Investment briefing

Following its Q2 FY’23 numbers Glaukos Corporation (NYSE:GKOS) has demonstrated its propensity to unlock shareholder value over the medium term. Another strong quarter at the top-line is backed by robust economic factors, as it is growing gross profitability off a smaller degree of assets employed into the business. Since the last publication, the stock sells ~9% higher.

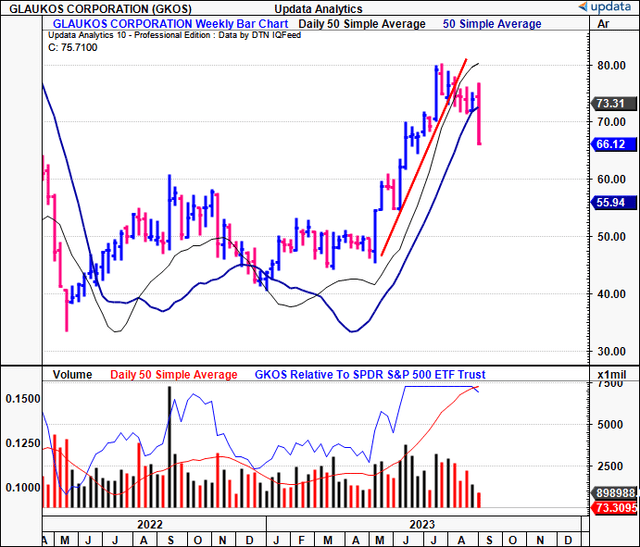

This economic leverage shouldn’t be discounted, even with the recent pullback in market pricing as we rolled into July/August. For one—as I’ve rhapsodized at lengths over our entire healthcare coverage universe—the healthcare basket has copped a large wave of selling pressures in H2 FY’23, and GKOS hasn’t been immune to this. Critically, the 10-week average buying volume has increased substantially over the last 2 months (shown in Figure 1, via the red MA line in “volume”, the lower pane), illustrating demand is still there in the near term. Backed by the fundamental factors above, the scope for GKOS to price higher over the mid-term is compelling in my view, and I continue to rate the company a buy on long-term value. This report will run through the reasoning why. Net-net, reiterate buy.

Figure 1.

Data: Updata

Key risks to thesis

it is critical that investors understand the following set of risks that could nullify the thesis:

1). GKOS’ sales growth is sensitive to the business cycle and an economic slowdown may impact the propensity of patients to consider its offerings. This should be factored in given the inflation/rates axis, alongside potential forex headwinds from its international markets.

2). It’s iDose segment may fail to obtain full FDA approval, which could hurt its stock price given much of the company’s current market value is growth-dependent as much as it is from its current level of operations.

3). Broad healthcare has sold off in H2 this year and this could continue. With rotation out of the sector, this could impact demand in GKOS’ stock and see it struggle to trade higher.

4). Any regulatory pressures from CMS on proposed rates and rate changes could have a material impact on its sales outlook. Whilst these are difficult to predict, it’s worth keeping a very close eye on the same as it may result in selling pressures if there’s negative developments in terms of pricing or reimbursements for 2024.

Investors must recognise these risks in full before proceeding to any investment decisions.

Critical updates to investment thesis—Q2 earnings, economic factors, valuation

1. Insights from Q2 FY’23

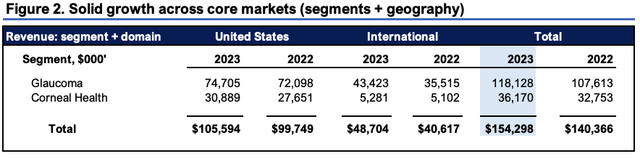

GKOS put up net sales worth $80.4mm, up 11% YoY on a core EBITDA loss of $17.7mm. This was a record second quarter for the company and was underscored by growth across its core portfolio of glaucoma and corneal health. The company is now in a strong position for management to revise its FY’23 net sales guidance, which it did to $304—308mm (previously $295—300mm).

The divisional breakdown on GKOS’ Q2 top-line is as follows:

- U.S. glaucoma sales tallied $39.6mm, clocking a 4% YoY growth rate and a growth of 13% sequentially. The company now has its sights set on driving its iStent infinite segment, even before formal Medicare Administrative Contractor (“MAC”) coverage and payments come into play. More on the company’s MAC coverage later.

- Ex-U.S. glaucoma sales booked $22.3mm for the quarter, up 25% YoY. Around 200bps of FX headwind is backed into this number. Adjusting for this (in constant currency terms), it was a 27% growth rate for the quarter.

- Meanwhile, its corneal health business put up record sales of $18.5mm, an 11% increase on Q2 last year. Its photrexa line delivered record sales of $15.9mm and grew 18% YoY.

Sources: BIG Insights, GKOS Company filings

Critically, there’s been substantial progress towards achieving iStent infinite coverage under Medicare Parts A and B. To date, 5 out of the 7 relevant Medicare Administrative Contractors (“MACs”) have approved local coverage determination (“LCD”) reconsiderations that would provide coverage that is consistent with FDA approval. The remaining two MACs are in the process of assessing iStent infinite coverage by either 1) proposing LCDs, or 2) updating temporary local coverage articles (“LCA”). For reference, MACs publish LCAs—which are educational documents containing guidelines related to coding and other technical aspects that support an LCD.

CMS is closely monitoring patient access to interventional glaucoma tools, alongside the MAC policies and processes surrounding glaucoma procedures. For GKOS, there have been notable developments to its current procedural terminology (“CPT”) coding. For one, there’s been a shift of the CPT code for iStent infinite and stand-alone procedures from APC 5491 to APC 5492. There’s also been a proposed reassignment of the code for combined cataract procedures (including trabecular bypass procedures), “66989” and “66991”, to a new code, APC 5493, as part of CMS’ 2024 proposed rule.

Finally, GKOS’ new drug application (“NDA”) for its iDose travoprost intraocular implant has been accepted by the FDA. iDose is an interesting formulation. It is a “1.8 x 0.5mm biocompatible titanium implant that releases a proprietary formulation of travoprost inside the anterior chamber [of the eye]“. Travoprost is a prostaglandin analogue that can reduce the pressure in the eye, the classic sign of glaucoma. It is currently working with the FDA as the agency reviews the application, with the goal date set for December 22nd this year. Consequently, the iDose commercial launch is scheduled for early FY’24.

2. Economic growth levers

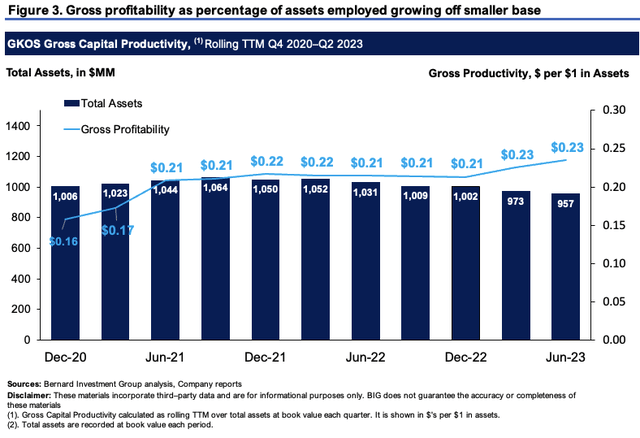

Analyzing the company’s profitability as a function of assets employed into the business reveals positive factors.

Figure 3 outlines the company’s gross profit as a percentage of total assets employed, on a rolling TTM basis from 2020–2023. All core and non-core assets are included. Clearly, GKOS is creating value from its sales growth to date. Reported TTM gross margin was 75.65% in Q2, up 500bps from 2020, and in-line with range observed across 2022–’23.

But as a percentage of resources employed into the business, the company is returning $0.23 for every $1 in assets. This, of a smaller asset base than in 2020. Hence—more gross profit off less ‘investments’. In terms of return on investment, this is a pleasing figure. I’d be looking for this trend to continue for GKOS as it ramps up its operations and clinical programs; the latter of which could unlock further value with iDose TR converting from the pipeline onto market.

BIG Insights

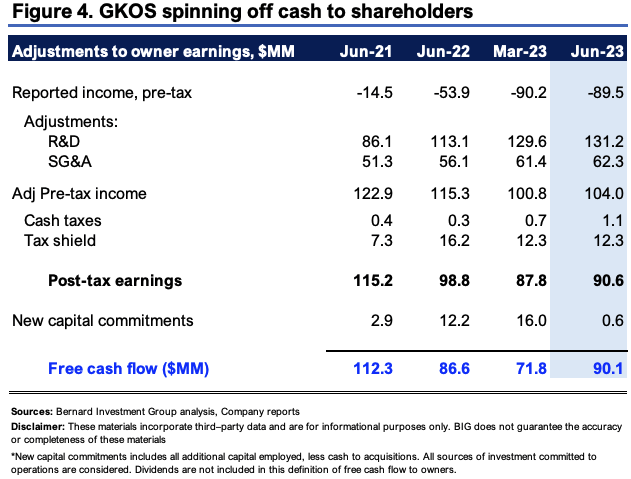

Certain adjustments are also required from GKOS’ reported statements to reconcile investments that are expensed on the balance sheet. Figure 4 depicts this in detail over rolling TTM periods since 2021. R&D is one such line item, and I’ve adopted research that advocates for 30% of SG&A to be capitalized as an intangible investment within speciailzed healthcare companies. Both items are included as intangible investments, then amortized in a straight line over a 7-year useful life.

After completing the necessary adjustments, it shows the company’s estimated post-tax earnings (NOPAT) at $90.6mm for the company. Considering all new capital commitments—including the capitalized expenditures from the P&L—I get to GKOS spinning off $90mm in cash to shareholders last period (TTM basis). This is up from Q2 FY’22 and Q1 FY’23, respectively.

Using a steady-state valuation, that capitalizes the company’s FCF to owners at the long-term market return on capital (12% here), this gets to $751mm in implied market value (90.6/0.12 = $751). Hence, investors have placed a 3.9x multiple (or $2.9Bn) premium on the company’s forward growth prospects. To me this is a bullish sign and tells of what the market expects for GKOS into the coming periods.

BIG Insights

Valuation and conclusion

The stock sells at 12x forward sales, and this is quite the premium to the sector, 200% to be exact. This supports the findings from earlier that showed the growth expectations. Using the equation of Value = steady-state + growth contribution; GKOS’ equivalent would be GKOS Value = $751 + $2,900. Alas, the bulk of its current market value is biased to the growth contribution, clear indication of the market’s outlook on the company. What validity is there for this though?

For one, management looks to $304—308mm at the top line this year, ~9% YoY growth from FY’22. Consensus looks to $407mm in revenues by FY’25, calling for another $100mm over the 2 years. That’s 9.2x today’s enterprise value (“EV”). The market is looking for the company to increase revenues by 1.3x over the coming 2 years, therefore (12/9.2 = 1.3x). To me this seems perfectly reasonable and may be subject to change to the upside with the pace GKOS is printing sales growth.

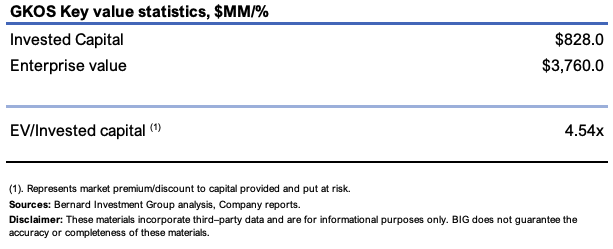

Second, the market places a high premium on the capital employed into GKOS’ operations [Figure 5]. It prices the company’s invested capital at a 4.5x multiple in the market, excluding all cash on hand. This also corroborates the growth expectations as it implies the market foresees this capital invested to produce strong growth in income (sales, EBITDA, etc.) over the coming periods.

At 12x forward using management’s $340mm estimates I get to $4.1Bn in market value or $84/share, and this supports a buy rating in my view. I’d be looking to this mark as the next price objective.

Figure 5.

BIG Insights

In short, there are multiple inflection points driving GKOS’ market value at the time of writing. The company continues on its growth route and is posting solid numbers at the top line each quarter. Critically, the gross profits produced of assets employed in the business are demonstrating excellent leverage and growing each period. This cannot be discounted, and the regulatory tailwinds discussed here add another interesting flavour to the investment recipe. If we are to serve up GKOS on a silver plate to our portfolios, the combination of all the investment flavours is appealing in my view, making for a tasty meal (and by tasty, I mean prospect for further capital gains). Net-net, I continue to rate GKOS a buy, eyeing $84/share as the next price objective. Reiterate buy.

Read the full article here