Introduction

When I first reviewed the PennyMac Mortgage Investment Trust NT 8.5% 28 (NYSE:PMTU), issued by PennyMac Mortgage Investment Trust (PMT), it received a Buy rating as a good choice to lock in a good YTC/YTM before the anticipated rate cuts people expected by the FOMC in 2024. Well, that hasn’t happened yet, though it appears such actions might occur this fall.

In my prior article, I compared PMTU against two similar Notes issued by another mREIT, the Eagle Point Credit Company (ECC). Here, I do the same with one ECC Note and two recently issued Notes by the AG Mortgage Investment Trust (MITT), which another article recently reviewed.

Based on that comparison, I dropped my rating from Buy to Hold for the PMTU as features on the other Notes it was compared to reward today’s investors better.

PennyMac Mortgage Investment Trust Review

Understanding the Issuer is a critical part of the Note’s review. This is how Seeking Alpha describes this mREIT (condensed):

PennyMac Mortgage Investment Trust, a specialty finance company, primarily invests in mortgage-related assets in the United States. It operates through four segments: Credit Sensitive Strategies, Interest Rate Sensitive Strategies, Correspondent Production, and Corporate. The company’s Credit Sensitive Strategies segment invests in credit risk transfer agreements, CRT securities, distressed loans, real estate, and non-agency subordinated bonds. Its Interest Rate Sensitive Strategies segment engages in investing in mortgage servicing rights, excess servicing spreads, and agency and senior non-agency mortgage-backed securities, as well as related interest rate hedging activities. The company’s Correspondent Production segment is involved in purchasing, pooling, and reselling newly originated prime credit residential loans directly or in the form of MBS. PennyMac Mortgage Investment Trust was founded in 2009 and is headquartered in Westlake Village, California.

Source: Seeking Alpha PMT

This is how the mREIT describes itself:

PennyMac Mortgage Investment Trust is a specialty finance company that invests primarily in residential mortgage loans and mortgage-related assets. As a real estate investment trust (REIT), our objective is to provide attractive risk-adjusted returns to our shareholders over the long term, primarily through dividends and secondarily through capital appreciation. Our investment focus is on mortgage-related assets that we create through our industry-leading correspondent production activities, including mortgage servicing rights (MSRs). In correspondent production, we acquire, pool and securitize or sell newly originated prime credit quality loans.

Source: PennyMac

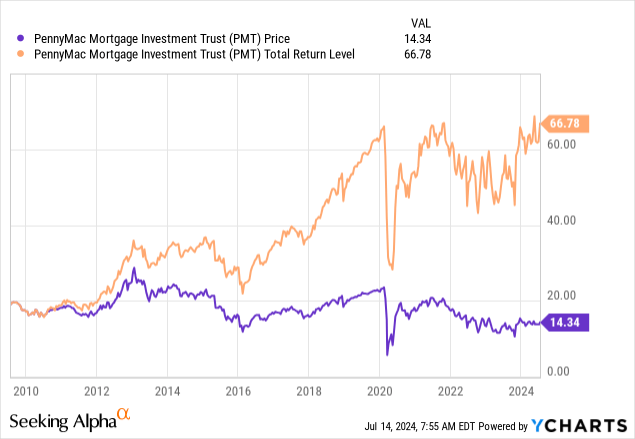

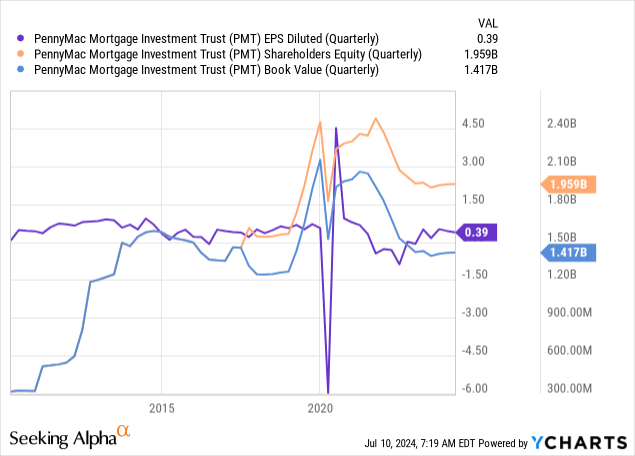

Some recent financial data shows a hiccup around COVID, with some value declines once the FOMC started raising interest rates.

Understanding PMTU

Seeking Alpha Charting

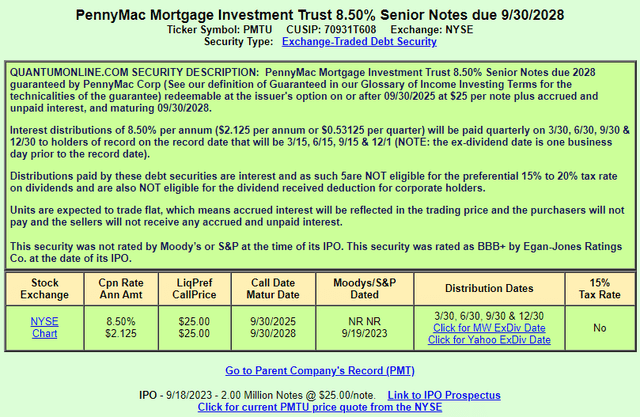

QuantumOnline.com

Notes come with several advantages over preferred stocks, of which PMT investors also have as a choice.

- They rank higher in the event bankruptcy is filed.

- The interest payments cannot be easily skipped.

- Unlike some preferred stocks, the interest rate does not float.

- Notes have a maturity date which only a Term preferred would.

For this Note, its Call protection is limited, ending in September 2025.

Comparing Notes

The two AG Mortgage Notes used are:

- AG Mortgage Investment Trust, Inc. NT 24 (MITN)

- AG Mortgage Investment Trust, Inc. CAL 29 (MITP)

I also included the Eagle Point Credit Company Inc. NT CAL 29 (ECCV) as its features are close and were part of the prior PMTU review.

| Factor | PMTU | MITN | MITP | ECCV |

| Issued | 9/18/23 | 1/23/24 | 5/8/24 | 1/2/22 |

| Size | $50m | $30m | $65m | $87m |

| Coupon | 8.5% | 9.5% | 9.5% | 5.375% |

| Call date | 9/30/25 | 2/16/26 | 5/15/26 | 1/31/25 |

| Maturity date | 9/30/28 | 2/15/29 | 5/15/29 | 1/3/29 |

| Price | $25.40 | $25.15 | $25.10 | $22.60 |

| Yield | 8.37% | 9.44% | 9.46% | 5.95% |

| YTC | 7.14% | 9.10% | 9.26% | 23.64% |

| YTM | 8.05% | 9.34% | 9.40% | 7.89% |

All four Notes are not rated nor eligible for the lower tax rate. This is how I read the data in terms of investing options:

- The clear choice based on YTC is the ECCV but its low coupon compared to other ECC Notes and its preferred stocks make that event very unlikely.

- For longevity, looking at both YTC and YTM, the edge goes to MITP.

- For the current yield, it’s a toss-up between the two ECC Notes. That is also the case when comparing YTM data.

- PMTU has the least amount of time left, with the closest maturity date. If the goal is locking in today’s yields, that is a negative. Ignoring ECCV, it also has the shortest period of Call protection too.

Assuming one rates each Note as having the same level of risk, my current Buy rating would go to the MITP Note, with a Hold for the others.

Portfolio Strategy

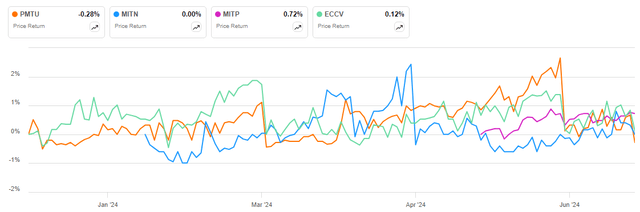

Seeking Alpha Ticker Charting

As the above chart shows me, there hasn’t been much price movement since the end of 2023 when investors started to lose confidence that 2024 could see multiple rate cuts starting as early as March. One set of issuers that are looking ahead are US banks as CD rates peaked in late 2023, with rates trending down slowly since then, especially in the out years. UST investors are seeing the same type of yield curve. When compared to the 5-year yield on corporate bonds rated BBB, investors in these Notes are getting 200-300bps in extra yield, except for ECCV. While one can wait for the first rate cut to pull the trigger, prices will probably already reflect that event before it happens.

Of these four, I have owned ECCV since early 2022 which in hindsight was too soon. Recently, I have added several ETFs like the iShares iBonds 2029 Term High Yield and Income ETF (IBHI) as a way to lengthen the WAM on my portfolio. While neither the yield nor YTM are locked, the risk is less by holding a basket of Notes.

Read the full article here