Investment Thesis

I previously covered Masco Corporation (NYSE:MAS) last year with a buy rating. Despite the tough macroeconomic environment impacting its results since then, the stock has performed well, gaining over 30% thanks to its good margin performance. While I don’t have high expectations around revenue recovery going into Q2 earnings, I expect to hear increasing commentary about stabilizing demand trends and sales bottoming, which should pave the way for eventual recovery towards the end of this year or early next. The company is also gaining market share and benefiting from strength in its PRO paints channel and from secular demand trends in the repair and remodeling sector, driven by aging housing stock and strong home equity levels.

On the margin front, the company should benefit from the carryover impact of price increases, easing input cost inflation, volume leverage, and cost-saving initiatives. With EPS growth expected to return to low double digits starting next year (consensus estimates) and a dividend yield of ~1.6%, I believe the stock can give a low teen CAGR over the coming years. Given the accelerating revenue growth and continued margin expansion prospects, I rate the stock a buy.

Masco’s Revenue Analysis and Outlook

After experiencing good demand during the pandemic, the company’s end markets started slowing down in mid-2022 due to rising inflation, high interest rates, and tight spending. The lower demand continued in the first quarter of fiscal 2024 as well.

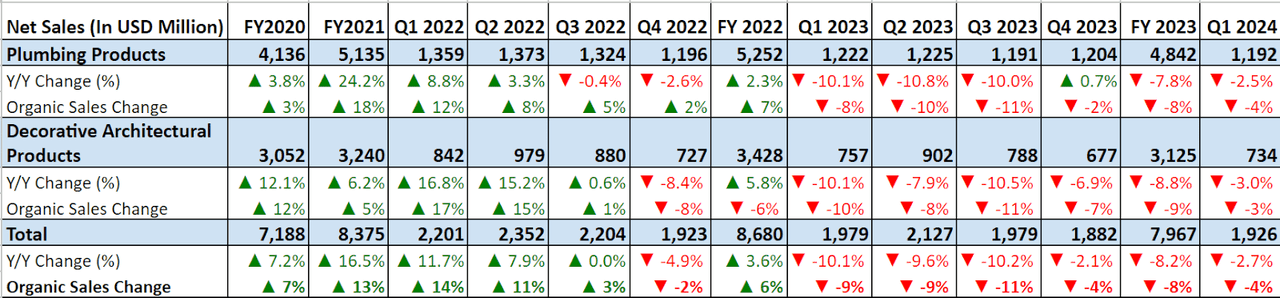

In the first quarter of fiscal 2024, the company’s sales were impacted by continued softness in end market demand due to lower repair and remodel projects in a persistent inflationary and high interest rate environment. This resulted in lower volumes for plumbing and hardware products. This was partially offset by price increases and good demand for paint and coating. As a result, sales declined by 2.7% Y/Y to $1.92 billion, Excluding a 1 percentage point benefit from acquisitions, organic sales declined by 4% Y/Y, reflecting ~4 percentage point impact from lower volumes, partially offset by ~1 percentage point benefit from price increases.

On a segment basis, the Plumbing segment’s sales declined by 2.5% Y/Y and by 4% Y/Y excluding currency headwinds and benefits from acquisition. Lower volumes driven by lower demand for plumbing products in North American and International markets resulted in a sales decline in this segment. In the Decorative Architectural Product segment, sales declined by 3% Y/Y due to lower pricing benefits and lower volumes for DIY products, partially offset by volume growth within PRO paint and coating products due to good demand.

MAS’s Historical Revenue (Company Data, GS Analytics Research)

Looking forward, the company is set to report its Q2 2024 earnings on July 25th and I don’t have very high expectations around sales recovery in Q2 given the high interest rates and tough macroeconomic environment continued in the quarter. However, I expect to see increasing signs of stabilizing end-market demand and revenue trends not getting incrementally worse. This should pave the way for an eventual recovery towards the end of this year or early next year as the interest rate cycle starts reversing.

To give a recap, Masco saw good demand for its products due to increased repair and remodeling projects during the pandemic as people prioritized home improvements. This good demand continued in 2021 and the first couple quarters of 2022 due to the pull forward of demand, benefiting sales. However, by the middle of 2022 the demand for the company’s product began to normalize as the economy fully reopened. In addition, rising inflation, a high interest rate environment, and tight consumer spending further impacted the demand.

While lower demand has been dragging sales since then, there have been some signs of stabilization in the North American markets, which are seeing orders for repair and remodeling projects starting to return to their normalized seasonality.

In a recent J.P Morgan Homebuilding & Building Products Conference, talking about stabilization, CFO Richard Westenberg commented,

… importantly, what we’re seeing in the business is, as I mentioned earlier, is stabilization. And so, the industry and our business has declined at a decreasing rate. And what we’re seeing is some favorable trends, not only in stabilization, but some opportunities. So I think just to mention it as a data point, in Q1, in North America, our Delta Faucet Company wholesale business actually grew and Delta grew overall in Q1. So that’s shaping up to be favorable and we’re seeing that slowly manifest itself across the industry. I think it’s a matter of timing. As I mentioned, the fundamentals are strong. And so, it’s not a matter of if, but when. And so, we’re tracking it very closely. Things are encouraging. I mean, we see 2024 really as a kind of a transition year. And we see things stabilizing here as we progress during the course of the calendar year.”

So, I believe we are close to the bottom and should see a recovery in North American sales over the next few quarters.

On the international side, demand continues to be lower due to a weak Chinese and European market. However, I believe as we progress, forward sales should benefit from easing Y/Y comparisons. International organic sales declined 3% Y/Y in Q1 2023, 8% in Q2 2023, and 11% in Q3 2023, implying easing comps in the coming quarters.

Moreover, management in the Q1 2024 earnings call and the recent J.P. Morgan Home & Building Product Conference commented that the company is seeing market share gain internationally despite a declining R&R industry. Here are some relevant excerpts,

Hansgrohe and that team there (international market) has done a phenomenal job and there’s no question, while it’s certainly difficult to pin down in a particular quarter the size of the market when you’re in well over 100 countries. But clearly, we’re outperforming our major competition in Europe and continuing to gain share. So, we expect that to continue to happen. The business is performing very well. There is a little bit more signs of stability in Germany and Central Europe than we’re seeing in China. So, we think China is lagging a little bit. But we expect to continue to gain market share against the backdrop of International markets that will be down low- to mid-single-digits.”

– Keith J. Allman, CEO (Q1 2024 earnings call)

Second, is in the international space, Hansgrohe specifically. And in terms of that, we’ve seen performance against our primary competitor really outperform in terms of our performance on a global basis and specifically in Europe. And although the industry is down, as I mentioned before, we’re gaining share in that environment, which is encouraging and sets up well when the market does turn to grow.”

– Richard Westenberg, Masco CFO (J.P Morgan Conference)

I expect international sales to hit bottom in the second half of the year, and it should also support overall demand and sales recovery as we exit the current year.

In addition to stabilizing end market demand and easing comps, the company should also benefit from improved offerings on the PRO side. Over the last three years, the company has consistently launched new innovations, improved delivery convenience through more convenient and flexible delivery options like online delivery, pickup in-store, and onsite delivery, and expanded its loyalty program. In the last quarter as well, the company continued its investments in PRO products by expanding the PRO sales force into additional markets across the U.S., as well as increasing job site delivery availability. The good strength in the company’s PRO product demand should also support sales recovery and help in revenue acceleration in the coming years.

In the long run, secular trends from aging housing stock and increased home prices should also accelerate overall demand and boost sales. The average age of housing stock in the U.S. is 40 years old which makes them prone to repair and remodeling services as they require significant renovations and updates. This is creating a good tailwind for the company’s end markets. Further, existing home prices have also increased over the last few years and have resulted in strong home equity. This makes people more financially secure in investing in their existing homes for renovations and upgrades, and should help increase the demand for the company’s products in the coming years.

Hence, I am optimistic about the company’s sales growth prospects ahead. The company should see demand stabilization over the next couple of years and revenue recovery and sales growth acceleration as we exit this year and into the next few years.

Masco’s Margin Analysis and Outlook

Over the last year, the company’s margins benefited from price increases, and cost-saving measures despite volume deleverage.

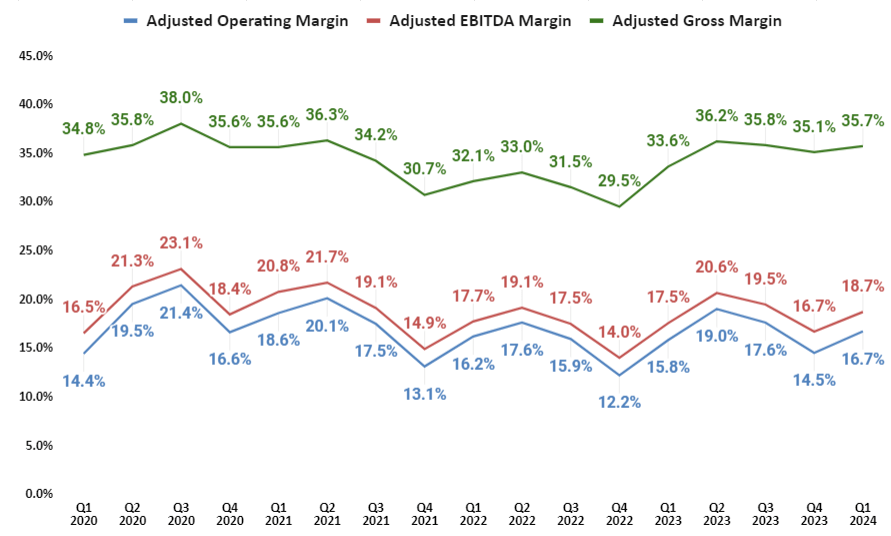

In the first quarter of fiscal 2024 as well, the company continued to offset volume deleverage with the help of price increases, and improvement in operational efficiencies through cost-saving measures. As a result, the adjusted gross margin increased by 210 bps Y/Y to 35.1%. The increase in Adjusted SG&A as a percentage of sales due to higher incentive compensation partially offset gross margin increase, resulting in a 120 bps Y/Y increase in adjusted EBITDA margin to 18.7% and a 90 bps Y/Y increase in adjusted operating margin to 16.7%.

MAS’ Historical Consolidated Adjusted Gross Margin, Adjusted EBITDA Margin, and Adjusted Operating Margin (Company Data, GS Analytics Research)

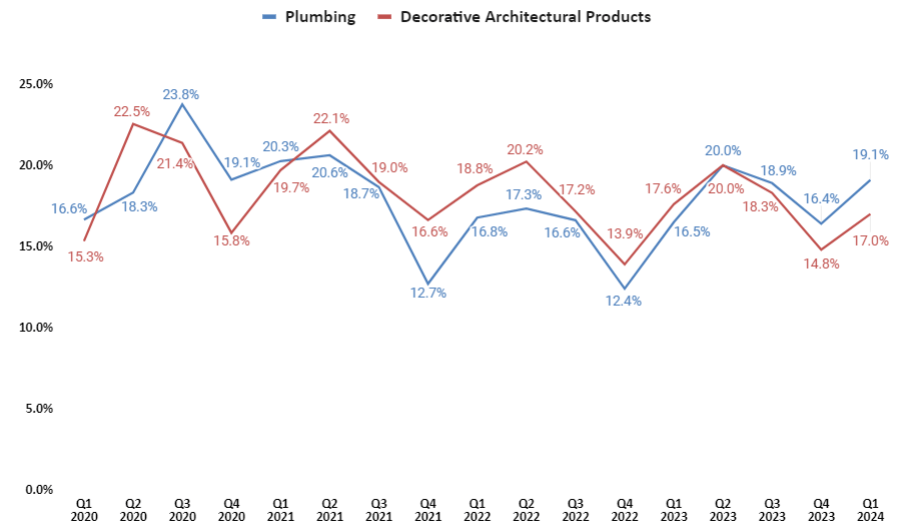

MAS’ Historical Segment-wise Adjusted Operating Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should continue to deliver margin growth. The company took price increases over the last year to offset inflationary input costs. The carryover impact of these previous price increases should continue benefiting the margins for the full year 2024. In addition, management also expects modest input deflation in the current year, which along with the carryover impact of price increases should result in a favorable price/cost environment, helping margin growth. I also expect volume leverage to benefit margins as sales recover exiting 2024 and in FY25.

The company has also been consistent with its cost-saving initiatives. Some examples include improving labor productivity through efficiently managing labor in line with the end market demand, lowering manufacturing costs through bulk purchases of input volumes to get lower purchase prices, commonizing component sets to reduce the number of parts to manage, and increasing the efficiency of new facilities. The company plans to continue these cost-saving initiatives moving forward, which bodes well for the margin growth. Hence, I am optimistic about the company’s margin growth prospects.

Valuation and Conclusion

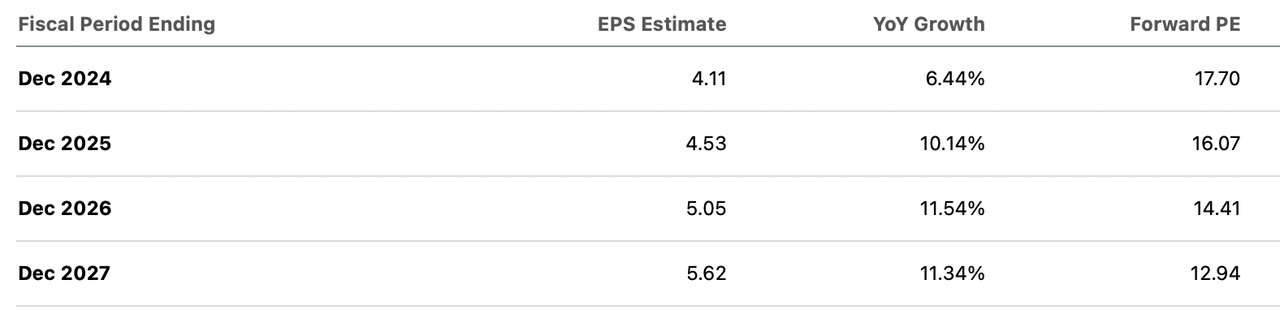

Masco Corporation is currently trading at ~17.70x FY24 consensus EPS estimate of $4.11 and ~16.07x FY25 consensus EPS estimate of $4.53.

MAS consensus EPS estimates (Seeking Alpha)

Over the last five years, the stock has traded on an average P/E forward of 16.56x. So, while Masco’s trading multiple is slightly above the historical average on the FY24 consensus EPS estimate, it is trading at a discount on the FY25 consensus EPS estimate. Compared to its peer Sherwin-Williams (SHW) in the paints industry, which is trading at 28.33x FY24 consensus EPS estimates and 25.35x FY25 consensus EPS estimates, Masco is available at a meaningful discount.

I believe the valuation provides a reasonable entry point given the good growth prospects of the company ahead. The company is well-positioned to deliver revenue recovery in the coming quarters as the end market demand has begun to stabilize after a year of lower demand. Easing comps, market share gains, strength in the PRO paint demand, secular demand trends within the repair and remodeling industry from aging housing stock, and strong home equity should help Masco deliver accelerating revenue growth next year.

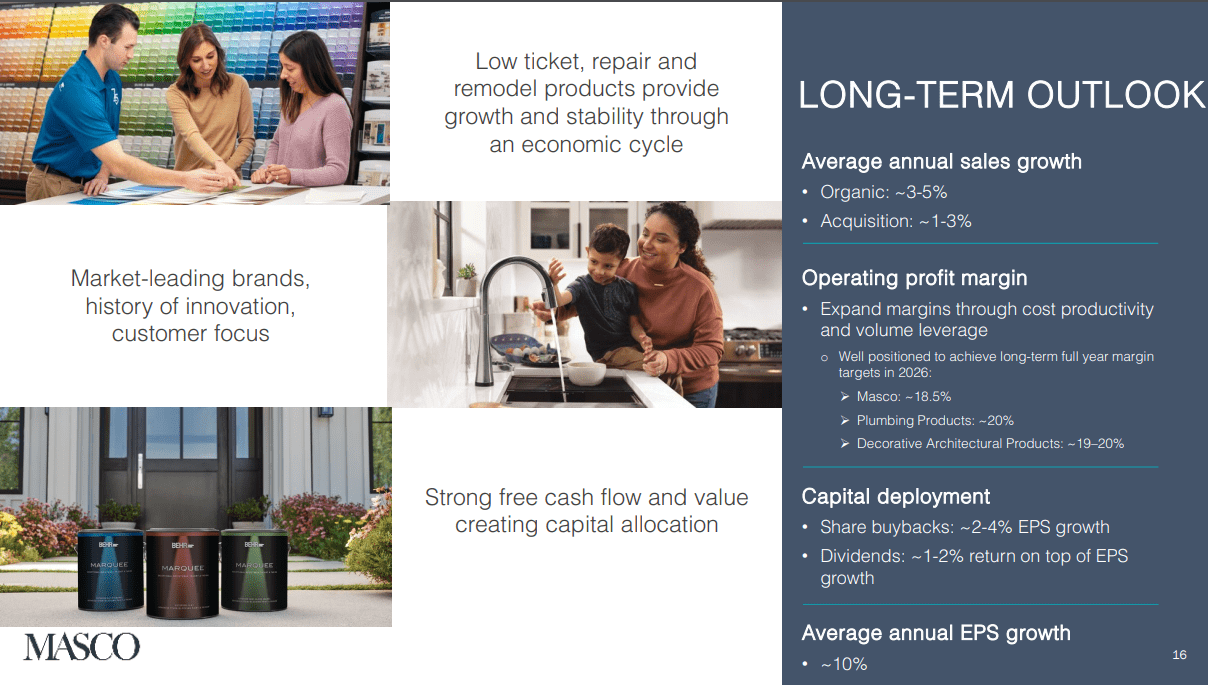

Management has laid out its long-term sales growth of 4%-8% comprising 3%-5% organic sales growth and a 1%-3% contribution from M&As, and average annual EPS growth of above 10%. The company’s result should start tracking in-line long-term algorithm growth from next year onwards and should result in a good upside for the stock. A double-digit EPS growth coupled with a ~1.6% dividend yield could result in an annual stock return to the low teens, assuming the valuation multiple remains constant. Hence, I believe the stock offers a good upside and continue to maintain my buy rating on it.

MAS’ long-term growth algorithm (Q1 2024 Earnings Call Presentation Slide)

Risks

-

The end markets are showing signs of stabilization. However, if the weakness in the end markets persists and there is another leg down as a result of macroeconomic uncertainties like inflationary pressure or a sticky high interest rates environment over the coming year, the revenue recovery could be delayed, impacting overall growth prospects.

-

Any failure to properly implement the cost-saving measures could impact margins.

Read the full article here