I gave Cadence Design Systems (NASDAQ:CDNS) a ‘Hold’ rating in my initiation article published in July 2023. I highlighted their leadership position in the semiconductor electronic design automation (EDA) software industry but expressed my concerns about the stock price valuation. They released their Q2 FY24 earnings on July 22nd after the market close, beating the market consensus and gaining momentum with its AI portfolio. As its stock price is overvalued, as per my calculations, I reiterate a ‘Hold’ rating with a one-year price target of $250 per share.

Accelerated Verification and Performance Required by AI

My biggest takeaway from the quarter is Cadence’s evolving portfolio in the AI semiconductor industry. In recent months, Cadence has been expanding its partnership with global foundry players and unveiled its new prototyping systems to support AI chip designing activities.

- In June 2024, Cadence announced the achievement of several key milestones partnering with Intel (INTC) foundry including the complete AI-driven Cadence flow, digital full-flow for Intel 18A as well as Design IP for Intel 18A.

- In June 2024, Cadence announced its collaboration with Samsung (OTCPK:SSNLF) Foundry to accelerate design for AI and 3D-IC semiconductors. Cadence is working with the implementation flow for Samsung Foundry SF2.

- In April 2024, Cadence launched its new Palladium Z3 and Protium X3 Systems for accelerated verification and better performance for AI workflows.

In my view, Cadence is well positioned to capture the growing demand in the EDA market. As AI chip designs require increased capacity and higher verification throughput, Cadence’s AI portfolio can help the company capture more market share in the EDA and verification market. As indicated in my previous article, Cadence and Synopsys dominate the EDA software market, with leading technology to support the entire semiconductor industry’s designing activities. In the AI era, it is evident that both Cadence and Synopsys can share the benefits of rapid AI market growth.

Q2 Review and FY24 Outlook

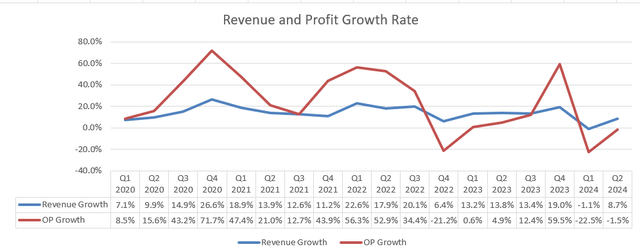

As depicted in the chart below, Cadence delivered 8.7% growth in revenue with a $6 billion of backlog, beating the market expectations for both topline and bottom lines.

Cadence Quarterly Earnings

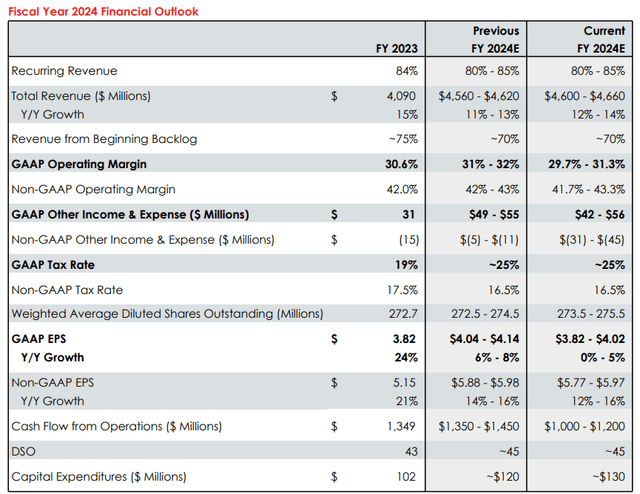

Now, the company guides 12%-14% growth in revenue and 12%-16% growth in adj. EPS for FY24, as detailed in the table below:

Cadence Q2 FY24 Earnings

For the FY24’s growth, I am assessing the following factors:

- Cadence announced to acquire BETA CAE Systems for $1.24 billion on March 5th 2024. The acquisition is quite value accretive to Cadence in my view. BETA CAE’s solutions can potentially extend Cadence’s simulation portfolio to several end markets including automotive, aerospace, industrial and healthcare. BETA CAE has an annual revenue of about $90 million, and Cadence expects the acquisition will add $40 million in revenue for FY24.

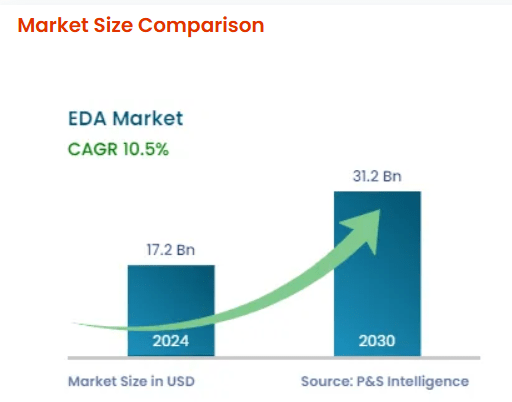

- President & Strategic Intelligence predicts the EDA market will grow at a CAGR of 10.5% from 2024 to 2030. As a market leader in the EDA market, Cadence has the potential to outgrow the overall market by gaining more shares from small players.

President & Strategic Intelligence

- The growth area in the semiconductor industry is predicted to be in the AI, automotive and industrial automation markets, according to most chip design companies. As discussed in my previous article, Cadence is well positioned in these growth areas.

Overall, I estimate that Cadence will achieve 13% organic revenue growth for FY24, with the acquisition contributing 1% to the topline growth.

Valuation Update

For the growth rate from FY25 onwards, I anticipate the company will continue its growth momentum, achieving 13% organic growth. As the acquisition is part of its growth strategy, I forecast the company will allocate 10% of revenue towards M&A, contributing 2%-3% to the overall topline growth.

As a semiconductor software company, Cadence has already generated a respectful operating margin, standing at 30.7% in FY23. I anticipate 20bps margin expansion in the DCF model assuming 10bps from new product launching with higher ASP, and 10bps operating leverage from sales & marketing expenses.

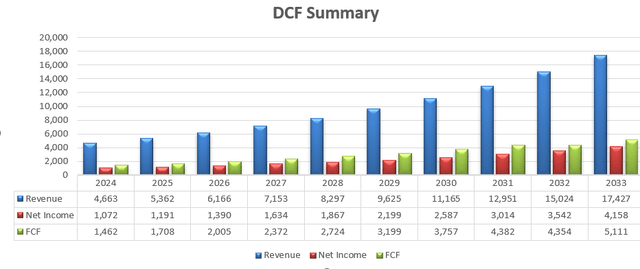

The summary can be found as follows:

Cadence DCF – Author’s Calculations

I calculate the free cash flow from equity as follows:

Cadence DCF – Author’s Calculations

The cost of equity is calculated to be 14% assuming: risk-free rate 4.2% ((US 10Y Treasury Yield)); beta 1.4 (SA); equity risk premium 7%.

The one-year price target is calculated to be $250 per share after discounting all the future free cash flow. The stock price is trading at more than 50x free cash flow, and the stock price is high, expensive in my view.

Key Risks

China represents more than 16% of total revenue, growing by 30% year-over-year in FY23. Currently, the U.S. government primarily focuses on the export restrictions for advanced AI chips and manufacturing equipment, and has not paid much attention to the EDA software market. However, it is quite possible that EDA software could become a tool used by the U.S. government to hinder the advancement of the Chinese semiconductor industry, as EDA is mission-critical for the chip design process. In other words, EDA could become another battlefield amid the geopolitical tensions between the U.S. and China.

End Notes

I believe Cadence is well positioned in the rising semiconductor market, with its EDA software being mission-critical for the chip design process, especially for more complex AI chips. However, the stock price is overvalued; therefore, I reiterate a ‘Hold’ rating with a one-year price target of $250 per share.

Read the full article here