Investment thesis

Our current investment thesis is:

- GIII has struggled to maintain interest in its brands, with increased competition from the rise of social media/e-commerce, leading to softening revenue growth. We believe this continues to be a key threat to the business.

- The loss of its Tommy Hilfiger and Calvin Klein licensing agreements will be a disaster for GIII, contributing to a material adverse impact on its financial performance. We do not believe GIII is positioned to offset this impact in the coming years.

- The nail in the coffin in our view is its performance relative to peers, which is extremely disappointing, with no scope for parity. GIII is one of the weakest members of the apparel industry.

Company description

G-III Apparel Group (NASDAQ:GIII) is a leading designer, manufacturer, and distributor of apparel and accessories. Headquartered in New York City, the company operates in the fashion industry and is known for its diverse portfolio of brands that cater to various customer segments.

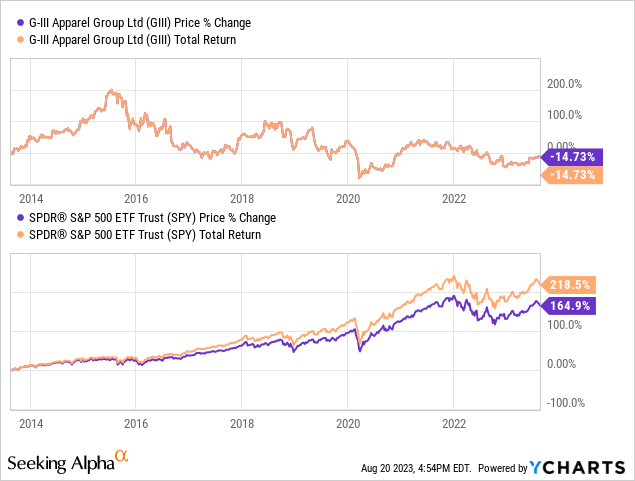

Share price

GIII’s share price performance has been disappointing, as changing industry dynamics, namely changing trends and increased competition, have contributed to poor financial results.

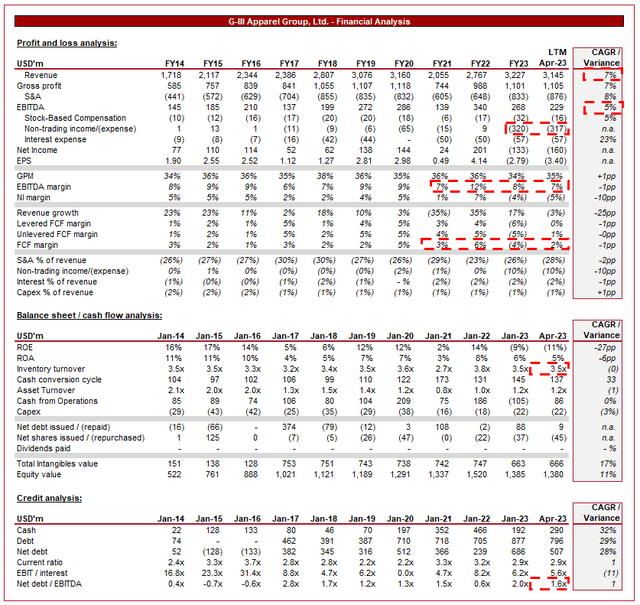

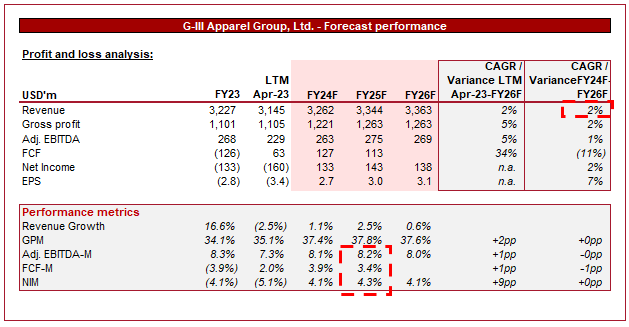

Financial analysis

G-III Financials (Capital IQ)

Presented above is GIII’s financial results.

Revenue & Commercial Factors

GIII’s revenue has grown at a CAGR of 7% during the last decade, with broadly consistent growth that has ticked down in recent years. M&A is a core part of the company’s strategy, supporting the growth story during this period.

Business Model

GIII Apparel Group owns and licenses a portfolio of well-known brands, including DKNY, Donna Karan, Karl Lagerfeld, Vilebrequin, G.H. Bass, Eliza J, Jessica Howard, Andrew Marc, Marc New York, Wilsons Leather, and Sonia Rykiel.

In addition, GIII offers a selection of products under a collection of licensed brands that includes Calvin Klein, Tommy Hilfiger, Levi’s, Guess?, Kenneth Cole, Cole Haan, Vince Camuto, and Dockers.

The company offers a diverse range of products, including outerwear, dresses, sportswear, and more. This variety allows GIII to cater to different customer preferences and market segments, leveraging the value of its brands to maximize sales.

GIII distributes its products through various channels, including wholesale to department stores and specialty retailers, as well as through its retail stores and e-commerce platforms. The vast majority of the company’s revenue is achieved through the wholesale channel, leaving the business susceptible to changes in retailer stock levels but maximizing its reach to consumers and limiting stock on hand.

GIII primarily targets the female demographic, led by brands such as DKNY. The female segment is more lucrative as they make up more than half the US population, control or influence 85% of consumer spending, and are more resilient with spending. This is primarily how GIII has achieved positive organic growth.

GII has struggled with maintaining interest in its brands, with the likes of DKNY experiencing a sustained for many years (as the below illustrates). The apparel industry is highly competitive, with consumer trends and tastes changing over time. This makes it incredibly difficult to maintain consumer interest for a substantial amount of time, particularly if the brand is not one of the few globally that is trend-setting.

Management has relaunched and repositioned the DKNY brand in the past and is attempting to do something similar for Donna Karen, seeing potential with both brands. We do think there is value with these brands but with so many brands following a similar design philosophy to attract consumers, we struggle to see how DKNY stands out.

DKNY (Google)

Within GIII’s financial statements, Management has disclosed the following

“PVH Corp. (PVH), the owner of these two brands, has indicated that it intends to produce these products itself once the license agreements expire.

Unless we are able to increase the sales of our other products, acquire new businesses, and/or enter into other license agreements covering different products, the inability to renew the Calvin Klein and Tommy Hilfiger license agreements would cause a significant decrease in our net sales and have a material adverse effect on our results of operations.“

This is a logical step for PVH as Tommy Hilfiger and Calvin Klein are globally successful brands that have seen an improvement in recent years, likely contributing to the end of various agreements such as this to bring the success in-house.

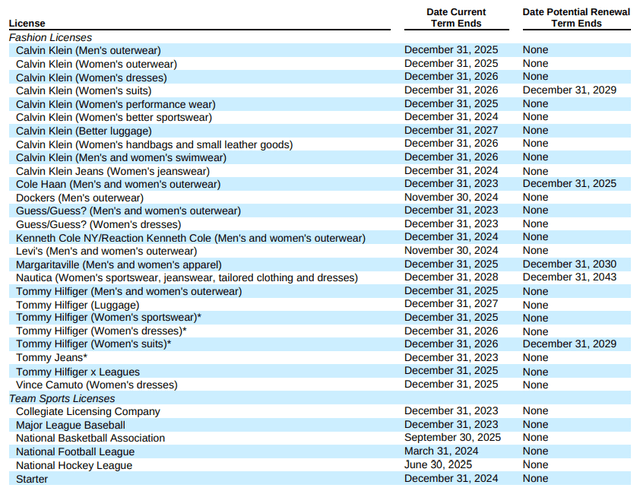

This is disastrous news for GIII, as Sales of licensed products comprise 58.6% of revenue in FY23 (67.2% in FY22 and 68.5% in FY21). The below table lists all current licenses held by the business and as the reader will observe, the largest and most frequent of which are Calvin Klein and Tommy Hilfiger. This implies a large portion of this 58.6% of revenue will go once these licenses will expire (Management does not disclose and so assumptions need to be made).

Licenses (G-III)

What compounds this issue for GIII is three key factors. Firstly, its organic growth is not high enough to offset the loss come the expiry date. Secondly, GIII lacks the financial capabilities to conduct genuinely transformational M&A. During a high-interest rate environment, a large chunk will need to be funded with cash, and with a FCF margin of <5%, this will be difficult to achieve. Finally, markets are aware GIII needs to achieve inorganic growth to support the business, leaving it susceptible to difficult M&A negotiations and the potential of unfavorable takeover terms.

Competitive Positioning

We believe GIII’s key competitive advantages are:

- Brands. GIII owns several valuable brands, which should ensure a healthy level of demand and the potential for growth if interest can be sustainably developed.

- Focus on Women. Women control or influence 85% of consumer spending, making the segment extremely lucrative and more robust against cyclicality.

- Production expertise to expand licenses/incorporate new brands. GIII’s relationship with PVH has illustrated its ability to produce high-quality products and meet consumer demand effectively, representing an opportunity to expand its licensing capabilities to offset the loss of Tommy Hilfiger and Calvin Klein.

Broadly, however, we believe the business has become less competitive within the apparel industry and is facing significant threats to its position above and beyond the loss of its various licenses.

Our key concerns include:

- New Competition. The fashion industry is highly competitive, with numerous brands vying for consumer attention as trends change and fluctuate over time. The rise of social media has made it incredibly easy for new entrants and swings in consumer interests. This has reduced the power brands like DKNY have in the market, degrading brand value.

- E-commerce Impact. The rise of e-commerce has altered how consumers shop, contributing to greater choice and comparability by consumers. We believe this has been a serious issue for major brands, as it is far easier to discover new brands.

- Retailer Challenges. G-III’s wholesale distribution exposes the company to challenges faced by its retail partners, including store closures and changes in inventory strategies. This has been in large part due to the impact of e-commerce.

G-III Apparel operates in a competitive environment within the fashion and apparel industry. Key competitors include PVH Corp, Ralph Lauren Corporation (RL), and Tapestry, Inc (TPR).

Economic & External Consideration

Current economic conditions represent a near-term risk to the business, with high inflation and elevated rates contributing to softening discretionary spending. There have been impressive resilience in demand globally, nevertheless, we are concerned.

In GIII’s most recent quarter, the company posted an (11.9)% decline in recent, its first negative quarter following a strong period for the business post-pandemic. Further, GIII has been its OPM decline, falling from 6.7% in the prior quarter to 2.5%. Both declines are a reflection of softening demand, although it is worth highlighting that the business beat expectations and performed well to reduce inventory levels.

Further, GIII announced a licensing agreement with Xcel Brands for the brand Halston (25 years), with the option to buy the brand at the end of this period. This is a positive development for the business and we believe the monitoring of further agreements is key.

Outlook

Valuation (Capital IQ)

Presented above is Wall Street’s consensus view on the coming 5 years.

Analysts are forecasting flat revenue growth in the coming years, with minimal margin improvement. Given the near-term trajectory, and importantly the attractiveness of its brands, we consider this a reasonable estimate.

Although the business is seeking to acquire brands and new licenses, we struggle to see these being material enough to drive the top line.

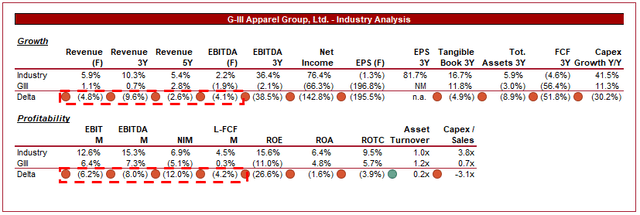

Industry analysis

Apparel, Accessories and Luxury Goods Stocks (Seeking Alpha)

Presented above is a comparison of GIII’s growth and profitability to the average of its industry, as defined by Seeking Alpha (27 companies).

GIII is a clear underperform, with a negative result relative to the cohort on all but one of the metrics. The company has been unable to exploit the post-pandemic spike in demand, continuing to lose market share. Further, its margins are significantly below the market average, with no realistic scope to sufficiently close this gap.

This compounds the unattractiveness of the business we feel, as the underlying financial performance with the PVH brands is subpar relative to the industry.

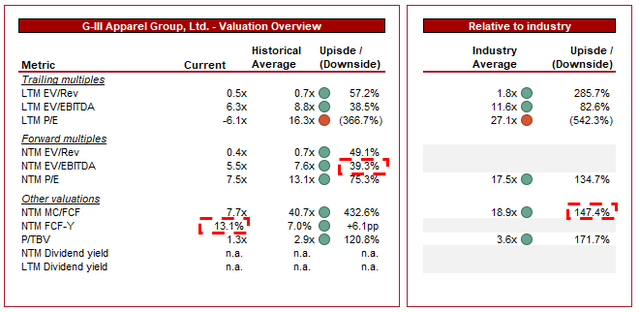

Valuation

Valuation (Capital IQ)

GIII is currently trading at 6x LTM EBITDA and 5.5x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is warranted in our view, primarily due to the continued decline in brand value, weakening financial performance, and loss of key licenses. The current discounts look broadly reasonable, although we suspect this can decline further.

Additionally, GIII is trading at a discount to its peer group, a justifiable position given the weakness relative to the group. This is far more difficult to quantify given the significant size of the weakness.

GIII currently has a NTM FCF yield of 13%, supporting the argument the business is fairly valued, or at least not overvalued. We would not argue against this, although suggest the issue here is that GIII is likely to continue to decline as financial performance continues to underwhelm as the business approaches the loss of Tommy Hilfiger and Calvin Klein.

Final thoughts

GIII owns several culturally important brands but we do not think this is sufficient to make this an attractive business. The business is facing a substantial decline in future earnings, while currently generating unattractive financial returns and does not have a clear route to offsetting the commercial losses ahead.

This does not look to be an attractive long-term investment, even if the stock is not glaring overvalued.

Read the full article here