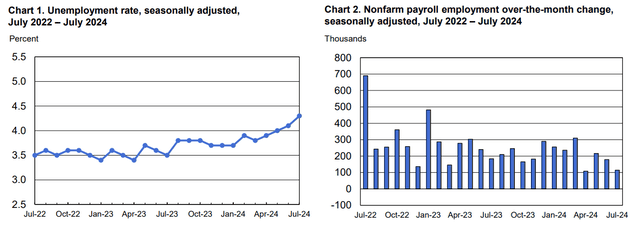

The July payrolls report revealed a soft 114,000 jobs gain. That was below the consensus which called for +175,000 positions and the lightest since December 2020. Revisions to the previous two months were negative by 27,000 jobs – the third consecutive month of downward revisions. The unemployment rate rose significantly to 4.25%, the highest since October 2021, triggering the Sahm Rule which asserts that a US recession is imminent.

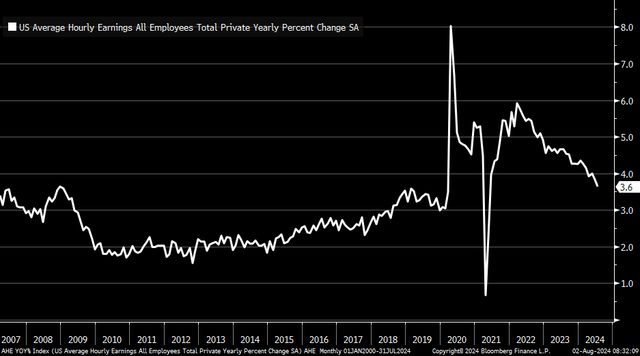

Average hourly earnings for July were soft, just 0.2%, while the year-on-year rate came in light at 3.6%, below the 3.7% forecast, and significantly below the June read of 3.9%. The average workweek dipped to 34.2, the lowest since March 2020. The labor force participation rate actually ticked up, a good sign, to 62.7% – the best since November 2023 as the prime-age labor force participation rate rose in July to its highest since March 2001.

Digging into the report, the U-6 underemployment rate rose to 7.8%, up from June 7.4%, the highest since October 2021. Government jobs added only 17,000 and private payrolls summed to 97,000, below the 148,000 expectation. The July household survey revealed a comparably light jobs gain of 67,000 compared to 116,000 in June.

The employment picture suggests that neither much firing nor hiring is going on in the US economy right now. That could portend weak trends among other backward-looking indicators and a significant slowdown from the pace of economic expansion in the first half.

A Weak July NFP Report, Sahm Rule Triggered

Christian Fromhertz

Unemployment Rate Jumps, Fewer Jobs Created in July

BLS

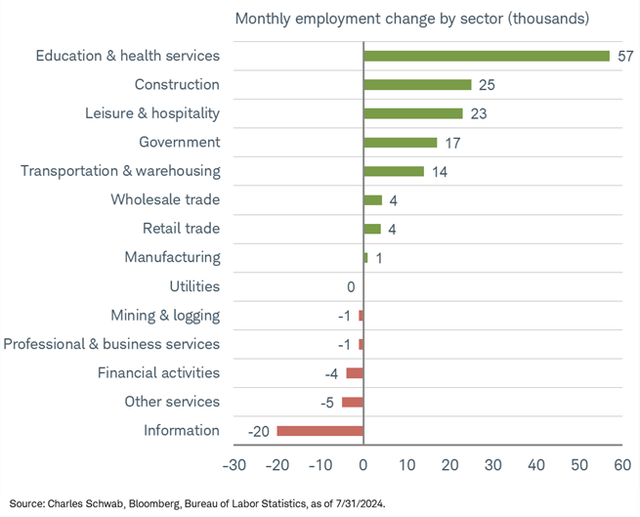

Job Losses in Tech & Financials

Kevin Gordon, Schwab

US Average Hourly Earnings Growth Falls to Just 3.6% YoY

Kevin Gordon, Schwab

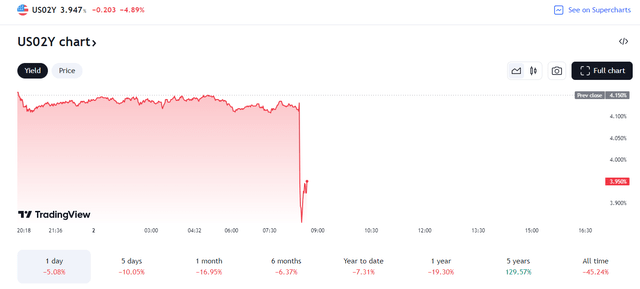

It was a broadly weaker-than-expected July labor market report, and stock market futures fell further initially after the 8:30 a.m. ET report. Bond yields sunk, too. The yield on the 2-year Treasury note dropped to fresh year-to-date lows, down about 30 basis points, to near 3.84% at the low, while the 10-year rate fell below 3.8% in the moments after the data release. The S&P VIX Index (VIX) jumped to a 2024 high, too, above 21.

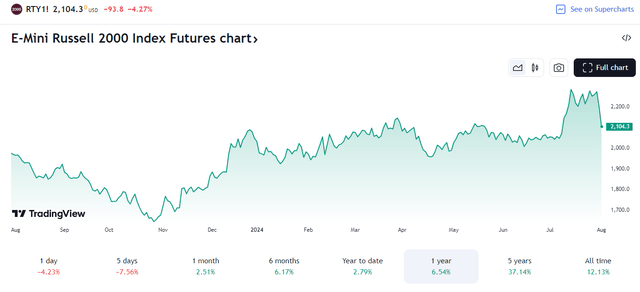

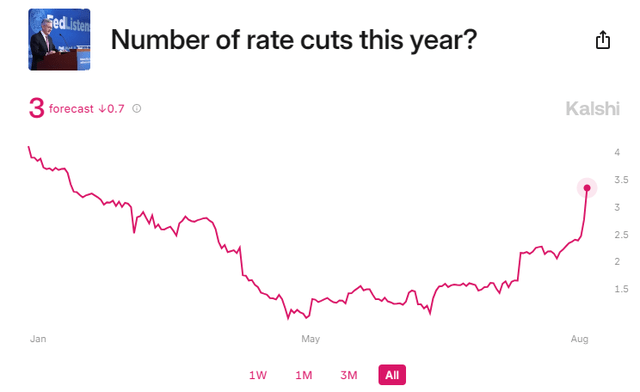

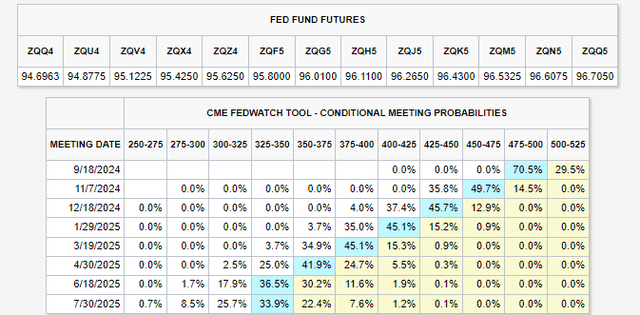

Bond traders now price in between four and five quarter-point rate cuts by the Fed between now and year-end. There’s now a 90% chance of a large 50-basis-point ease by September. Russell 2000 futures were -4% in advance of the Wall Street open.

Spot gold (XAUUSD:CUR) surged to a record high of $2470 per ounce amid a clear risk-off trading atmosphere. The US Dollar Index (DXY) was also lower, which bucks the usual flight-to-safety trade we commonly see during significant market drops.

It’s key to remember that futures and global markets were already significantly lower before the July NFP report – the Nikkei 225 plunged 5.8% in overnight trading, its worst session since Black Monday of 1987.

US 2-Year Yield Plunges to 3.84% at the Morning’s Low

TradingView

2s10s Least Inverted Since July 2022

TradingView

VIX Surges to a 2024 High

TradingView

Russell 2000 Futures Give Up Most of July’s Gain

TradingView

A Rising Number of 2024 Rate Cuts Expected

Kalshi

113 Basis Points of Cuts Priced Into 2024

CME FedWatch Tool

Markets are clearly in a “shoot first, ask questions later” mood, but it’s key to realize that lower interest rates today should help many companies that depend on debt financing. Considering that corporate earnings are coming in well and business and personal balance sheets are generally decent, there are still some positive aspects of today’s economy.

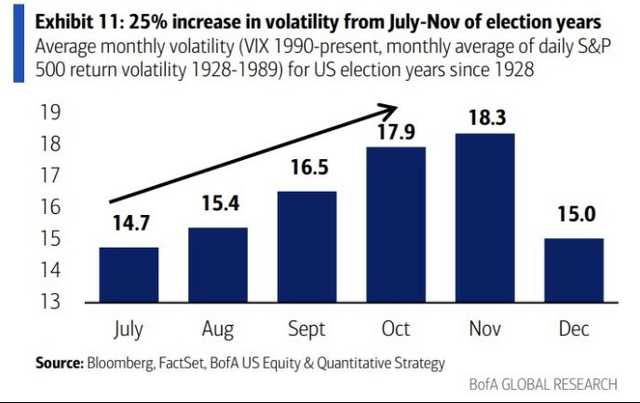

Big picture, perhaps some areas of the market are due for a correction, and we often see volatility tick up as the election date nears. All eyes will be on July eco data to come for further indicators of just how much of a slowdown we’ll see.

Volatility Often Increases Heading Into Elections

BofA Global Research

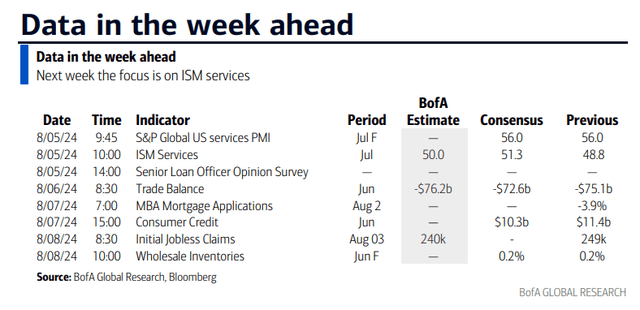

Looking ahead, it’ll be a respite for macro traders next week. The data deck is light, but it will still be a busy period for Q2 corporate earnings reports. The bottom-line beat rate has been decent this season, just shy of 80%, and reactions to quarterly reports have mostly been solid compared to previous quarters.

We’ll get the July final read on S&P Global US Services PMI on Monday, the key July ISM Services PMI comes shortly after along with the SLOOS report in the afternoon. Tuesday is light with just June Trade Balance data before Wednesday’s Mortgage Applications data and a look at June Consumer Credit figures. Weekly jobless claims will be key to watch to see if this past week’s jump was the start of another leg higher. The week wraps up early on the data front with Wholesale Inventories for June at 10 a.m. ET Thursday.

Next Week’s Data Deck

BofA Global Research

The Bottom Line

The labor market continued to slow in July. While there was a headline payroll gain, both the establishment and household surveys showed weak employment growth. The unemployment rate’s jump to 4.25% triggers the Sahm Rule, which asserts that a domestic recession may be on the way. Stock market futures took a leg lower, while Treasuries caught a big bid. All eyes are now on when the Fed will cut rates and by how much.

Read the full article here