Mesoblast: Navigating Regulatory Hurdles with Cellular Innovations

Mesoblast (NASDAQ:MESO) (OTCPK:MEOBF) is an Australia-based biotechnology company committed to “bringing to market innovative cellular medicines to treat serious and life-threatening diseases with significant, unmet medical needs.”

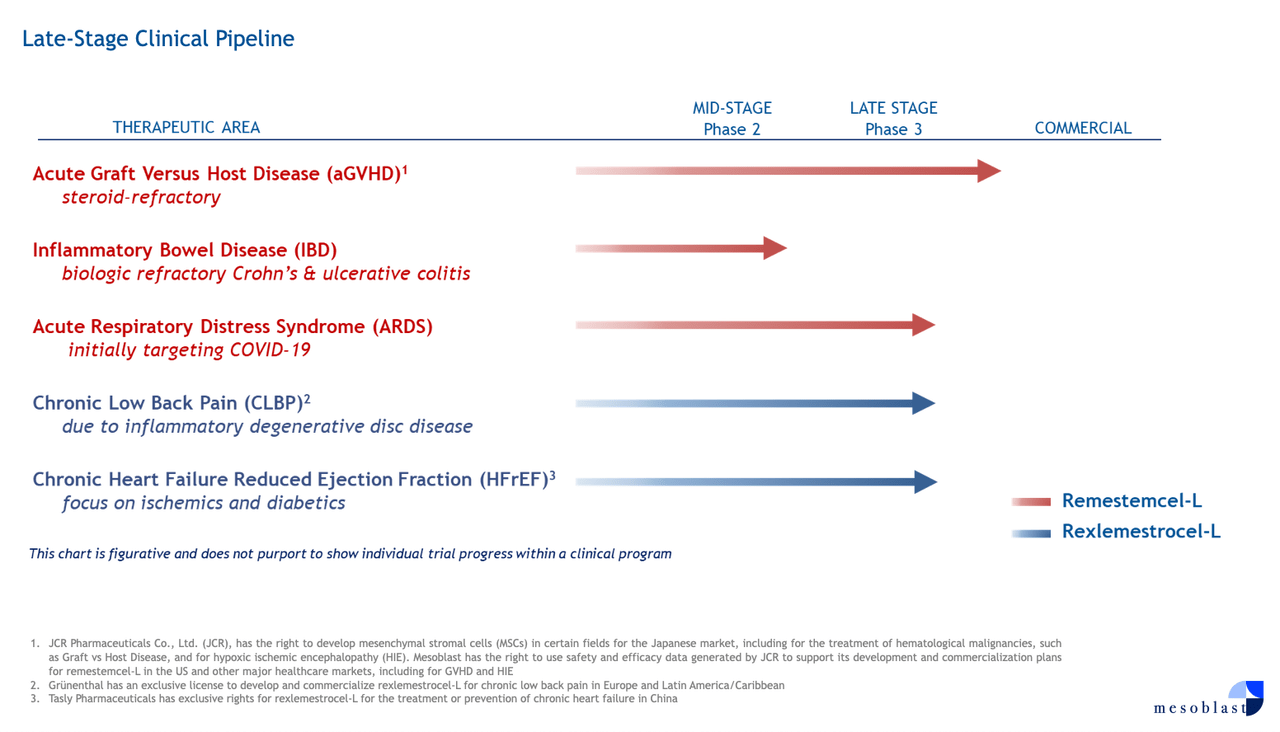

Mesoblast has two allogeneic, off-the-shelf, cellular medicines in development: rexlemestrocel-L and remestemcel-L. The former is being developed for advanced chronic heart failure (Phase 3) and chronic low back pain due to inflammatory degenerative disc disease (Phase 3), while the latter is seeking indications for steroid-refractory acute graft versus host disease (acute GVHD). Mesoblast is also developing remestemcel-L for acute respiratory distress syndrome and IBS.

Mesoblast

Earlier this year, Mesoblast announced that the FDA granted Orphan Drug Designation to rexlemestrocel-L for its potential in treating children with congenital heart disease. The company cites data from a “trial conducted in 19 children” that was “indicative of clinically important growth of the small left ventricle,” prompting further clinical investigation into pediatric congenital heart disease. So, this is quite a speculative venture.

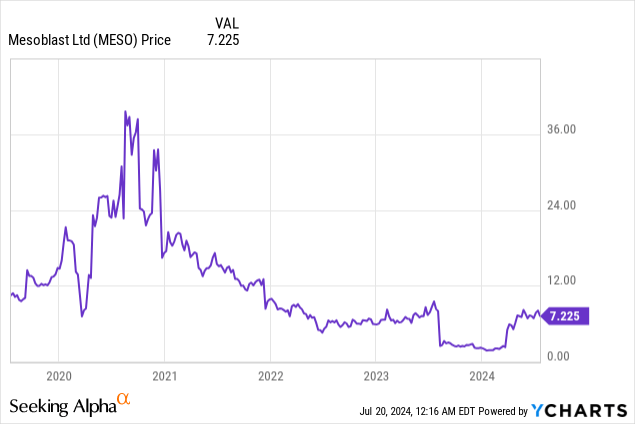

Mesoblast’s stock has seen significant volatility in recent years as a result of remestemcel-L-related developments in pediatric patients with acute GVHD refractory to steroids.

The company has been in communication with the US FDA about a regulatory application for remestemcel-L in this indication. Remestemcel-L was initially denied approval in 2020, with the FDA requesting additional data (a new randomized clinical trial). The company conducted additional research and resubmitted the BLA in January 2023, only to be denied again in August 2023 when the FDA requested data to support long-term efficacy and safety. In March 2024, Mesoblast noted that “the FDA had notified the company that existing data from its MSB-GVHD001 Phase 3 trial looked adequate to support a marketing application for remestemcel-L in children with SR-aGVHD.” Maybe the third time’s a charm? The company resubmitted its BLA earlier this month with the expectation of hearing back within two to six months of receipt.

Mesoblast is also advancing remestemcel-L to a Phase 3 trial in adults with SR-aGVHD following ruxolitinib failure, with trial initiation anticipated within a few months pending FDA feedback on the trial protocol.

The market for SR-aGVHD is very small. According to Frontiers in Oncology, for example, 8,000 patients (pediatrics and adults) underwent allogeneic hematopoietic stem cell transplantation (allo-HSCT) in 2021. It is estimated that aGVHD is a complication that can occur in ~40% of patients following allo-HSCT. In first-line treatment, steroids are utilized, and ~50% will achieve a durable response. Ruxolitinib is utilized in steroid-refractory patients as a second-line treatment, and its efficacy was 57% in REACH1. This leaves ~1,000 US patients on the third-line. While many alternatives exist, there is no consensus regarding which is best.

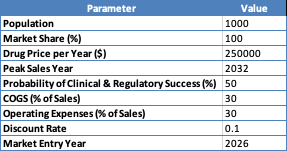

I entered the following parameters and values into my discounted cash flow analysis, which estimates the present value of remestemcel-L in aGVHD:

Author

The calculation that follows assumes linear growth in market penetration until the peak sales year, consistent drug pricing, specified probabilities of success, fixed COGS (higher than typical due to costs associated with manufacturing cell therapies relative to small molecules), operating expense percentages, and a defined discount rate to calculate the present value of future cash flows.

Author

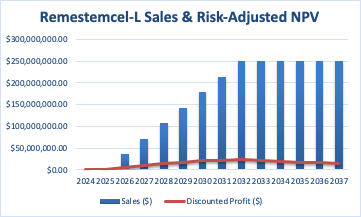

The risk-adjusted net present value [NPV] of $202.9 million is the sum of all discounted profits from the market entry year until 2037.

It is important to note that I combined the pediatric and adult populations, which is especially relevant when I estimated the probability of clinical and regulatory success because this is where the majority of the uncertainty exists. It is worth noting that products that have been rejected twice have only around a 30% chance of approval, and after a third rejection, these odds fall near zero, as this is typically indicative of the inherent and serious shortcomings of a product. It’s also worth pointing out that both of the CRLs were “Class 2,” that is, involving extensive concerns over data. Finally, the odds of success in a Phase 3 clinical trial (adults) in an autoimmune condition are about 60%. So, my estimate of the company’s probability of achieving clinical and regulatory success in both kids and adults is generous.

Moving onto rexlemestrocel-L, after careful consideration, I believe it is not worthwhile to model it. Its Phase 3 heart failure trial did not meet its primary or secondary endpoints. The company found some “positive signals” in a “prespecified assessment” and an “exploratory post hoc evaluation.” Post-hoc evaluations are deeply flawed, so no conclusions can be drawn. Based on their data from prespecified assessments, it appears that there might be some benefit in terms of stroke and myocardial infarction prevention. However, the number of follow-up patients is significantly lower than the initial 500+ patients tested. For instance, after three years, we only have data on 170 patients. This is a relatively tiny sample size to assess for “cardiovascular risk reduction” within a heart failure trial. The company has stated that they intend to seek accelerated approval for rexlemestrocel-L, but I would be extremely surprised if it were approved based on DREAM HF-1, given that the trial failed on multiple prespecified primary and secondary endpoints. While the data presented earlier may warrant further investigation, particularly in patients with high inflammation, rexlemestrocel-L, even if accelerated, is unlikely to be welcomed enthusiastically by the medical community. It is difficult to imagine how it would be used in an environment with several established therapies. Instead, I believe the FDA will request additional data. The DREAM HF-1 trial took six years to complete. As a result, another trial, especially one targeting CV risk reduction, would push rexlemestrocel-L back at least a few years.

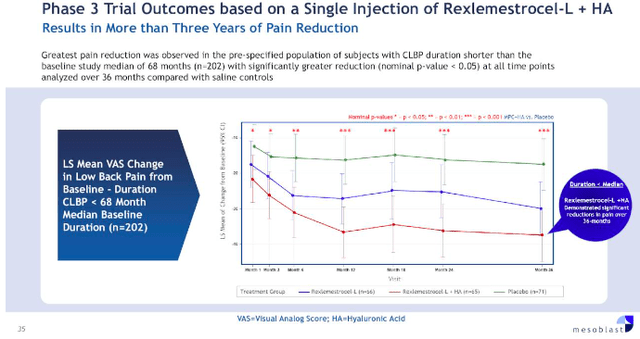

Similarly, rexlemestrocel-L for the treatment of chronic back pain is very challenging to forecast. For example, the first Phase 3 trial compared rexlemestrocel-L with hyaluronic acid [HA], rexlemestrocel-L, and a placebo. Neither treatment arm met the composite outcome of pain reduction and functional responses. Mesoblast notes most of the efficacy occurring in the rexlemestrocel-L+HA arm, but the data may be confounded given that HA is known to help with joints.

Mesoblast

The second and potentially registration-enabling Phase 3 trial, rexlemestrocel-L+HA versus placebo (saline), is recruiting, with an estimated study completion in late 2027. The primary endpoint is pain reduction at 12 months. Rexlemestrocel-L did achieve RMAT designation for this indication.

Financial Health

As of March 31, Mesoblast reported $76.364 million in cash and cash equivalents. They had $107.228 million in long-term borrowings, with $8.534 million owed within twelve months of March 31.

Mesoblast records small revenues from royalty receipts. This figure was $1.661 million in Q1. After accounting for R&D and other costs, net cash used in operating activities was $11.645 million.

To estimate their cash runway, if we divide their current assets by their quarterly cash burn, this suggests ~1.5 years of cash runway. This estimate excludes $10 million in additional debt financing they may be able to draw upon.

Risk/Reward Analysis and Investment Recommendation

Returns for Mesoblast’s investors have been very poor over the last ten years. The company’s prospects are difficult to gauge. After a third regulatory submission, they may find success in pediatric SR-aGVHD, but, as evidenced by my DCF analysis, this is a small and limited market. Chronic back pain and heart failure data, to date, while setting a foundation for further research, are inconclusive and require more research. Approval in these markets may be years away, and both indications are full of treatment options. It’s difficult to envision how Mesoblast’s solutions would be utilized in these markets.

There is significant operational risk encompassing clinical, regulatory, and market (including patient/provider adoption and manufacturing) realms. As the company points out (page 9),

Our product candidates are based on our novel mesenchymal lineage cell technology, which makes it difficult to accurately and reliably predict the time and cost of product development and subsequently obtaining regulatory approval. At the moment, no industrially manufactured, non-hematopoietic, allogeneic cell products have been approved in the United States.

Mesoblast’s balance sheet is sound in the short term, but pressure is building in the long run. It is difficult to see the company becoming profitable soon. As a result, they will need to take on additional debt and/or raise equity. They would ideally form partnerships. Recall that Mesoblast had an agreement with Teva (TEVA) in heart failure before Teva pulled out in 2016. They secured one in chronic back pain, but it was very “backloaded” (e.g., payment at signing was only $15 million). Furthermore, their partner, Grünenthal, “downgraded” their deal in 2021. I do believe that their technology makes the most sense for this indication, but achieving successful and convincing clinical data, regulatory approval, and market adoption are major uncertainties. In my opinion, Mesoblast is essentially a bet on rexlemestrocel-L for chronic back pain, which is a difficult task.

Author

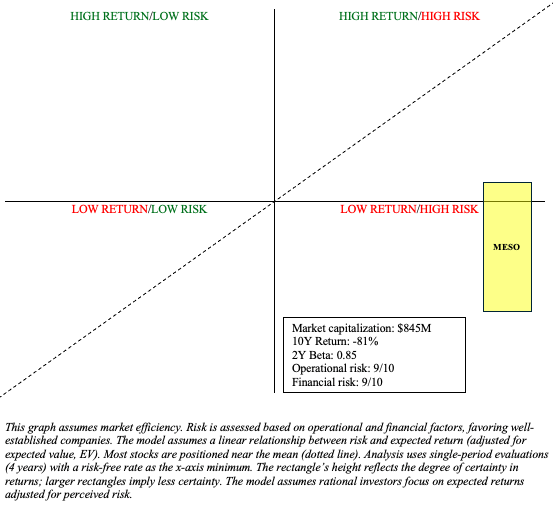

MESO has the potential to be a Quadrant 1 stock (high risk/high return), but I believe the risks outweigh the return potential at this time, especially given its market capitalization of nearly $1 billion. As such, MESO is a “Sell.”

There are risks to my sell recommendation. As noted in the chart above, MESO’s returns may beat the market’s despite its high risks. So, there are opportunity costs involved. Although I express skepticism regarding their prospects in chronic back pain and heart failure, even if they achieve niches in these markets, their stockholders would likely be rewarded. Moreover, I may have underestimated the aGVHD market. Finally, the company is undergoing efforts to reduce their OpEx. This should extend their cash runway beyond my estimate and reduce their dependency on debt financing, lowering their overall financial risk.

Read the full article here