Introduction

Magna International Inc. (NYSE:MGA) recently reported Q2 earnings, which were met negatively due to poor y/y results and revised guidance lower for ’24 and ’26. The stock price suffered, and since my first article on the company, where I recommended holding off for now because of tight margins, declining efficiency, and poor revenue growth, the company saw a -30% decline, compared to the S&P 500’s (SPY) 5.5% increase. I wanted to go through the numbers and slightly comment on the outlook and what is still keeping me away from starting a position.

Q2 Results

Let’s start from the top. The company’s sales came in at $10.96B, which was more or less flat y/y (-0.2%) and missed the consensus by $50m. Non-GAAP EPS came in at $1.35, which missed consensus estimates by $0.10. Adjusted EBIT came in at $577m, lower than the $616m it did the year before. In GAAP terms, the company’s EPS came in at $1.09, compared to $1.18 the year before.

On the margins side of things (GAAP terms) the company’s gross margins saw a slight improvement y/y (13.36% vs. 13.09%), while EBIT and net margins were down 50bps and 23bps y/y, respectively. On adjusted terms, as the company likes to highlight these the most, the Adjusted EBIT margin, came in at 5.3% vs. 5.6% the year before, and 4.8% vs. 4.9% for the 6 months ended June 30 vs. a year before.

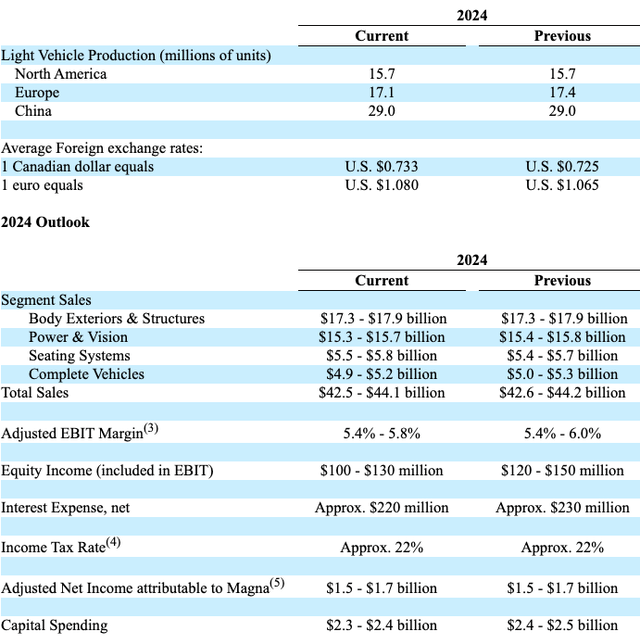

This lackluster performance can be attributed to the overall slump in global automotive activity, especially in the European markets. NA saw light vehicle production up 1%, China up 6%, while Europe saw a 5% decline, which led to this underperformance. Furthermore, Detroit-based customers declined 5%. So, the lack of y/y progress certainly didn’t help its case, but what put it completely down was the management’s updated outlook to the downside.

The company updated its 2024 assumptions as per below. The only change in the production part was the weakness in the European segment, while the company also adjusted FX numbers. These numbers led to the 2024 outlook being adjusted downward. The Power & Vision and Complete Vehicles saw a slight decrease in sales, which led to a decrease in the total sales outlook. Furthermore, the company has introduced some changes to its adjusted EBIT margins, and capital spending as well.

MGA 6-K report

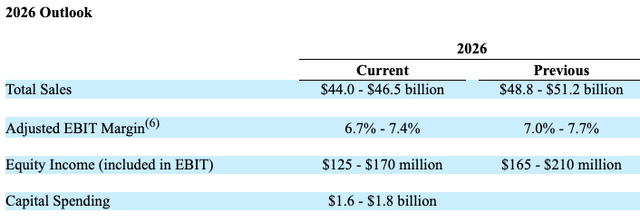

To be honest, revisions down are quite minimal. However, there are adjustments to the downside in any case, which is never a good thing. To add more to the negative side, the company also adjusted its 2026 outlook, which was much more pronounced, with the most significant change seen in the sales figures.

MGA 6-K report

So overall, the report was not great in my opinion. It appears that Europe is having some trouble with the demand for vehicles, as evidenced by the lower sales above. Moreover, the company’s efficiency seems to have come down also. In my first article on the company, I mentioned that the management could improve operational efficiency by 150bps. So, it appears that it is not the case here, as the slump in demand in Europe may have pushed it further out for now. Since reporting these numbers and adjustments to the outlook, the company saw around a 9% decline in share price. Of course, the market-wide selloff in the last couple of days didn’t help it at all, too.

Comments on the Outlook

The company is reliant on the overall global demand for vehicles. The outlook is not looking as rosy as a couple of years ago due to the much softer demand for EVs. The adoption rate of BEVs has been much slower than anticipated, which is going to affect the company’s sales, and the downward adjustments are a good indication that it is a material issue. I do not doubt that EVs will be the future, but in the current state, many people are not looking to upgrade due to high maintenance expenses and upkeep. ICEs are much more economical in that sense; however, I also think that bridging the gap between ICEs to EVs, hybrid is the way to go right now. Many people think the same way, as Hybrid vehicles are outpacing the sales of EVs. So, this should soften the blow overall, but I don’t think this is going to help its top-line growth significantly.

Recently, Tesla, Inc. (TSLA) reported numbers that it delivered almost 444k vehicles in Q2, which was above consensus estimates. However, margins took a hit as well since the discounting of the vehicles meant there wasn’t enough demand at those previous prices. At least MGA doesn’t rely on a single car manufacturer for its revenues, however, the overall weakness worldwide, means that there will be further pressures to the downside in terms of operations, and efficiency.

In terms of margins, I would like to see signs of at least bottoming over the next while, two to three quarters. I would like to see what the company can do to achieve higher efficiency, and whether it can in the first place. It is very dependent on the overall market demand for vehicles and there isn’t much it can do to control it, if anything. The company is said to be “taking steps to address the new market dynamics” and is committed to “margin expansion, capital discipline, and free cash flow generation” by “restructuring {their} complete vehicle cost base to adjust to lower volumes in the near term.” All of this is supposed to be evident going forward, especially by 2026. These are good promises in theory, but I will be convinced once I see some progress.

Closing Comments

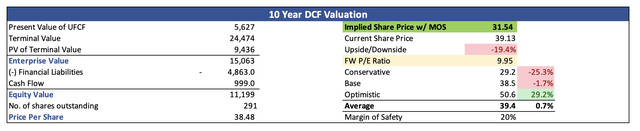

So, in my opinion, there is no rush to start a position right now. The Magna International Inc. numbers are not very promising for the next while, with no material improvement in margins, and a decrease in top-line growth isn’t helping any bullish case. In my previous article, which I have linked before, still stands, which means there is still a decent room for further pressure on the share price. If anything, the negative adjustments to 2026 in terms of sales and margins, bring it further down, but only slightly. Back in January, my fair price for the company stood at around $32 a share. With an update on sales for FY26 to be around $45.6B, and keeping the margins somewhat similar to before, MGA’s change in fair value is minimal. It is currently at $31.54 a share, meaning the company is still trading at a decent premium, but not as bad as before.

Author

Therefore, I am going to continue to stay on the sidelines. While my price alert has not been triggered yet, I wouldn’t be surprised if it will be within the next half a year. There are plenty of issues that are out of the hands of the company. The biggest one is, of course, the demand for vehicles, and the overall selloff in the broader markets, which may bring its share price down to where I would consider putting in some capital. I think it will be an interesting remainder of the year in terms of the economic outlook, so I will be ready to take advantage if we get further down.

Read the full article here