues is that the device output from Mohawk Valley is pushed back around 6 months.

Wolfspeed now forecasts reaching 20% utilization of the fab in 2H’F24, leading to $100 million in quarterly revenues to start FY25. The fab has the potential for $2 billion in revenues once reaching full utilization.

The semiconductor company is now building the JP Siler City facility for the next growth phase. The fab will offer up to a 10x increase in materials capacity at scale, offering both 150 mm and 200mm wafers.

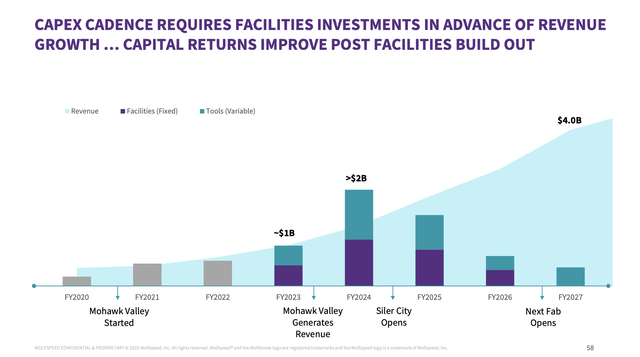

The biggest issue is pushing out the cash flow into future years. The capex plan highlighted back at the 2022 Investor Day is already being spent, but the plan for revenues during FY23 is now pushed out to only material amounts of Mohawk Valley revenues, not until reaching FY25.

Source: Wolfspeed 2022 Investor Day presentation

The last quarter of FY23 only produced $1 million in revenues from Mohawk Valley, while the ultimate full utilization levels reaches $500 million per quarter. The key here is that the facility has made substantial progress towards being in actual revenue ramp now.

During FQ4, Wolfspeed added another $1.6 billion worth of design-in wins. The company added $8.3 billion during FY23, bringing the total of cumulative awards in the last 4 years to $19.0 billion now.

At the investor event last October, Wolfspeed had $14.8 billion worth of cumulative design-in wins. The company is only operating at a $900 million annual revenue run rate for a book-to-bill ratio in the 9.2 range.

The market is disappointed the revenue aren’t coming fast enough, but Wolfspeed already has the design-in wins and the Mohawk Valley facility in ramp mode. The semiconductor company is making the progress, though not perfect at all.

Breeze Over Accounting Shift

The stock fell following earnings, due in large part to the accounting sift in how Wolfspeed will now report underutilization and startup costs of new facilities. Due to the impact on the financials of a company with sub-$1 billion in annual revenues, start-up costs and underutilization cost will have a huge impact on the financials for a new facility with the potential for $2 billion in annual revenues.

Previously, Wolfspeed was stripping out these charges as part of non-GAAP results provided to investors. The company reported a FQ4 non-GAAP loss of $0.42, missing analyst estimates by $0.22.

The key is that $0.26 of the loss were the $39.5 million worth of factory start-up costs in the quarter. The actual non-GAAP loss based on the prior accounting method was around $0.16, easily beating estimates by $0.04.

The company guided to a combined loss of $45 million for FQ1’24 leading to an additional EPS loss in the quarter of nearly $0.30. Whether or not the SEC forced Wolfspeed to include these costs in the non-GAAP numbers, the stock value shouldn’t be altered.

The disappointing aspect is how some analysts handled the shift. The CFO promised to continue breaking out the costs, allowing analysts and investors to make their own adjustment, but Charter Equity analyst Edward Snyder seemed to imply the investment story has somehow changed via this question on the FQ4’23 earnings call:

We spent most of last year with all the operational problems talking about the ramp of Mohawk Valley and how your targets were for yields and margins and how you would pro forma out those numbers so we get a good glimpse of if it was living up to expectations or not. And it sounds like based on your answer, what Jed said, you were not forced to make this decision by SEC. Correct me if I’m wrong. Did the SEC tell you, you had to do this? And if they didn’t tell you to do this, why in the very first quarter we do this, would you now mix it up so that your public report looks just terrible, right?

Takeaway

The key investor takeaway is that Wolfspeed has the revenue ramp finally set up for the rest of FY24, with a much bigger jump in FY25. The stock trades at less than 4x FY25 revenues, providing the bargain price level where Wolfspeed typically bounces.

Read the full article here