Cedar Fair (NYSE:FUN) operates amusement and water parks in the United States and Canada. After a difficult pandemic-related market, the company’s earnings have bounced back significantly. Although the company seems cheap at first glance, I believe the company’s large debt balance makes the valuation reasonable as investors are exposed to risks caused by the leveraged balance sheet. As such, I have a hold-rating for the stock.

The Company

Cedar Fair operates amusement and water parks, as well as hotels related to the parks:

Cedar Fair’s Brands (cedarfair.com)

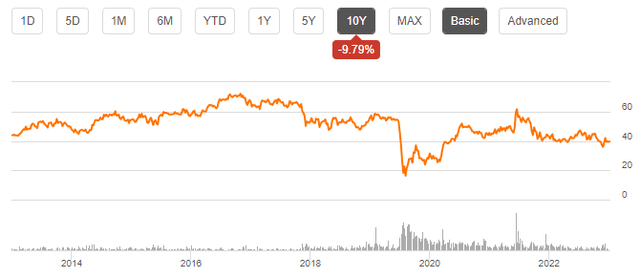

The company has a very long history, as Cedar Fair opened their first park over 150 years ago in 1870 in Ohio. Although the company has recovered its earnings impressively from pandemic lows, the company’s stock continues to trail both short- and long-term:

Cedar Fair’s Stock Chart (Seeking Alpha)

Prior to the pandemic, Cedar Fair paid a good dividend yield – in 2019 the company had quarterly dividends of $0.93. Although Cedar Fair started to pay dividends again in August of 2022, the dividends have been significantly lower than prior to the pandemic – the quarterly dividends have only been $0.30, making the current yield 3.00%.

Financials

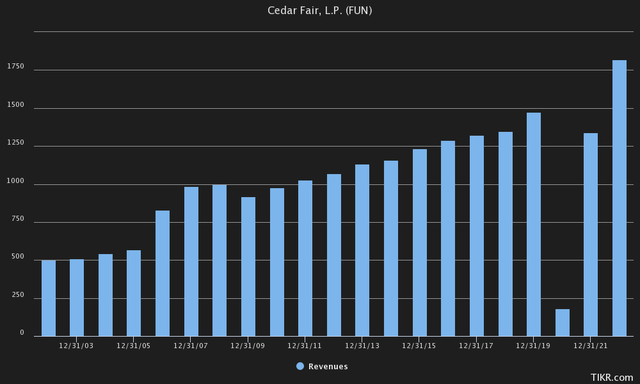

Cedar Fair has had a very solid growth in revenues throughout the company’s history from 2002, as the compounded annual rate has been 6.6% from 2002 to 2022:

Historical Revenues (Tikr)

The only hiccups in the park operator’s growth have been the 2008 financial crisis affecting 2009 revenues, and most recently the Covid pandemic, crashing Cedar Fair’s revenues by around 88% in 2020.

The company has since recovered from the pandemic, posting new record revenues in 2022. Most recently, though, the company has seen some issues as revenues have decreased in both Q1 and Q2 of 2023, with a Q2 decrease of 1.7%. Cedar Fair’s CEO, Richard Zimmerman, attributes the poor revenue performance to weak weather conditions in the quarter in the company’s Q2 press release:

“Unfortunately, anomalous weather patterns – including unprecedented rainfall in California and wildfires in Canada – have significantly disrupted year-to-date attendance, as well as sales of 2023 season passes, creating a headwind on demand. To better adapt to changing market dynamics, we have expanded our research efforts to further isolate the impact of macro factors on specific markets.”

Zimmerman doesn’t seem to attribute the decrease to macro factors in a significant manner; the company claims on its investor relations website to be a resilient and a non-cyclical business. At some level, this seems to be true from Cedar Fair’s performance in the 2008 financial crisis – the company’s revenues only decreased by eight percent in 2009 from 2008 highs. The crisis did show up a bit more in the operating earnings, as the company’s EBIT did decrease by 27% in the year – still a moderate amount compared to many other companies in the year.

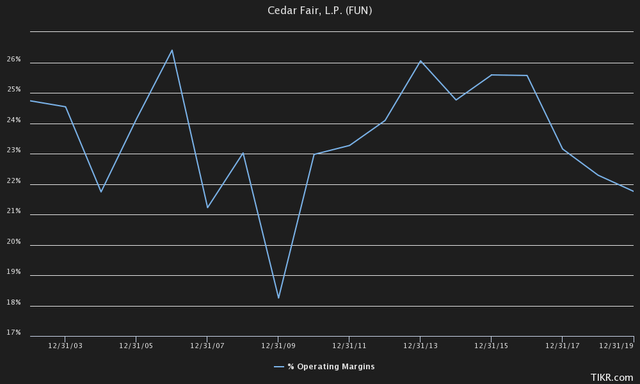

Cedar Fair’s earnings stability is boosted by the company’s high operating margin; in 2022, the company achieved a margin of 20.6%, representing a very healthy level. Even though the margin is high, it is still below the park operator’s long-term average – prior to the pandemic, Cedar Fair had an average margin of 23,5%:

Historical EBIT Margin (Tikr)

Unlike the company’s operating margin, Cedar Fair has a weak balance sheet. The company currently has long-term debts of $2.43 billion; compared to the company’s market capitalization of around $2.04 billion, the amount seems excessive. I believe two factors do somewhat mitigate the risk brought by the debt – firstly, no amount of the long-term debt is in current portions as Cedar Fair has flexibility in the payment schedule. Secondly, the company’s earnings have historically been very stable, with the pandemic representing the only very significant drop. The interest expenses are currently around 43% of the company’s operating earnings with trailing numbers – a high amount, but not catastrophic in my opinion due to the mentioned reasons.

Valuation

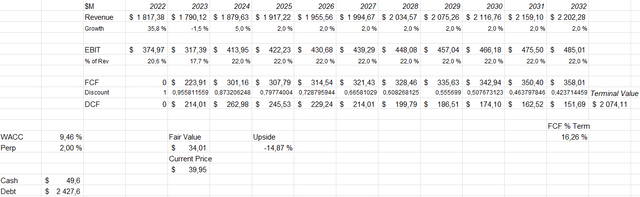

Cedar Fair has a trailing P/E of 8.11. Although the ratio seems low, I believe investors must consider the large outstanding debt as well as the currently decreasing revenues. To get a further context of the stock’s valuation, I constructed a discounted cash flow model as usual.

In the model, I estimate Cedar Fair to have a revenue decrease of 1.5% in 2023, as the macro factors are quite weak, and the first half has had decreases in revenue. In 2024, I expect a jump of 5% as macro and weather conditions should normalize. After 2024, I estimate Cedar Fair to have a growth of 2% – although the growth is significantly lower than Cedar Fair’s historical average of 6.6%, I believe it’s reasonable to stay conservative in the estimates.

For the company’s EBIT margin, I estimate a decrease of 2.9 percentage points into a margin of 17.7% as inflation increases the company’s expenses in a sudden way and as revenues are a bit below a normalized level. After 2023, I estimate the company to have a stable EBIT margin of 22.0%, a bit below the company’s historical average. These estimates along with a weighted average cost of capital of 9.46% craft the following DCF model, with an estimated fair value of $34.01, around 15% below the current price:

DCF Model of Cedar Fair (Author’s Calculation)

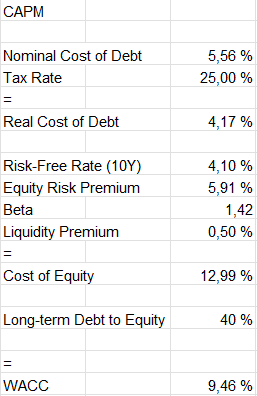

The used cost of capital is derived from a capital asset pricing model:

CAPM of Cedar Fair (Author’s Calculation)

Cedar Fair guides interest expenses of $130 million to $140 million in 2023. The middle point of this guidance would represent an interest rate of 5.56% with the company’s current amount of debt, which I use in the model. As the company is highly leveraged and has been for a long time, I estimate the company’s long-term debt-to-equity ratio to be 40%.

On the cost of equity side, I use the United States’ 10-year bond yield of 4.10% as the risk-free rate. The equity risk premium estimate of 5.91% is Aswath Damodaran’s calculation made in July. Tikr estimates Cedar Fair’s beta to be 1.42, which I use in the model. As the company’s earnings seem to be resilient, I believe the beta could be currently higher than it should be as the company has had significant correlation with the pandemic – I believe the only reason that the beta should be high would be the leveraged balance sheet. Although the beta could very well decrease in the future, I use the estimate of 1.42 to be conservative. Finally, I add in a liquidity premium of 0.5% creating a cost of equity of 12.99% and a WACC of 9.46%.

Takeaway

Excluding the pandemic, Cedar Fair seems to generate steady earnings and cash flows to investors. Although the company seems quite cheap, I believe the valuation is currently justified as the park operator has a very high amount of debt. For the time being, I have a hold-rating for the stock.

Read the full article here