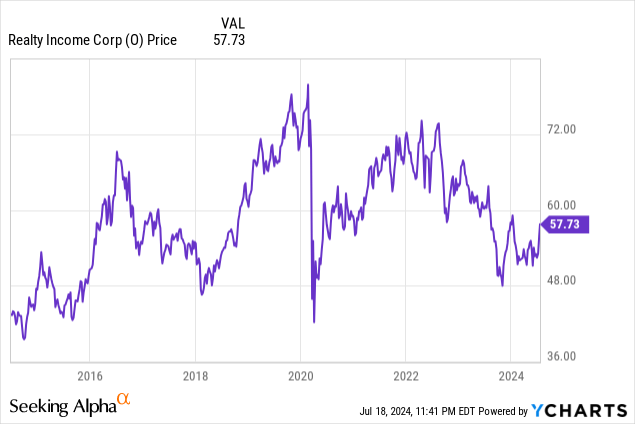

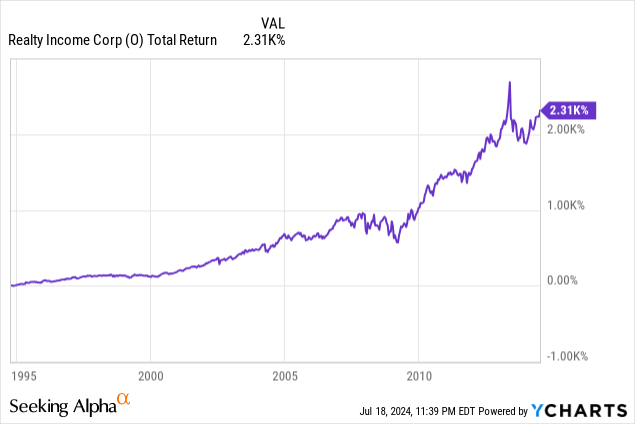

This month marks a special milestone as a shareholder of Realty Income (NYSE:O). I purchased my first shares of O in July 2014, making this my tenth year as a shareholder of the world’s largest net lease real estate investment trust. Since my initial investment, I have accumulated more, making “The Monthly Dividend Company” my largest real estate investment.

My initial investment came following O’s acquisition of American Realty Capital Trust for $3.2 billion in 2013. I believed in management, including newly appointed Chief Executive Officer, John Case.

Over this past decade, the net lease world has changed radically, largely shaping my career in real estate along the way. As I review the past decade, I can’t help but notice the world of O looks very different from the time of my initial investment.

Outside of the company, the world has changed since 2014. We’ve endured a global pandemic which virtually stopped global economies and reshaped modern economics. Interest rates have increased to their highest levels in decades as the federal funds rate increased dramatically. Amazon (AMZN) emerged as a behemoth of online shopping, shaking up the retail industry and brick-and-mortar real estate more broadly. However, these larger environmental factors are not the topic of today’s discussion.

In our past discussion of O, we’ve touched on specific components of their business. The last discussion several months ago, focused on O’s enormous scale, emphasizing how a slowing net lease market would negatively impact forward AFFO per share growth. Our prior coverage included an overview of Realty Income’s business. Perhaps more importantly, we outlined the company’s unparalleled dividend history. For those unfamiliar with O, it may be helpful to review that article before proceeding here.

Today, we are going to take a critical look at O to show just how much the underlying business has been reshaped over the past decade. We will discuss how these changes stand to impact O’s future and forward performance in the net lease sector. This feels appropriate considering 2014 & 2024 have interesting similarities including being on the tail ends of the company’s two largest historical acquisitions. However, much has happened in the interim impacting the company’s business, portfolio, and future.

“O” How You’ve Changed

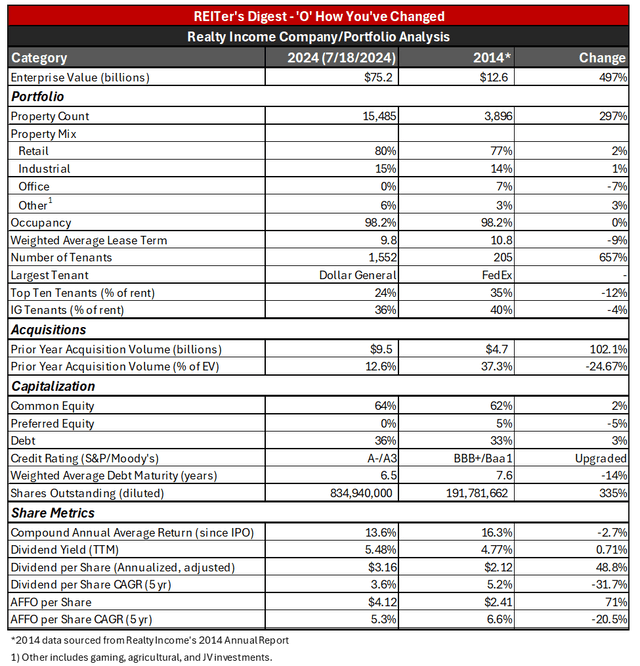

Given O is my largest REIT position, I monitor changes to the company on a quarterly and annual basis. This process includes tracking certain metrics that I find important from a real estate perspective as well as looking through their acquisition and disposition activity on public sources. These categories include enterprise value, portfolio details, acquisition activity, capitalization, and certain share level metrics that O has emphasized over time.

Below is a table with two specific years of data selected. The illustration is intended to compare O’s business today against their business a decade ago. The far right column labeled change quantifies the difference between O as of 2014 and today.

REITer’s Digest, Seeking Alpha

Enterprise Value

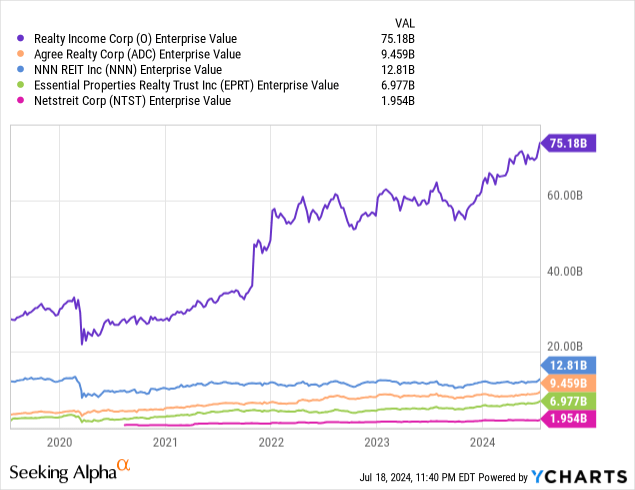

O’s enterprise value growth has been one of the most impressive aspects of the company. Over the past five years, O has been focused on becoming one of the largest landlords in the world. They have been successful, increasing their gross property count by nearly 500% over the past decade. Today, Realty Income’s portfolio by asset count is larger than some of the largest net lease landlords like Agree Realty (ADC), NNN REIT (NNN), Essential Properties Realty Trust (EPRT), and NETSTREIT (NTST) combined.

At $75 billion enterprise value, O has become a top five landlord in the S&P 500 index.

Portfolio

Beyond the sheer number of assets that O has added to their portfolio, the portfolio has also been reshaped. In 2014, the property mix was primarily retail (77%), industrial (14%) and office (6%). The remaining portion of the portfolio was mostly allocated to vineyards as O is one of the largest landlords in Napa County.

Today, the portfolio has remained primarily allocated to retail, increasing the concentration through the acquisition of more retail-specific competitors and voluminous sale leaseback transactions with DG.

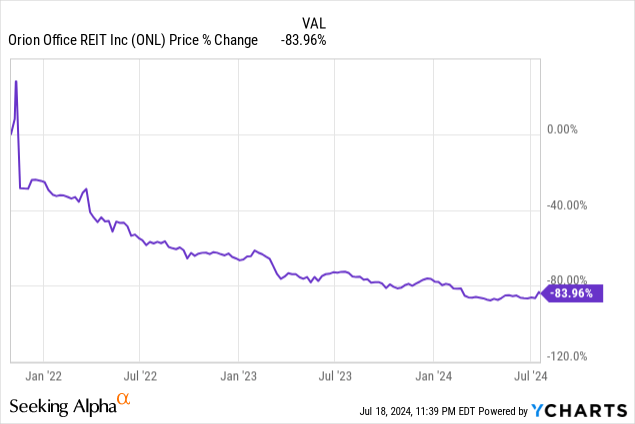

The largest change to O’s portfolio came during the spinoff of their office assets following the pandemic. O spun off their entire portfolio of single tenant, suburban office assets into Orion Office REIT (ONL). Performance speaks for itself as to why O would dispose of these assets.

All in all, O’s portfolio has remained largely the same with a split between retail and industrial, however O has added more diverse assets which we will touch on. The company’s tenant base has expanded significantly and the shift from FedEx (FDX) to Dollar General (DG) as the largest tenant speaks with their realignment towards traditional retail.

The percentage of revenue generated by investment grade tenants has declined considerably in recent years, but aligns roughly with 2014. By my estimation, John Case put more emphasis on having an investment grade portfolio whereas Sumit Roy has focused on building a more diversified tenancy. Further evidence of this assumption is the reduction in revenue generated by the top ten tenants to less than 25%.

Acquisitions

Acquisition activity grew significantly over the course of the decade. As of 2014, the prior year’s acquisitions reached $4.7 billion, by far the largest in the company’s history. The split was $3.2/$1.5 billion between the acquisition of American Realty Capital and organic acquisitions through their traditional pipeline. In all, the year was behemoth for acquisitions reaching nearly 40% of enterprise value.

Last year, O was similarly acquisitive, closing on several large scale transactions in addition to their purchase of Spirit Realty. Even though $9.5 billion was more than twice the volume from 2013, it equated to just 12.6% of enterprise value.

Twice the acquisition volume for much less incremental growth. For an acquisitive REIT like O, this shows that M&A-size activity is having a progressively smaller impact on the portfolio.

Capitalization

O’s balance sheet has remained largely unchanged over the course of the past decade. O uses a stated capital mix of around 2:1 equity to debt to fund new acquisitions. Over time, O has redeemed their outstanding preferred stock and simplified their balance sheet.

Currently, O uses common equity and unsecured debt as their primary capital sources. The debt is long term and fixed rate, insulating O from interest rate risk. O has also received an incremental upgrade from both major credit rating agencies over the past decade. Today, the firm is one of few REITs to earn an A rating, lowering their cost of capital.

Share Metrics

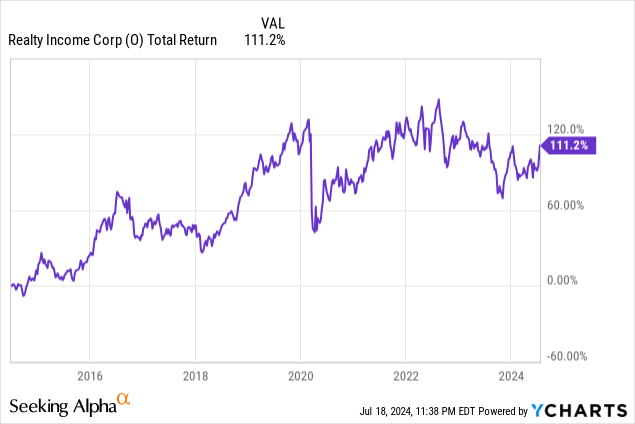

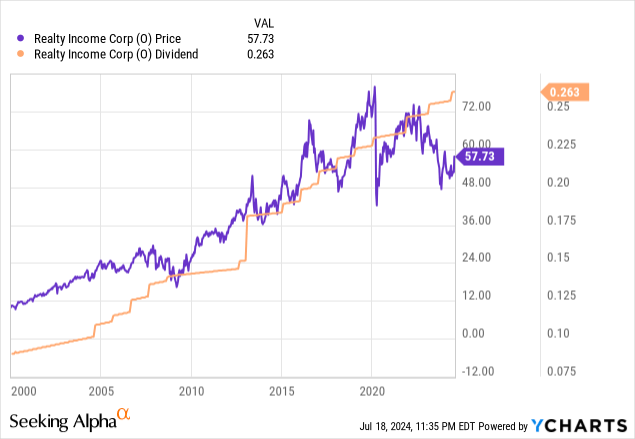

Share level metrics look different for O as compared to a decade ago. Since inception, O’s performance has slowed considerably. The past five years have been particularly rough. Historically, O was beating the S&P 500 powered by significant growth of NAV and the dividend. Upon my initial investment, O had returned 16.3% annually since IPO in 1994 and averaged an AFFO per share growth rate of 6.6%.

Performance has slowed as interest rates rose. The era of free money for REITs has ended causing a systemic slowdown across the net lease sector in particular. Net lease is a longer duration corner of real estate exposing net lease REITs to additional interest rate risk.

O’s enormous scale also means the company has struggled to maintain its growth trajectory by sticking to its core growth mechanisms. As a result, the dividend and AFFO growth rates have both tempered over the past five years.

O has turned to alternative growth mechanisms to keep moving the needle. In particular, the firm has become more aggressive in their M&A ambitions, including two major acquisitions over the past three years. Let’s explore this piece is greater detail.

Who Is O Today? – M&A

In addition to the data above which outlines the quantitative changes to O’s business, the transformation goes far deeper than just growth and maturation of their portfolio and balance sheet. O has expanded their business significantly. First, let’s review the two largest changes via M&A activity.

Over the past decade, O has been a massive buyer of real estate, gobbling up properties far and wide. In addition to the traditional acquisition pipeline of existing assets and sale leasebacks, O has ventured out into bolder opportunities for growth. This includes larger portfolio acquisitions from private investors like CIM, but more notably the acquisition of competing public REITs. The two key examples for O were the acquisitions of VEREIT and Spirit Realty Capital.

In 2021, O announced the acquisition of VEREIT a competing net lease REIT which owned around 3,800 properties. The press release provides detail on VEREIT’s business prior to acquisition. The business was similar and O noted large scale synergies through the combination of the two companies.

VEREIT is a full-service real estate operating company which owns and manages one of the largest portfolios of single tenant commercial properties in the U.S. The Company has total real estate investments of $14.6 billion including approximately 3,800 properties and 89.5 million square feet. VEREIT’s business model provides equity capital to creditworthy corporations in return for long-term leases on their properties.

However, the press release also included details on the strategic rationale behind the acquisition of VEREIT. Two of the first three bullet points refer to building additional scale and the added benefits associated with a growing enterprise, such as diversification and higher weighting in real estate index funds.

Strategic and Financial Rationale

- Immediate AFFO per share accretion. Relative to the $3.465 midpoint of Realty Income’s 2021 AFFO per share guidance, the transaction is expected to be over 10% accretive to shareholders on an annualized, leverage-neutral basis.

- Increased and diversified scale driving growth. The complementary nature of each company’s real estate portfolio results in greater diversification of client credit, industry, and geography, providing further runway for Realty Income to grow in its chosen verticals with best-in-class clients without compromising prudent concentration metrics.

- Enhanced leadership amongst blue chip benchmarks. Upon closing of the merger, Realty Income is expected to become one of the six largest REITs in the MSCI US REIT Index (RMZ) by equity market capitalization and among the top half of constituents in the S&P 500, resulting in increased weighting in major benchmark equity indices and further growing its net lease industry-leading trading liquidity.

Pursuant to the acquisition, O’s portfolio grew by nearly 50% in terms of number of assets, passing 10,000 properties owned. In my opinion, the VEREIT transaction moved O into the category of a mega-REIT following several years of record portfolio acquisitions when rates were low. The merger also saw the expansion of O’s business when various members of the VEREIT team merged into O’s business. The acquisition of VEREIT also spurred the spin-off of ONL.

However, O did not stop there. After acquiring VEREIT, O moved to acquire Spirit Realty Capital in a similar transaction, but this time when rates were significantly higher.

Last year, O announced the acquisition of Spirit Realty Capital for $9.3 billion. Prior to acquisition, Spirit owned 2,034 properties. Spirit Realty was a similarly diversified net lease REIT with a much lower quality portfolio, lower credit rating, and higher equity yield. The rationale behind O’s acquisition was like the VEREIT deal, emphasizing scale and diversification. The emphasis remained on growth as O stressed the transaction would solidify O as the 4th largest public REIT.

Benefits of scale extends to capital markets as Realty Income solidifies position as one of the largest real estate companies in the S&P 500. Pro forma for the merger, Realty Income expects to remain in the top 200 of the S&P 500 index and become the 4th largest REIT in the index, by enterprise value, with a total enterprise value of approximately $63 billion. Further, after giving effect to the merger agreement’s fixed exchange ratio and the company’s current 3-month average daily trading volume, the resulting Realty Income stock is expected to trade approximately $300 million of value on a daily basis. We believe the company’s highly liquid share currency and increasing representation in key benchmark equity indices will create natural demand for the stock and provide Realty Income with meaningful flexibility to continue to effectively and efficiently access the capital markets.

Following the acquisition, O owns a portfolio of over 15,000 properties, which marks another 50% growth since their acquisition of VEREIT. These two acquisitions are important for shareholders of O because it means you are now also an investor in VEREIT and Spirit Realty Capital’s respective portfolios. Net of dispositions, O’s portfolio now owns around 6,000 properties previously owned by VEREIT and Spirit, or around 40% of the current portfolio by property count.

Who Is O Today? – Continued

Looking beyond major M&A activity, O has changed in even more ways which have gone largely under the radar. The firm has added a development platform which provides funding for pre-leased development projects called “build to suit” developments. O does not build properties on a speculative basis, limiting development risk. Instead, O works as a capital partner, fronting money for the tenant who has agreed to lease the property upon completion. In the post pandemic era, this platform was able to capitalize on the development gold rush, particularly in retail and industrial.

O has also added new asset classes which expand far beyond the traditional retail REIT. As the company grows, single tenant retail has become an incrementally smaller component of the business. Finding larger deals means venturing into new asset classes and geographies.

This includes O opening an office in Europe and building out a European investment team. Although O started investing across the pond in the United Kingdom exclusively, the company now owns properties in Spain, Portugal, and other regions as well. O continues to look for new geographies to expand into.

O has even ventured into new property sectors such as their recent acquisition of the Wynn Encore Boston Harbor in an unusual net lease deal for a trophy hotel/casino asset on the east coast. O’s creative ability to use their scale and capital markets prowess to capitalize on new opportunities has benefitted the REIT.

The sale-leaseback transaction with Wynn Resorts is expected to be executed at a 5.9% initial cap rate, includes an initial lease term of 30 years with annual rent growth of 1.75% for the first ten years and the greater of 1.75% or CPI (capped at 2.5%) over the remaining lease term. The lease also includes an additional 30-year option to renew upon expiration. Pending regulatory procedures, the company expects to close this transaction in the 4th quarter of 2022.

O also recently made a more complex investment in the Las Vegas gaming market through a partnership with Blackstone (BX). O agreed to acquire a $950 million interest in the Bellagio in Las Vegas from BX’s Real Estate Income Trust, known as BREIT. The deal marked a complex JV which is radically different from O’s traditional investment in single tenant real estate. Another critical step for O was their recently announced JV with Digital Realty Trust (DLR) which will provide build to suit funding for two data centers located in Northern Virginia.

The Monthly Dividend Company®, announced that they have established a joint venture to support the development of two build-to-suit data centers in Northern Virginia. Realty Income invested approximately $200 million to acquire an 80% equity interest in the venture, while Digital Realty maintains a 20% interest. Each partner will fund its pro rata share of the remaining $150 million estimated development cost for the first phase of the project, which is slated for completion in mid-2024. The build-to-suit facilities were 100% pre-leased to an S&P 100 investment grade client prior to construction and are expected to generate a 6.9% initial cash lease yield upon lease commencement in mid-2024. The facilities are subject to a 10-year initial lease term with extension options and 2.0% annual rent escalators.

This list goes even further as O acquires new assets such as cold storage facilities. Recently, O acquired a distribution center leased to Martin Brower, the primary food distributor for McDonald’s (MCD) according to Triangle Business Journal.

Today, O is a radically different business with a more sophisticated growth engine. Let’s explore what the future may hold for O.

What Does This Mean For O’s Future?

The past decades have been a story of consistency with O. Despite venturing into new businesses including property development, international investments, and new asset classes, O has maintained a strong portfolio of assets. By absorbing competitors of all shapes and sizes, O has become the “net lease index fund” owning a material portion of the entire net lease universe.

My concern around O lies towards the future. As we illustrated, the company’s growth has slowed over the past decade. Traditional growth drivers like acquisitions are no longer moving the needle as a percentage of enterprise value. This means changing share level metrics will also become more difficult as larger transactions become necessary. As evidence of this, AFFO share growth has already slowed, despite O continuing to acquire new properties as fast as their pens can sign on the dotted line. This reflects in the growth of the dividend over time, which has similarly slowed.

The acquisition of Spirit Realty marked a significant shift in my outlook for O. It showed a shift from a concerted focus on high quality tenancy, to a larger diversified approach. By absorbing the entire net lease universe, adverse credit events become less impactful and the company can achieve a more attractive risk profile.

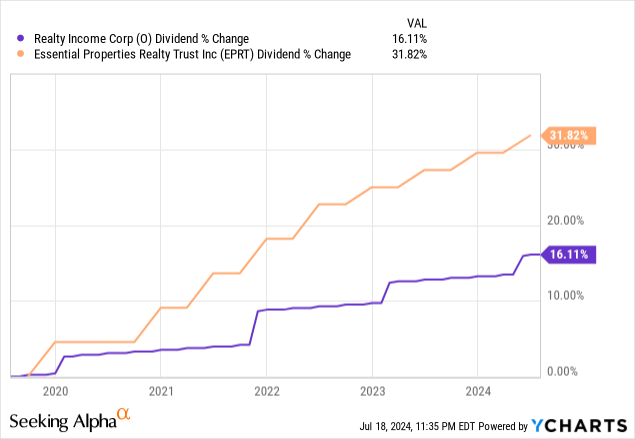

There are other net lease REITs, such as Essential Properties Realty Trust (EPRT) which have better growth prospects via a smaller balance sheet than O. Over the past five years alone, EPRT’s dividend growth rate has doubled O’s. However, those seeking a behemoth REIT that has stood the test of time should look no further than O.

I will continue to hold my shares of O, however I believe there are better opportunities to recreate the magic of O’s golden era.

Read the full article here