Since I last wrote about the Australian iron ore miner Rio Tinto (NYSE:RIO) in March, its share price is up by 4%. This isn’t a big increase by any stretch, of course. It’s even lesser than the 10% increase seen in the S&P Metals & Mining Select Industry Index during this time.

It does, however, need to be recognised that by mid-May, the stock had seen a much bigger increase of 20%, before correcting significantly since on a run up in base metal prices. As these prices saw some correction, so did RIO.

Here I take a closer look at whether there’s a case for more sustainable price rise for the stock now, based both on its own production and commodity prices.

Prospects for iron ore

Iron ore is the key commodity to consider for Rio Tinto, considering that it contributed almost 84% of the company’s underlying EBITDA in 2023. If follows then, that much of the company’s fortunes are linked with those for the commodity, which are looked at in some detail here.

Production and projections

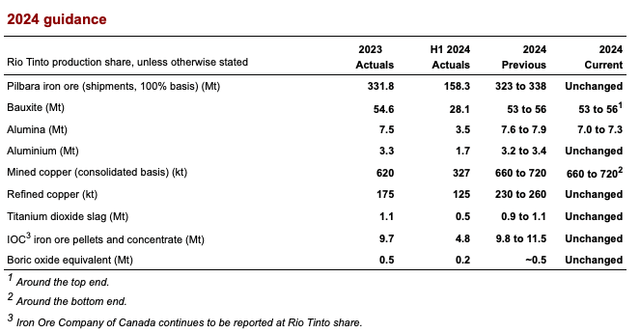

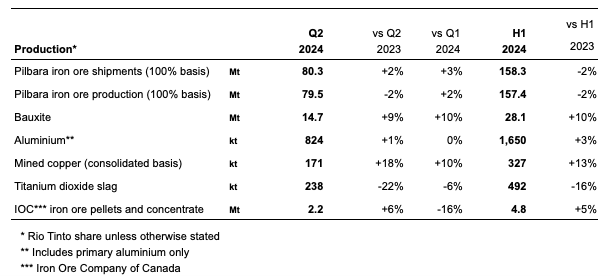

As far as production goes, the company’s important Pilbara iron ore has seen no change in guidance up to H1 2024. At the midpoint of the range (see Table 1 below), there’s expected to be little change in production in 2024 from last year as well. However, after a slight decline of 2% year-on-year (YoY) in H1 2024 (see Table 2 below), it may well come in at the lower end of the range.

On the other hand, a 5% YoY increase in its iron ore pellets and concentrate production is some consolation. It’s relatively tiny in production terms, though. Essentially, unchanged to slightly lower production for iron ore can be envisaged for 2024.

Table 1 (Source: Rio Tinto) Table 2, Production, H1 2024 (Source: Rio Tinto)

Iron ore price

At any other time, unchanged production might not have mattered as much but with an underwhelming outlook for iron ore prices, it does matter now. The commodity’s price has already disappointed in 2024 so far, with an over 20% price decline and the price prospects don’t look encouraging either. At best, it’s expected to end the year flat. For details on iron ore prices please look at my recent article on BHP (BHP) here.

Prospects for Aluminium and Copper

The prospects for aluminium and related products, which accounted for almost 10% of the company’s underlying EBITDA in 2023, are better. Both bauxite and aluminium production was up in H1 2024, and guidance for them remains unchanged too. The only exception is alumina, which is now expected to see slightly lower production than last year.

It’s also encouraging that aluminium’s price on average in H1 2024 has been higher YoY (see chart below) as the base metal saw a temporary price spike in April following the US and UK banning Russian metal imports.

Source: Trading Economics

Much like aluminium, copper price too saw higher price on average in H1 2024 compared to H1 2023. Even though the metal contributed around a relatively small 8% of the underlying EBITDA in 2023, in addition to aluminium, this adds in terms of positive trends for Rio Tinto. Also, copper production has been positive, with a 13% YoY increase in H1 2024 and guidance has remained unchanged for it too. In sum, copper is a bright spot for the company in the past half year.

Financial outlook and market multiples

Broadly speaking, however, aluminium and copper can do only as much to prop up the company’s financials. With iron ore’s trends weak, the company’s H1 2024 numbers due later in the month are likely to show weakness.

In fact, with iron ore prices expected to stay static at their 2023 levels, at best, the financials could stay sluggish for the remainder of 2024 as well. This is also mirrored in analysts’ estimates on Seeking Alpha, which expect revenue to decline by around 2% this year and the EPS to stay flat.

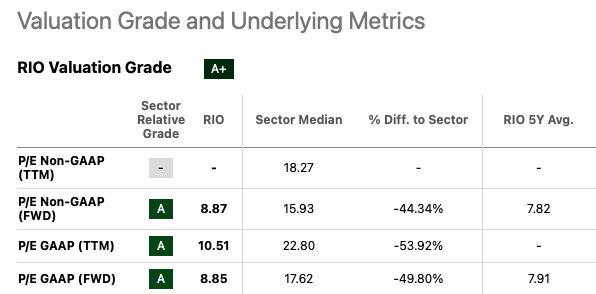

Even then, if the stock’s market multiples were low, there could still be a buy case for it. That’s not so, either. Its forward price-to-earnings (P/E) ratios are higher than the five-year averages (see table below). In fact, even these look good compared to my estimates, which assume that the company’s net margin remains constant at last year’s level of 18.6%, and the revenue declines as indicated by the average of analysts’ estimates. This results in a forward non-GAAP P/E of 11.1x.

Source: Seeking Alpha

Essentially, it’s hard to make a Buy case for Rio Tinto from the price perspective. That said, it’s worth considering the dividend yield. The forward dividend yield, in particular at 8% is impressive.

Though, whether it makes up for the potential weakness in the price, remains to be seen. In the past three years, the total returns on the stock have been just 5.7%, dragged down significantly by a 17.4% decline in price. The commodity cycle isn’t just in a weak place right now, but it’s unlikely to see a significant upturn anytime soon as well.

This is largely due to China, the biggest metals’ consumer, which hasn’t seen the hoped for pickup in demand. And the US economy expected to continue losing momentum as well, it could be some time before metal prices start shining again.

What next?

For long-term investors looking for reliable dividend income, Rio Tinto is still a good stock to buy. However, it’s hard to make a Buy case for it in the short-to-medium term looking at the commodity price outlook, its own production guidance and the market multiples.

I believe right now, there’s a risk to capital from buying the stock. There could be short term upticks based on news flows, as seen in April and May, as base metal prices saw an increase. But its unlikely to be sustained. I’m reverting Rio Tinto to Hold. This can change, if there are any unexpected positive developments on the macroeconomic front, but so far that appears unlikely.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here