Welcome to another installment of our BDC Market Weekly Review, where we discuss market activity in the Business Development Company (“BDC”) sector from both the bottom-up – highlighting individual news and events – as well as the top-down – providing an overview of the broader market.

We also try to add some historical context as well as relevant themes that look to be driving the market or that investors ought to be mindful of. This update covers the period through the second week of July.

Market Action

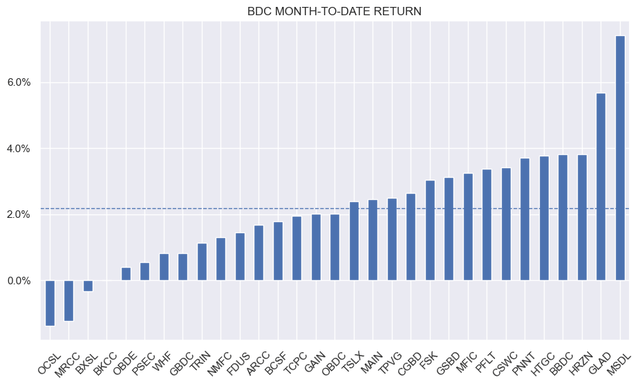

BDCs had a solid week with an 0.8% average total return. Month-to-date, the sector is up 2% with only a handful of companies in the red. MSDL and GLAD are in the lead.

Systematic Income

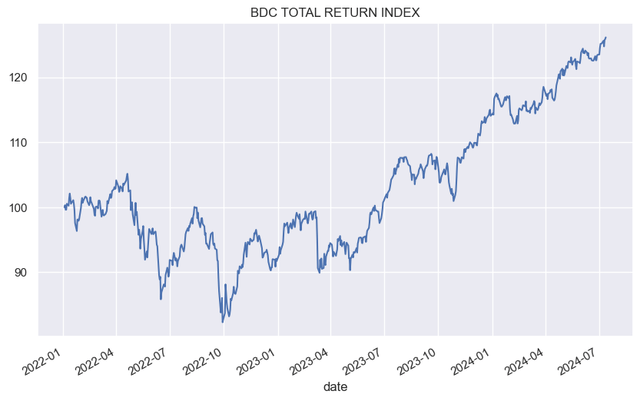

The sector total return index is setting new highs after a short wobble. The performance over the past year has been blistering.

Systematic Income

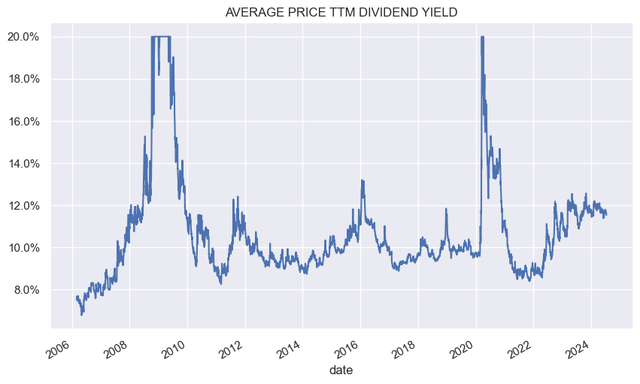

Trailing-twelve month dividend yields remain high and continue to attract interest, supporting prices.

Systematic Income

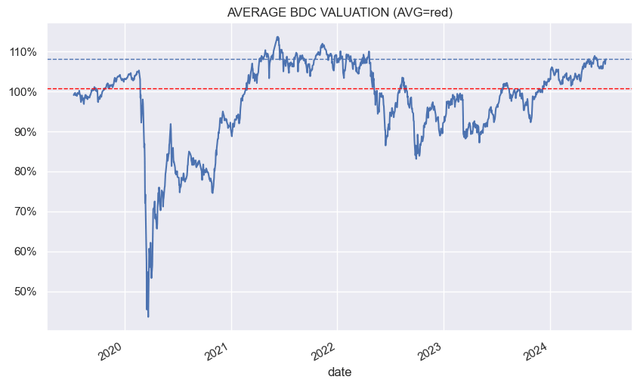

High dividend yields, low level of distressed assets and positive risk sentiment are supporting sector valuations which are near its 5-year peak.

Systematic Income

Market Themes

This week we got a couple of early indicators of upcoming Q2 earnings results.

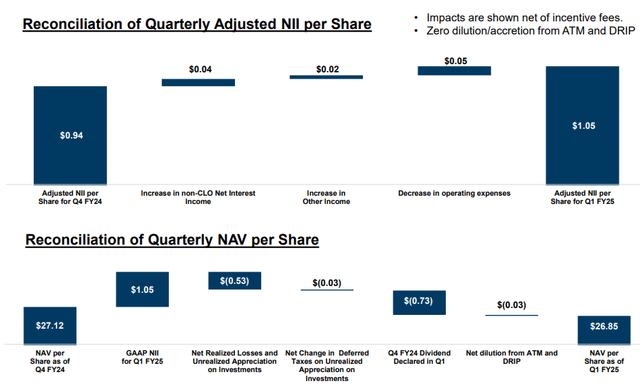

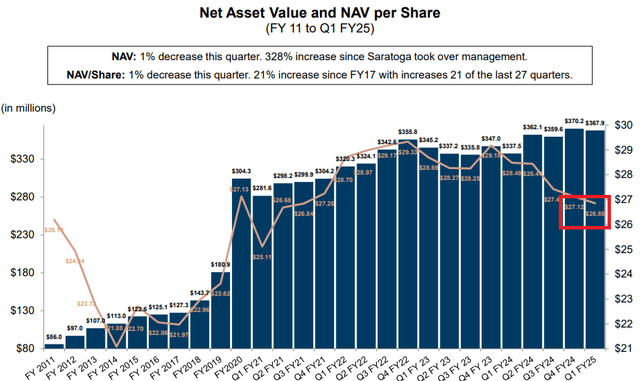

Saratoga Investment (SAR) is already out with a full earnings release due to its odd calendar period. It can be a good canary in the coalmine for the broader BDC sector which releases earnings a few weeks later. The NAV fell about 1%, primarily due to net realized losses on a couple of investments.

SAR

Losses totaled around 2%, however the company retains a lot of income which tends to pull its NAV higher. The total NAV return for the quarter was still a fairly healthy 1.7% or close to 7% annualized.

SAR

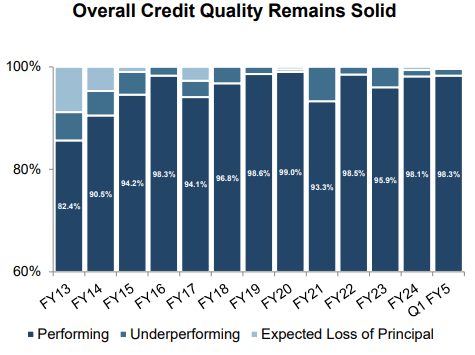

Net investment income increased around 11% from the previous quarter however it stands slightly below the same quarter a year ago. Non-accruals on fair-value were relatively modest at 1.6%. The at-cost figure is pretty high at 4.8% which, together with a descent in the NAV, shows that there has been some accumulated losses and non-performing assets.

SAR

PennantPark (PNNT) also released early guidance, saying core net investment income will come in around $0.21 – a cent lower from the previous quarter. The NAV is estimated to be around $7.525 – a drop of 2.1%. Non-accruals on fair-value fell to 2.5% vs 3% in the previous quarter. It’s likely the company had some net realized losses which drove the drop in both the NAV and non-accruals.

Both SAR and PNNT run at very elevated levels of leverage and are not strangers to occasional losses which means that their Q2 NAV drops are not particularly concerning for the broader sector.

The key result from these early releases is that we are not seeing a step change lower in performance which suggests to us that the overall Q2 reporting results should hold up well and generate solid positive total NAV returns for the sector.

Stance And Takeaways

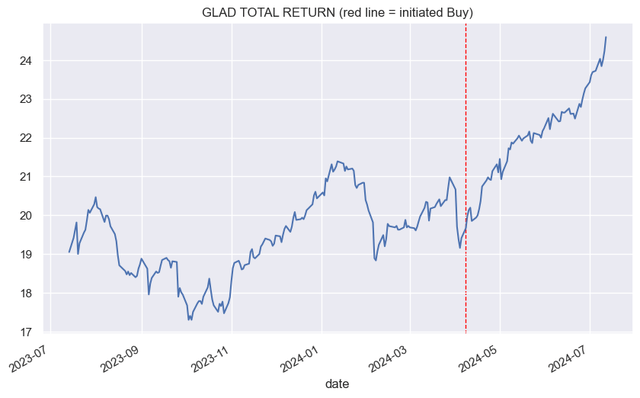

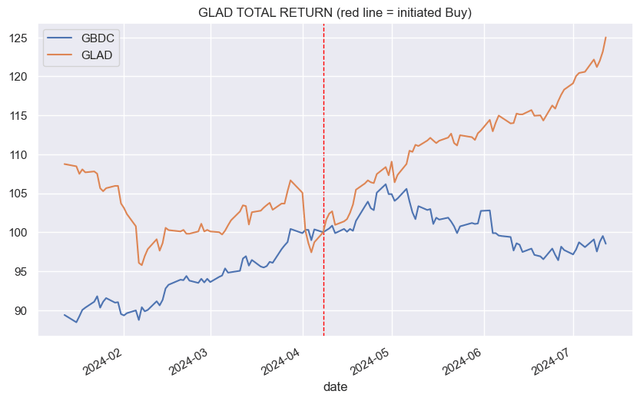

Gladstone Capital (GLAD) has had a great run since early April when we added it to our High Income Portfolio for a total return of around 25%.

Systematic Income

The capital for GLAD came out of the GBDC position which we viewed as somewhat rich at that point. The rotation worked well as the following chart shows – GBDC fell slightly, underperforming the sector while GLAD rallied, outperforming it.

Systematic Income

At this point, GLAD has much less of a margin of safety at its 128% valuation, so we will likely look to exit the position.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Read the full article here