Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the fourth week of July.

Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the closed-end fund (“CEF”) markets for perspectives across the broader income space.

Market Action

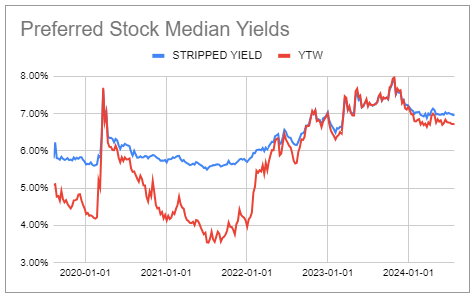

Preferreds were flat on the week and up month-to-date so far due to the drop in Treasury yields and steady credit spreads.

Yields are on the lower part of their range so far this year. Apart from the brief gap lower in early 2023, yields are at their lowest level in about 18 months.

Systematic Income Preferreds Tool

Market Themes

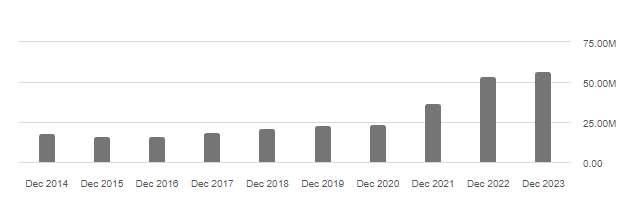

Agency mortgage REITs are reporting Q2 results. Dynex Capital (DX) saw a 5% drop in book value and a modest decrease in leverage. Despite the book value drop, equity / preferreds coverage rose to 8.4x from 7.6x as a result of a large common equity issuance. DX equity issuance has been on fire in the last few years, as shown below.

SA

This has been a hallmark of Agency mREITs – a steady drop in book value has been offset by additional equity issuance. For example, from Dec-2020 DX book value is down by a third while coverage of the same preferred is up by nearly 50%.

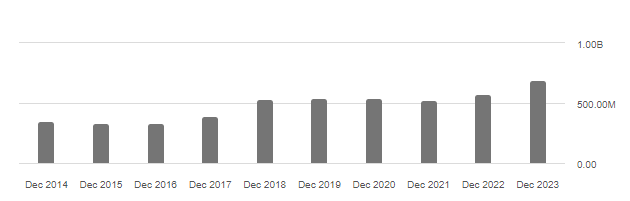

A similar dynamic for AGNC – a 5% drop in book value in Q2 was offset by a 5% rise in the number of shares, driving a steady level of equity / preferreds coverage of 5.1x. Agency mREIT preferreds particularly from NLY, DX and AGNC have been tremendous assets over the last couple of years and remain core holdings in our Income Portfolios.

SA

Although the yields of the preferreds are well below the common shares, the performance of the preferreds puts the common to shame. Across the three companies, DX, NLY and AGNC, the preferreds have outperformed the common by miles over the last decade. The common in these companies have delivered around 4-4.5% per annum over the last decade, versus 7-8% for the preferreds.

Investors need to remember that in the preferreds, the yield is much closer to the longer-term return they are likely to get. As far as the common, investors should mentally subtract 5-10% from the yield to get a sense of the likely longer-term return. This is due to the fact that the common investors are short interest rate volatility and the stocks lose value through periodic deleveraging due to the negative convexity of their Agency MBS portfolios.

Market Commentary

Synovus Financial Corp. preferred Series E (SNV.PR.E) has had its coupon reset on its first call date earlier in the month. The new coupon was set in line with the 5Y Treasury yield + 4.127%, resulting in a coupon of 8.507% and a slightly lower yield as it’s trading around 1% above “par” in stripped price terms.

The stock enjoyed a steady price rise towards “par” over the last few months which was expected and part of the win-win playbook of below-par Fix/Float preferreds on the service which would either be redeemed, generating a high yield-to-call or would float at a very attractive coupon. SNV.PR.E will not be redeemable for another 5 years until the next reset date, so the coupon is locked in until then. The yield of around 8.4% is very attractive, particularly as 5Y Treasury yields have fallen a bit since the stock reset its coupon. The rest of the Bank preferreds sector trades at a much lower yield of around 6.3%. SNV.PR.E remains in a couple of Income Portfolios.

A few bank preferreds were added to the Preferreds Tool. Citizens Financial issued a new CFG.PR.H 7.375% fixed and redeemed CFG.PR.D. It’s split-rated by S&P and Moody’s but overall the ratings are on the high side in the sector.

Two M&T Bank preferreds were also added. M&T Bank Corporation Series J (MTB.PR.J) recently started trading. It was issued near a local peak in longer-term rates and so rallied as rates have fallen back. The yield of around 6.8% is still decent.

BDC Trinity Capital is issuing a new 7.875% $100m 2029 bond (TRINI). Use of proceeds is to partly redeem the 2025 bonds and pay down some of the KeyBank facility. There is $180m of the 2025 bond so there is not enough of TRINI to fully redeem it. It probably makes sense to wait a bit more and see if TRIN issues a larger bond to fully redeem the 2025 bond, which may then have a higher coupon.

As it is, the yield of the new bond is slightly below the other 2029 bond TRINZ so we could see some weakness at the open. Overall, it’s good to see the potential reduction in the credit facility. The less secured debt there is ahead of the bonds, the stronger they are, as they have a larger claim on the rest of the portfolio. Historically, the TRIN bonds traded at a lower yield than they should have, and this has corrected somewhat as the rest of the market has rallied versus them. At this point, they are beginning to look fairly attractive – the yield is right on top of the sector average.

Angel Oak Mortgage REIT is issuing a new 9.5% 2029 bond (AOMN). The portfolio is focused on non-QM residential loans and RMBS. Recourse leverage is fairly low at 1.3x. Book value has been steady over the last couple of years after the initial fall in early 2022. It’s worth a look if it opens around par or below.

Read the full article here