Buying a stock is easy to do, especially in today’s electronic marketplace, where all you need is a computer or smartphone to hit the buy button while waiting for a latte at Starbucks (SBUX).

With each purchase comes plenty of hopes and dreams of a better future and that’s what makes the stock market so engaging for investors. Anybody who says to take emotions out of buying a stock is probably lying to themselves, because all decisions are emotionally driven, no matter how rationally-minded the investor is.

When you buy a stock, you hope that management will be competent act in the best interest of shareholders, you hope that the business model will prove durable, and you hope that you didn’t pay too much for it.

While you may have all the due diligence in the world, you would still hope that your investment thesis will pan out, because investing is a game of managing what you know while being prepared for uncertainties.

What’s probably harder for most investors than buying a stock, however, is figuring out when to sell a stock. Counter to why buying a stock is so easy, for the aforementioned reason of having hope that things will work out the way you believe, selling a stock comes with the fear of missing out on potential gains down the road.

That’s likely why Warren Buffett’s favorite holding period is ‘forever’ as that takes the guesswork out of when to sell a stock. What makes it even easier to hold onto a stock are dividends, as it’s ideal for a company to pay you for holding onto it as a rightful part owner of a business.

This way, price volatility becomes less of a concern, so long as the investment thesis stays intact. Perhaps that’s why Berkshire Hathaway’s (BRK.A)(BRK.B) top 5 holdings, Apple (AAPL), Coca-Cola (KO), Bank of America (BAC), American Express (AXP), and Chevron (CVX), all pay dividends.

As Robert & Sam Kovacs so aptly put it in a recent brilliant piece, dividends do matter, because there’s nothing like getting cash payment from an asset that you own, as a bird in hand is better than two in the bush.

That’s why I gravitate toward income stocks, because they take pressure off having to time sales, so that I can focus more time on finding undervalued opportunities using dividend income as dry powder to make purchases. Let’s get started with the following 2 picks, which offer great recurring income!

#1: Crescent Capital BDC

One such stock that I like is Crescent Capital (CCAP) and externally-managed BDC that currently trades at a discount to net asset value. CCAP is one of the few BDCs on the market today to have international exposure with 8% of its portfolio investments being in Europe, 2% in Australia and New Zealand, and 1% in Canada, with the remainder being in the U.S.

CCAP invests primarily in defensive industries with 84% of its portfolio being in non-cyclical sectors. It’s also diversified with a portfolio fair value of $1.6 billion spread across 183 different companies. Plus 98% of investments are floating rate, which means that it’s seeing higher earnings due to the current rate environment.

Risks to CCAP stem from a potential economic downturn, which could impact all BDC investments. Another risk is potential for lower rates going forward, but that may not come until September, and even then, rates would still be meaningfully above where they were a two years ago.

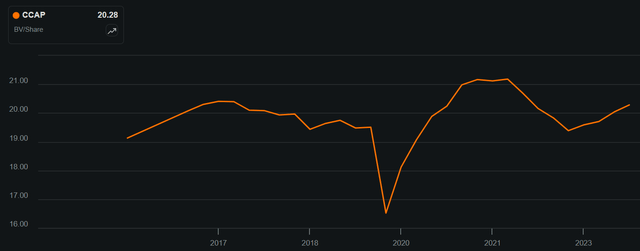

CCAP has demonstrated its ability to grow or preserve its NAV in both high and low interest rate environments since 2016. As shown below, NAV per share has rebounded since the end of 2023 as portfolio values have recovered from lower mark-to-market valuations due to higher rates.

CCAP NAV/Share (Seeking Alpha)

CCAP’s NII per share grew by $0.09 on a YoY basis to $0.63 in Q1 2024, and this translates to a strong NII-to-Regular Dividend coverage ratio of 1.5x, and a still strong 1.19x when including the special $0.11 dividend paid just last month.

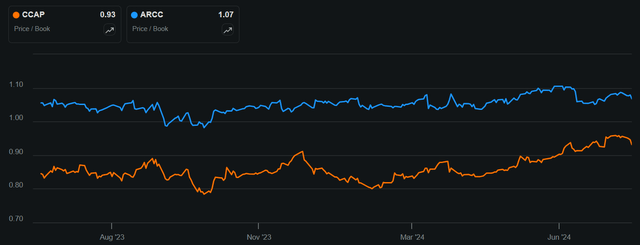

At the current price of $18.89, CCAP trades at 7% discount to NAV, comparing favorably to the 7% premium that industry bellwether Ares Capital (ARCC) currently trades at.

It’s worth noting that CCAP does have a slightly higher non-accrual rate of 0.9% of fair value compared to 0.6% for ARCC. However, the well-covered regular dividend plus extra potential from special dividends, resulting in an 11% TTM yield, and the wide NAV per share disparity more than makes up for it. This makes CCAP an attractive ‘Buy’ at present.

CCAP vs ARCC Price-to-NAV (Seeking Alpha)

#2: Canadian Natural Resources

Another income favorite of mine is Canadian Natural Resources (CNQ) which offers a very different business model from CCAP, thereby offering automatic diversification.

CNQ is the largest oil and natural gas producer in Canada with a significant presence in energy rich oil sands. This compares favorably to many U.S. producers like Exxon Mobil (XOM) and Occidental Petroleum (OXY), which operates depleting shale wells that can see a decline of as much as 70% in a year.

Unlike shale wells, oil sands are long-lived assets that are costlier to set up initially, but offer recurring income streams that require far less capital expenditures to maintain the same level of throughput.

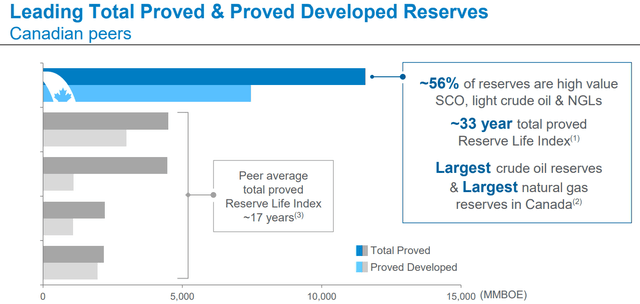

Most (56%) of CNQ’s reserves are high value with 33 year total proved reserve life. As shown below, this makes CNQ a leader amongst its Canadian peers for having the largest crude oil and natural gas reserves.

Investor Presentation

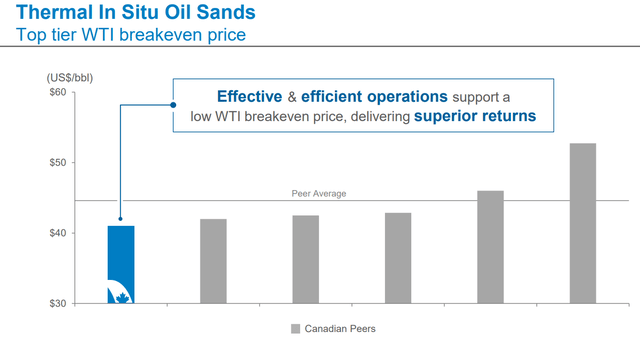

CNQ is seeing strong operating fundamentals, with total production averaging 1.33 billion barrels of oil equivalent per day during Q1 2024. Thermal and situ oil sands production increased by 10% over the prior year period to 268K bpd, and effective cost management drove a 12% YoY decline in operating costs in those regions.

This further builds upon CNQ’s cost leadership. As shown below, CNQ carries the lowest breakeven point amongst its Canadian peers at just over $40 per barrel.

Investor Presentation

The aforementioned low breakeven point compares favorably to the current WTI Crude Oil Spot Price, which as shown below, continues to sit at an elevated level compared to the past 10 years, at $83.22 presently.

YCharts

Risks to CNQ include its sensitivity to economic downturns, which could suppress oil demand and prices. This is considering CNQ’s role as an upstream producer that’s subject to commodity price risk. Other risks growth in electric vehicles.

However, EV demand has been slowing, and Ford (F) this week announced its intent to build gasoline-powered heavy duty trucks at a Canada site that originally intended to build EVs, further supporting the thesis that ICE, hybrids, and gas-powered cars will coexist well into the future.

Notably for income investors, CNQ has a stated policy of returning 100% of its free cash flows to investors so long as its net debt is around CAD $10 billion. This is what CNQ is doing is its net debt currently $9.9 billion, and makes sense considering CNQ’s low maintenance CapEx costs due to its exposure to zero-decline oil sands with long-lived reserves.

CNQ has raised its dividend for 24 consecutive years and currently yields a respectable 4.1%. While the yield isn’t particularly high, it’s worth noting that CNQ has raised its dividend at a 21% CAGR since 2008, and has a 5-year CAGR of 22.4%. It also comes with a safe payout ratio of 52%.

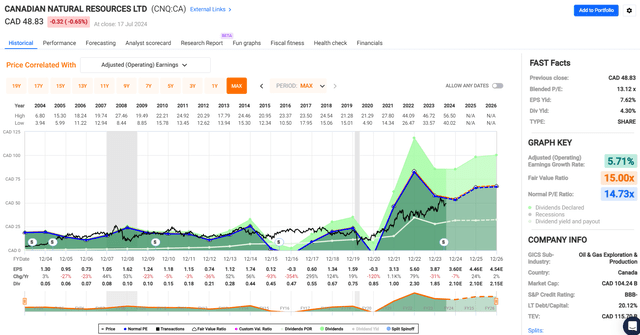

Lastly, I find CNQ to be attractive at the current price of $35.64 with a forward PE of 13.4, sitting below its normal PE of 14.7, as shown below.

FAST Graphs

This valuation puts CNQ on par with that of XOM’s 13.4x PE, and ahead of Chevron’s (CVX) 12.9x PE. I believe CNQ deserves to trade at a premium to its American peers due to its higher quality and long-lived asset base.

Sell side analysts who following the company have an average price target of $40.74 on CNQ and estimate 22% EPS growth next year, which could be achieved should oil prices stay elevated, and its expansion plans in the oil sands and plan to increase bitumen (asphalt) production to 195K barrels per day pan out. As such, CNQ remains a terrific long-term growth play with a great dividend growth kicker.

Investor Takeaway

Income stocks like Crescent Capital BDC and Canadian Natural Resources offer a compelling opportunity for long-term growth and steady returns. CCAP, with its diversified and primarily non-cyclical investment portfolio, provides an attractive dividend yield supported by its robust net investment income.

Meanwhile, CNQ benefits from its extensive oil and natural gas reserves, low operational costs, and consistent dividend growth, making it a solid dividend stock backed by strong free cash flows.

Both stocks allow investors to focus on capitalizing on undervalued opportunities while receiving recurring income, aligning with the strategy of using dividends as dry powder for personal use and/or future investments.

Read the full article here