The Tobacco Investment Thesis Remains Robust In IMBBY

We previously covered British American Tobacco p.l.c. (BTI), Altria (MO), and Philip Morris (PM), discussing their combustible and alternative tobacco offerings during the secular tobacco use decline.

For this particular article, we will be looking at Imperial Brands (OTCQX:IMBBY) (OTCQX:IMBBF) and sharing our findings about the stock, continuing the theme surrounding the tobacco sector.

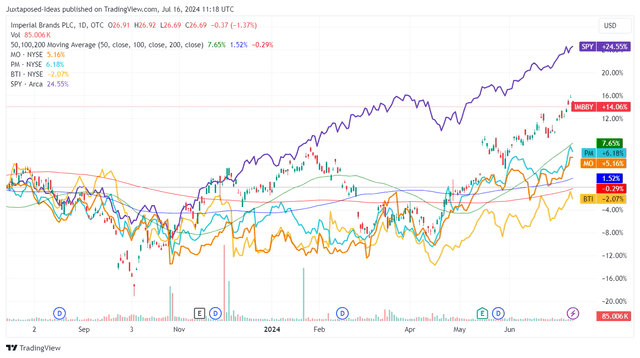

IMBBY 1Y Stock Price

Trading View

For now, IMBBY has charted an impressive 1Y stock price return compared to its tobacco peers, one rarely observed in the sector due to the secular decline in tobacco use.

Much of the stock’s tailwinds are attributed to numerous factors: the company’s ability to grow tobacco share in priority markets, expand profitability, return great value to long-term shareholders through share repurchases and dividend payouts, and finally, its inherent undervaluation despite the consistently lower sales volume.

For reference, by Half Year 2024 [HY2024], IMBBY has already reported impacted tobacco volumes of -6.3% YoY, with the higher net revenues of +2.3% YoY only attributed to higher pricing at +8.6% YoY.

The same trend has also been reported by numerous tobacco companies and the World Health Organization [WHO], with it apparent that more consumers are preferring vaping/ e-cigarette options and/ or cannabis.

While IMBBY has attempted to enter the alternative tobacco market with Next Generation Products, the segment only comprises 3.9% of its HY2024 net revenues (+0.5 points YoY) while remaining unprofitable at -37.7% in adj operating profit margins (+13.5 points YoY).

So, why has the wider market rewarded the tobacco stock so handsomely in stock returns thus far?

1. Growing Market Share In Priority Markets

IMBBY has been very strategic in their execution, in which it does not aim to be the largest tobacco company in the world, as reiterated by the management in the recent JP Morgan Consumer CEO call series (bold for clarity):

Imperial is unique and it’s a reflection of our smaller size that virtually five markets drive more than 70% of our profitability… To be clear, as a management team it is also easier to stay very close to 5 vs. when you have to stay close to 10 or 20. But I think what’s also important, that when we planned out our strategy the financial model is based on us holding our share, maintaining the share as an aggregate between these five markets. So, the ambition is not to grow share in these markets consistently. (Imperial Brands)

From these excerpts alone, it is apparent that IMBBY prefers to be smaller and focused in their execution, with the strategy already bearing fruit. The company has reported a relatively stable tobacco share of:

- 32.2% in Australia (+0.1 points YoY/ -0.4 points from FY2019 levels of 32.6%),

- 26.9% in Spain (+0.5 points YoY/ -2 points from FY2019 levels of 28.9%), and

- 10.8% in the US (+5 points YoY/ +2 points from from FY2019 levels of 8.8%),

- well balancing the moderate declines observed at 18.1% in Germany (-0.25 points YoY/ -3.5 points from FY2019 levels of 21.6%) and

- 38% in the UK (-0.4 points YoY/ -2.6 points from FY2019 levels of 40.6%).

As a result of these developments, it is apparent that IMBBY’s strategy has been a net positive indeed, especially since its Next Generation Products have been growing in adoption – representing 7% of its net revenues in the EU.

At the same time, readers must note that the company recently entered the oral tobacco market in the US with ‘zone’ in early 2024, allowing it to tap into a fast growing market while directly competing with PM’s Zyn and BTI’s Velo.

As discussed in our previous BTI article here, with oral tobacco increasingly popular in the US and PM’s Zyn unable to meet the growing demand through the end of 2024, we believe that competitors may benefit from the interim shortage, as observed in BTI Velo’s growing market share.

This is especially since the oral tobacco market is expected to grow from $6B in 2023 to $18B by 2027, expanding at an accelerated CAGR of +31.6%, allowing newcomers such as IMBBY’s ‘zone’ to establish a foothold in the intermediate term

2. Expanding Profitability – Leading To Its Robust Shareholder Returns

The Consensus Forward Estimates (in $)

Tikr Terminal

Despite the lower sales volume and stable tobacco market shares, IMBBY continues to deliver its medium term guidance of “adjusted operating profit growth to support a mid-single-digit constant currency CAGR over FY23-FY25.”

The same has been observed in its 2Y adj EPS growth at a CAGR of +6.3% by FY2023 and adj EPS growth at +7.7% YoY at constant currency in HY2024. These numbers imply that the consensus forward estimates of adj EPS growth at a CAGR of +7.3% through FY2025 is not overly aggressive indeed.

IMBBY’s dividend investment thesis remains more than safe as well, based on its growing 12-month cash flow of £3.72B (+26.5% sequentially/ inline to FY2019 levels) and annualized dividend obligation of £1.82B (inline sequentially/ -5.2% from FY2019 levels, partly attributed to lower share counts).

Combined with the recent interim dividend increase by +4% and the target adj net-debt-to-EBITDA ratio of 2x by the end of 2024 (compared to the current 2.5x), it is apparent that the management remains confident about its ability to generate robust profitability ahead.

Lastly, IMBBY continues to reiterate £1.1B in FY2024 share repurchases, with 57.4M shares or the equivalent 6% of its float already retired over the LTM, exemplifying the management’s competent use of cash flow with it also boosting the adj EPS growth.

3. IMBBY Is Inherently Undervalued – Offering Opportunistic Investors With The Dual Pronged Returns

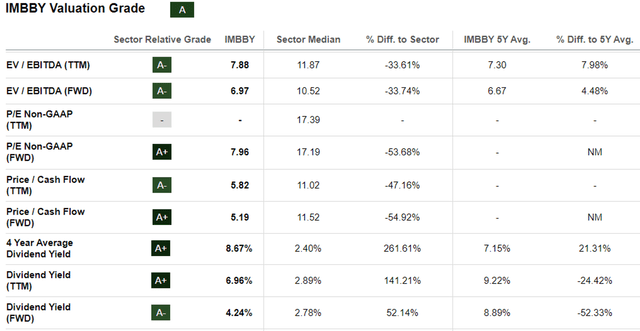

IMBBY Valuations

Seeking Alpha

For now, the market’s quiet optimism surrounding IMBBY’s competent prospects has been reflected in the recovery of its FWD P/E valuations to 7.96x, up from the 5.49x recorded in the October 2023 bottom, though still a distance from its 3Y pre-pandemic mean of 11.56x.

As a result of its robust mid-single-digit constant currency growth, we believe that IMBBY is still cheap at FWD P/E of 7.96x, compared to BTI at FWD P/E of 6.90x/ adj EPS growth at a CAGR of +2.6%, MO at 9.36x/ +3.7%, and PM at 16.62x/ +8.3%, respectively.

As a result of its overly discounted valuations for the constant currency growth rates, we believe that IMMBY’s FWD P/E valuations may eventually be upgraded nearer to its historical FWD P/E of ~11x, upon the successful monetization of its Next Generation Products.

Combined with the consensus FY2025 adj EPS estimates of $3.56, we are looking at a bull-case 2Y price target of $39.10, with it offering an excellent upside potential of +46.4% despite the stock’s recent rally.

So, Is IMBBY Stock A Buy, Sell, or Hold?

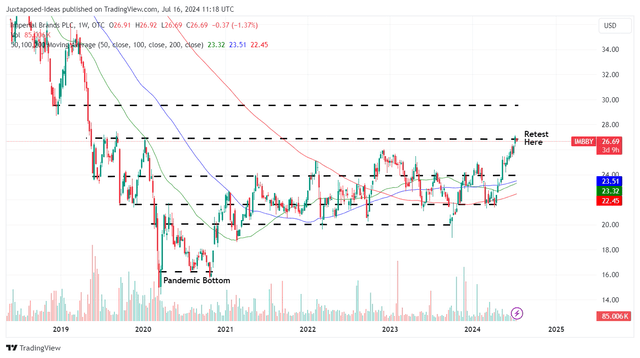

IMBBY 5Y Stock Price

Trading View

For now, IMBBY has already charted an impressive recovery of +37% since the October 2023 bottom, well outperforming its peers, such as BTI at +7%, MO at +14%, PM at +15%, and the wider market at +32%.

And it is for this capital appreciation reason that IMBBY’s forward dividend yields have appeared to decline to 4.24%, compared to its 4Y average of 8.67%, though still decent compared to BTI at 9.23%, MO at 8.21%, and PM at 4.95%.

If anything, we believe that long-term IMBBY investors are happy about this recent development, since it implies robust total returns through capital appreciation and dividend payouts.

As a result of the still attractive risk/ reward ratio and the three promising factors discussed above, we are initiating a Buy rating for the IMBBY stock.

For now, with the CBOE Volatility Index rising and the wider market pulling back from the recent generative AI heights, we may see traders take some profits off the table with the tobacco stock potentially pulling back afterwards.

As a result, interested investors may consider monitoring the stock’s movement for a little longer before adding according to their dollar cost averages/ risk appetite for an improved margin of safety.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here