Walgreens Boots Alliance, Inc. (NASDAQ:WBA) looks in disarray after the company announced that Rosalind Brewer was stepping down as CEO immediately. Lead Independent Director Ginger Graham will take over as interim CEO.

This follows CFO James Kehoe announcing at the end of July that he was stepping down in mid-August to pursue an opportunity in the tech sector. So in span of a few weeks, WBA has lost its top 2 execs, with neither having a full-time replacement.

Under Brewer, who became CEO in March 2021, WBA has undergone a transition to become a broader healthcare company. The former CEO aggressively invested in its healthcare segment by buying up and investing in companies that touch patients across the healthcare continuum.

Brewer’s goal was to create an integrated healthcare-pharmacy services company that could be there with a patient through their medical journey, from pre-medical visit through post-discharge in-home care. Her hopes were to provide value both to patient by delivering better medical outcomes, as well as to payors by driving down costs.

In the process, Brewer went on a buying spree of medical groups. In 2021, after Brewer became CEO, WBA raised its stake in VillageMD from 30% to 63% by investing $5.2 billion in the company. The investment was to help the company expand nationally, and also to speed up opening Village Medical within existing Walgreen Drugstores.

Brewer doubled down on VillageMD this year, as its now majority owned subsidiary closed an $8.9 billion deal in January for Summit Health, which runs the urgent case chain CityMD in New York and New Jersey. It also acquired Starling Physicians, which is a medical group that offers everything from primary care to specialties such as cardiology in over 30 locations in Connecticut.

In addition to adding medical practices, under Brewer, WBA also acquired Shield and CareCentrix. CareCentrix is a platform centered on home-came coordination and value based in-home benefit management, while Shield is a specialty pharmacy integrator and accelerator with solutions to help increase drug access for specialty pharmacies and complex patients.

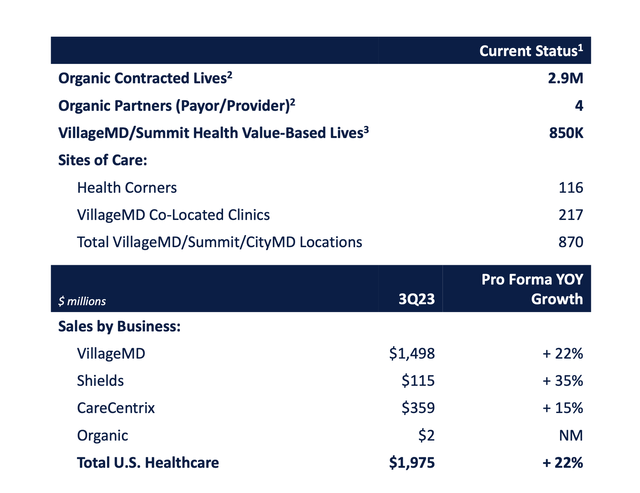

WBA’s Healthcare segment showed growth in its most recent quarter, with the segment seeing 22% pro forma growth. VillageMD grew its revenue 22% to $1.5 billion. Shields revenue jumped 35% to $115 million, while CareCentrix revenue was up 15% to $359 million.

Company Presentation

Despite the growth, VillageMD and CityMD (Summit) have been underperforming and the company has slowed the pace of clinic opening in new markets for VillageMD. The company was set to refocus its growth plans and focus of adding clinics to existing market to create regional density and support more profitable growth.

On its fiscal Q3 earnings call, Executive SVP John Driscoll said:

“While we’re confident in the range and scale of our health care business, we are disappointed with the pace of our path to profitability. U.S. healthcare missed targets due to VillageMD and CityMD underperformance, directly related to reduced COVID, cold and flu season and softer market demand. We’re taking immediate actions to drive improved profitability. We anticipate this year will remain a transition year as we take action to deliver value and drive profitability. We’re rightsizing our cost structure through optimizing overhead and revenue synergies to better match market demand. We’re raising and accelerating synergy capture goals. We believe that we can enhance Village growth and value by focusing on gaining density in existing markets to accelerate VillageMD’s path to profitability and supporting the integration of our digital assets with our VillageMD platform and we continue to enhance our village management team. We’ve recruited Rich Rubino, a seasoned health care CFO to be the Chief Financial Officer of the combined VillageMD Summit business. Longer term, we’re implementing a high-impact, 3-year plan to improve performance through an intense focus on operational excellence and cost optimization. Achieving our health care vision depends on each of our companies, delivering on their respective plans and relentless execution of harvesting growth synergies across the Walgreens portfolio. We’re building a differentiated, value-based care delivery model that successfully integrates pharmacy and medical care for a value-based care market that will more than double by 2027.”

In addition to announcing that Brewer would step down as CEO, WBA also said that its full-year adjusted EPS guidance would be at or near the low-end of its prior guidance. The company lowered its full-year forecast at the end of June from adjusted EPS of between $4.45-4.65 to a range of $4.00-4.05. At the time, the company said it was being impacted by lower COVID-19 vaccine and testing volumes, as well as a challenging consumer and macroeconomic environment.

Valuation

Based on the 2024 EBITDA (ending August) consensus of $5.8 billion, WBA trades at an EV/EBITDA multiple of about 10.7x. Based on the 2025 EBITDA estimate of $6.8 billion, it trades at about 9x.

On a P/E basis, the stock trades at 6.2x the fiscal 2024 consensus of $3.85.

The company is projected to grow revenue 4.5% in fiscal 2024 and 5.4% in fiscal 2025.

It trades at a premium to rival CVS Health Corporation (CVS), although CVS also does managed care and has a PBM, so the models are quite different.

Conclusion

In my original write-up on WBA back in March, I wrote that there was no guarantee that the company’s vision of an integrated healthcare-pharmacy services company that connects with patients throughout their care continuum would actually come to fruition, while also noting I thought there were some conflicts of interest in the strategy. With Brewer now gone, it appears her strategy was not working and what the next CEO does is a huge question mark. At the same time, the company still faces headwinds from less COVID tests and vaccinations.

At this point, Walgreens Boots Alliance, Inc. stock is a rudderless ship with an unknown strategy, and thus is pretty much uninvestable at the moment. The new CEO will have to decide whether to try to turn around its medical groups business, or whether to try to cut bait. Either way, it won’t be an easy decision given the money that Brewer spent acquiring these assets. At the same time, I also wouldn’t call WBA stock cheap enough to make a blind bet on a turnaround.

As such, I’m neutral on the name and would stay far away from Walgreens Boots Alliance, Inc. on the sidelines.

Read the full article here