ETF Overview

SPDR S&P Oil & Gas Exploration & Production ETF (NYSEARCA:XOP) owns a portfolio of oil and gas exploration and production stocks. XOP’s portfolio consists of mostly small-cap and mid-cap stocks. The fund should benefit from a new rate cut cycle if the Federal Reserve begins to lower their key interest rates. In this new macroeconomic environment, energy demand will be supported due to improving business and consumer activities. In addition, XOP’s portfolio of mostly small-cap and mid-cap stocks should have less stress in servicing their debts. Hence, we expect XOP to outperform the broader market in the upcoming year. As such, XOP deserves a buy rating.

Fund Analysis

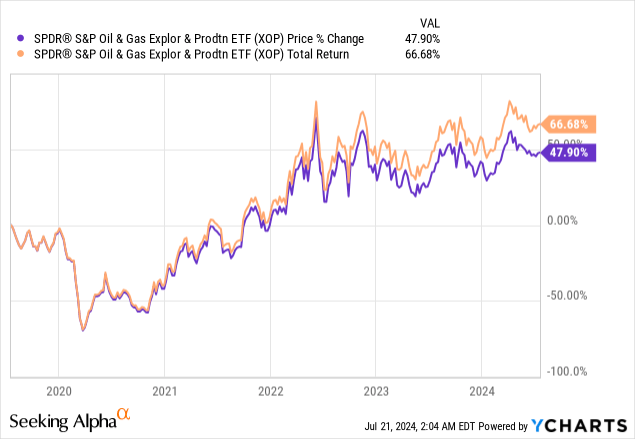

XOP’s fund price has been on a rising trend since the low in 2020

Let us first review how XOP performed in the past few years. Unlike the broader market that experienced a bear market in 2022, XOP has not experienced a meaningful decline in 2022. In fact, its fund price has steadily moved higher with higher lows and higher highs. However, XOP’s total return since 2023 has lagged the broader market. The S&P 500 index has outperformed XOP with a total return of 46.9% since the beginning of 2023. In contrast, XOP only delivered a total return of 12.0%.

YCharts

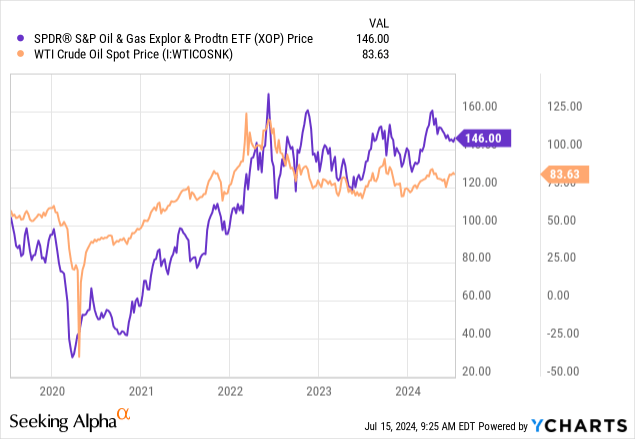

Strong correlation to oil price

Oil and gas exploration and production stocks belong to upstream energy stocks. Therefore, XOP include mostly stocks of upstream energy companies. These upstream stocks typically have higher sensitivity to energy prices. This is exactly the case to XOP. As can be seen from the chart below, XOP’s fund price has a high correction to WTI crude spot price.

YCharts

A new rate decline cycle is favorable

We are now in a very different macroeconomic environment than two years ago. Inflation has fallen considerably from the peak of 9.1% reached in mid-2022 to 3% in this past June. While it may still take a while for inflation to reach the Federal Reserve’s 2% long-term target, the Federal Reserve has indicated that a rate cut can still happen before inflation reaches this target. Hence, we are confident that the Federal Reserve is preparing to begin for a new rate cut cycle very soon. In this new rate cut cycle, the cost to service the debt for consumers and businesses will fall. This should eventually result in higher business and consumer activities. In this environment, demands for energy will also increase. Hence, a new rate cut cycle should support and cause oil prices to strengthen. Since XOP’s fund price has a strong correlation with oil price, we think XOP will eventually benefit from this new rate decline cycle.

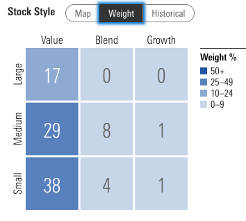

XOP’s portfolio of mostly small-cap and mid-cap stocks should also benefit

XOP’s portfolio consists of mostly small-cap and mid-cap stocks. As can be seen from the stock style table below, small-cap and mid-cap stocks represent about 83% of XOP’s total portfolio. In contrast, large-cap stocks only represent about 17% of the total portfolio.

Morningstar

As we have stated earlier, a rate decline cycle should be beneficial to consumers and businesses as the costs of servicing their debts will decrease. This is even more so for small-cap and mid-cap stocks than large-cap stocks. This is because small-cap and mid-cap stocks typically have weaker balance sheets than large-cap stocks. Therefore, these stocks tend to be impacted much more negatively in a rate rising environment. As soon as we enter a new rate decline cycle, these stocks should react positively as interest costs will be reduced, and their stock valuations may experience multiples expansion as well.

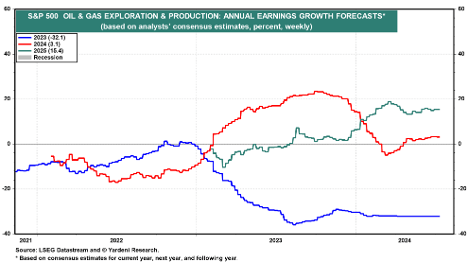

Annual growth forecast is strong in 2025

We do not have any consensus annual earnings growth forecast for stocks in XOP’s portfolio. However, we do know that oil & gas exploration & production stocks in the S&P 500 index (consists of large-cap stocks) are expected to see significant growth to their earnings in 2025 (see below). As can be seen from the chart below, these large-cap oil & gas exploration & production stocks are expected to see their earnings grow by 15.4% in 2025. Although we do not have the figure for small-cap and mid-cap stocks, we do know that small-cap and mid-cap stocks should have better earnings growth potential in a lower rate environment than large-cap stocks. Therefore, it is very likely that XOP’s portfolio of mostly small-cap and mid-cap stocks should have even better earnings growth rate than the growth rate of 15.4% of these large-cap stocks in the S&P 500 index.

Yardeni Research

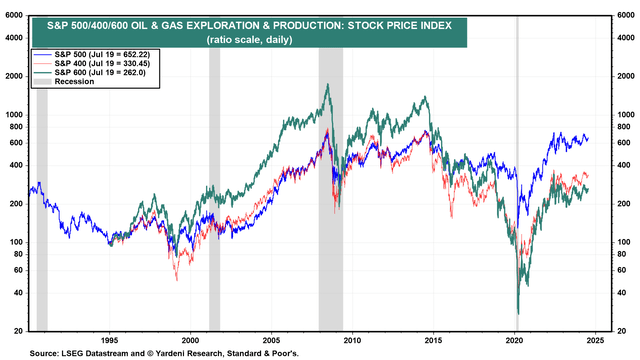

There is still room for XOP to gain ground

Below is a chart that compares the stock price index of oil & gas exploration & production stocks in the S&P 500 (large-cap), S&P 400 (mid-cap), and S&P 600 (small-cap) indices. As can be seen from the chart below, large-cap oil & gas exploration & production stocks have almost recovered from the previous high reached in 2008 and 2014. In contrast, small-cap and mid-cap stocks in this sector have not yet recovered from their previous highs. Given the likelihood of outperformance of small-cap and mid-cap energy stocks to large-cap energy stocks in the upcoming rate cut cycle, we think there is likely more room for XOP to move higher.

Yardeni Research

Investor Takeaway

We have a buy rating for XOP as the fund should benefit greatly in a new rate decline cycle. Hence, investors may want to take advantage of any pullbacks.

Additional Disclosure: This is not financial advice and that all financial investments carry risks. Investors are expected to seek financial advice from professionals before making any investment.

Read the full article here