I am updating my previous analysis on GE HealthCare Technologies Inc. (NASDAQ:GEHC) in light of Q2 2024 earnings which were released on July 31st, 2024.

I previously rated GE HealthCare a hold for the following reasons:

- GE HealthCare was lagging market growth across its businesses.

- The AI business had potential, but I didn’t believe management was correctly counting the impact of competition in their expectations.

- DCF generated price target of $74 was essentially flat to the price at the time.

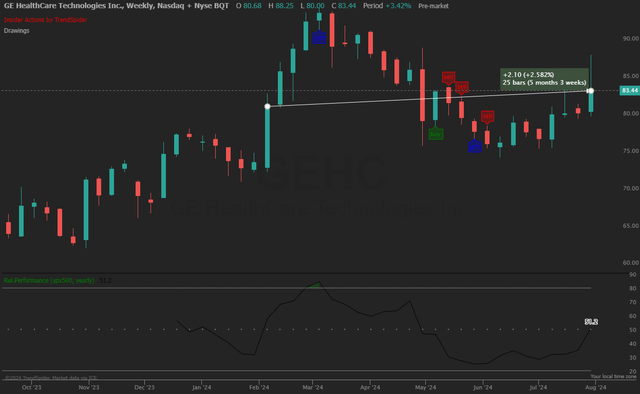

Since then, GE HealthCare has returned 2% while they S&P 500 has returned 8%.

GEHC Trend vs S&P 500 (TrendSpider)

I was disappointed by GE’s Q2 earnings, with revenue growth stagnating and earnings delivered by cost efficiencies. While cost efficiencies are great, they cannot carry a company for long. In addition, nearly every part of the business underperformed the respective markets. I also noted a decreased focus on AI and R&D, which signals that exponential future growth may be off the table.

Based on updated guidance and trends, my DCF generated price target is lowered to $64 from $74, and I lower my rating from hold to sell as the downside risk now far outweighs the dividend and upside potential.

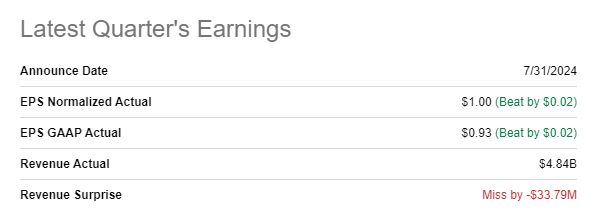

Earnings Recap

GE HealthCare reported earnings on July 31st, 2024. They reported revenue of $4.84 billion, missing consensus by $34 million and EPS of $1.00 beating consensus by $0.02.

GEHC Earnings Summary (Seeking Alpha)

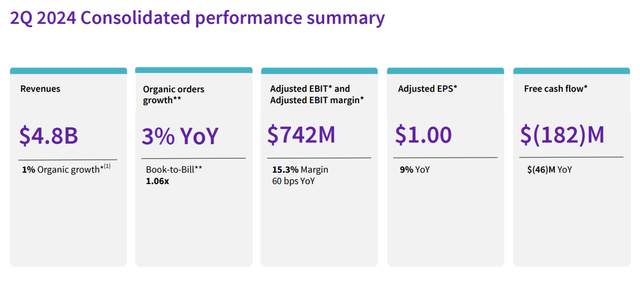

Performance was disappointing with revenue stagnating at 1%, down 3 percentage points from previous guidance, along with free cash flow deteriorating.

EBIT margin and Adjusted EPS were up, with management emphasizing the lean kaizen methodology during the earnings call as a major driver of profitability.

GEHC Q2 2024 (GEHC Investor Relations)

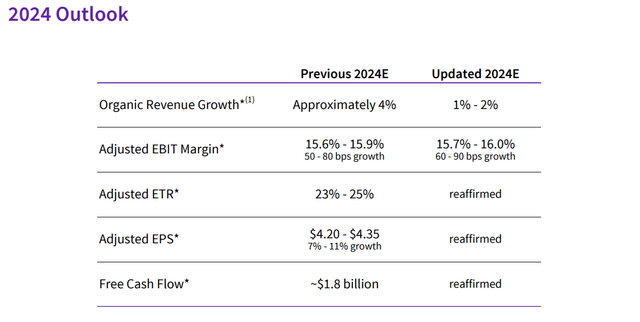

Guidance for revenue was lowered from approximately 4% to 1 to 2% for the full year, although surprisingly EBIT margin, EPS, and free cash flow were reaffirmed. This aggressive cost-cutting may save 2024, but I fear it bodes poorly for the future of the company.

GEHC 2024 Outlook (GEHC Investor Relations)

I had been looking to see GE start to catch up to the market or for AI to start to drive results for the business. Unfortunately, the business went backwards relative to my expectations.

Valuation

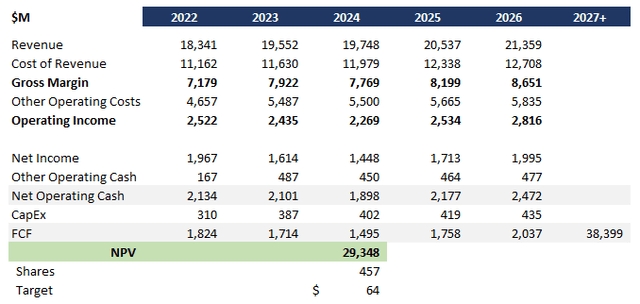

I updated my ongoing DCF analysis for changes to guidance, company trends, and industry trends. I made the following overall assumptions:

- 1% in 2024 and 4% near-term revenue growth, which aligns with slower than industry growth.

- 3% near-term cost growth assuming margin expansion from pricing and cost efficiencies.

- 7.4% discount rate based on current WACC.

- 2% long-run growth rate, with GE HealthCare short of the industry and managing a large cost base.

This DCF analysis generated a price target of $74, down more than 20% to today’s pricing and down $10 from my previous analysis.

GEHC DCF (Data: SA; Analysis: Mike Dion)

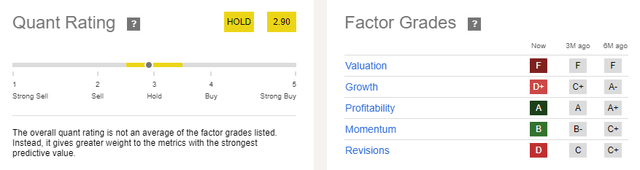

The quant ratings are also signaling an undervalued stock, with valuation receiving an F and growth a D+

GEHC Quant Rating (Seeking Alpha)

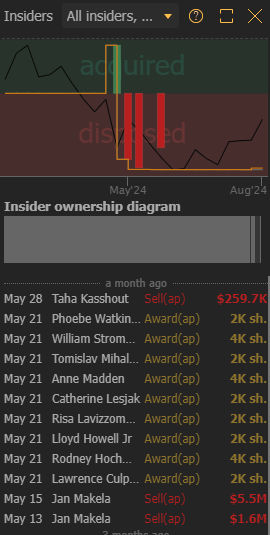

Additionally, Jan Makela, the former CEO of the imaging business, left GE HealthCare after 17 years and dumped millions of dollars of stock before he left. Certainly, not a strong sign on either count for the largest business within GE HealthCare.

GEHC Insider Trading (TrendSpider)

Continuing To Lag The Market

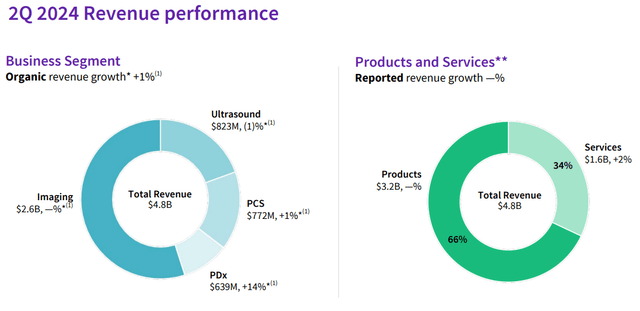

My biggest concern for GEHC has been their inability to keep up with what is a very strong healthcare market. This quarter was no different, as performance fell even faster. Certainly, China was a big component which management was quick to call out in earnings, but China is a key market and at the end of the day, it would be difficult to hit industry-leading growth rates without them.

GEHC Q2 by segment (GEHC Investor Relations)

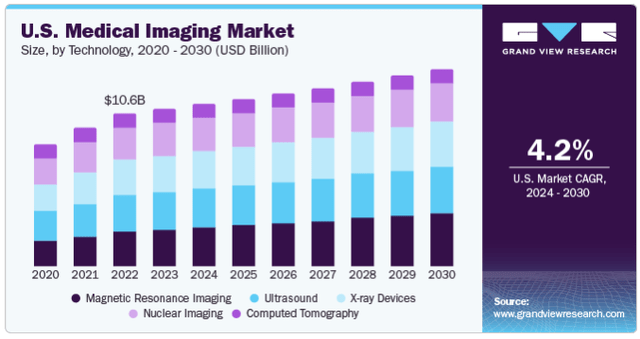

The medical imaging market, for example, is expected to grow at 4.2% through 2030, however, GE’s imaging business was flat, and the ultrasound business continued to decline.

Medical Imaging CAGR (Grandview Research)

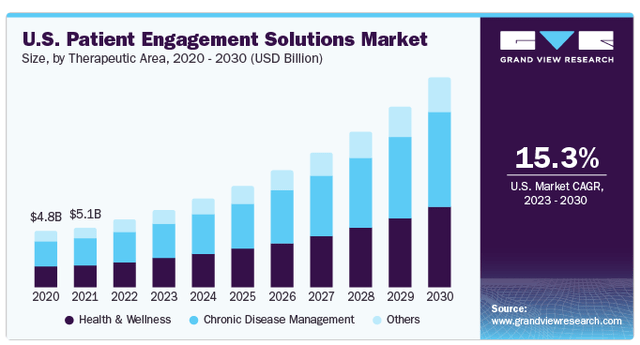

The patient solutions market is growing rapidly at an estimated CAGR of 15.3%, while GE’s business only grew at 1%.

Patient Solutions CAGR (Grandview Research)

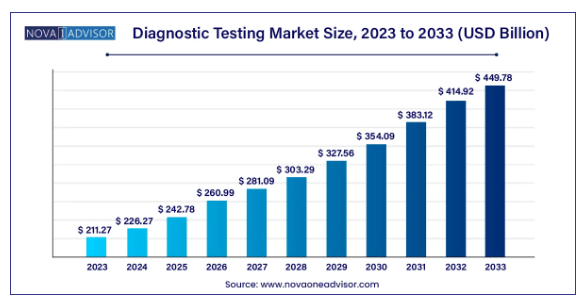

The one bright spot was the diagnostic testing market which is forecasted to grow at mid to high single digits while GE grew at 14%.

Diagnostic Testing CAGR (Nova One Advisor)

Exponential Growth Seems Off The Table

The biggest upside potential for GE was a robust AI business, as they have the scale and resources to deliver. I did feel that management was underestimating competition based on the players in the space, but the chance was still there.

Healthcare AI Companies (CB Insights)

That chance seems to be dwindling as management backed off the AI story. In addition to not having any dedicated slides and AI being essentially a footnote in the presentation, AI mentions have decreased rapidly:

Mentions of AI in Q4 2023 earnings: 13

Mentions of AI in Q2 2024 earnings: 5

Given managements desire to overcome the revenue challenges in the quarter, I believe that if there were an AI breakthrough on the horizon, it would have been spotlighted front and center.

Upside Potential

The biggest upside potential is the healthcare market itself. If GE could keep up with its respective markets, we would be looking at a very different long-term value for the company. Relative to other industries, these growth rates are exceptional, they just can’t seem to capture it.

AI also remains an upside as truly breakthrough technology could quickly grow revenue. GE HealthCare has scale and resources that few competitors can match. However this potential is reduced by both the sheer number of competitors working in the medical field as well as GE’s seemingly slow progress in the field.

Verdict

GE HealthCare’s disappointing earnings continue to show a company that is struggling to maintain market share despite a rapidly growing industry with plenty of opportunities. I am also concerned that the aggressive cost-cutting will impact future growth, further depressing the value. In addition, the prospective high-growth AI business seems to just be a footnote now.

With a DCF generated price target of $64, 20% downside to today’s pricing, as well as valuation and insider signaling, I lower my rating from hold to sell. While there could be significant potential in this business if they capitalized on the market, it just seems like they can’t get enough traction.

Read the full article here