By Scott Kennedy, produced with Colorado Wealth Management Fund.

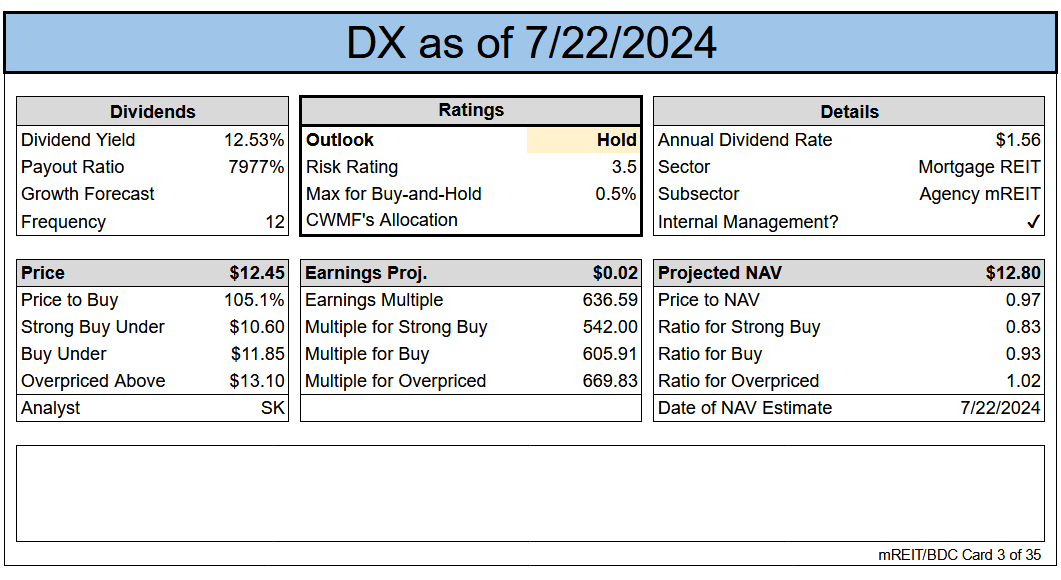

DX Commentary

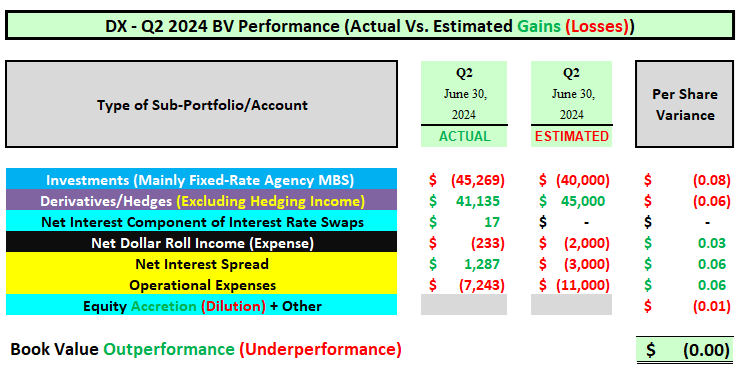

An “as expected” quarter regarding Dynex Capital’s (NYSE:DX) BV, in my opinion. DX recorded a modest quarterly BV decrease, which was correctly anticipated. DX modestly increased the company’s on-balance sheet fixed-rate agency MBS portfolio, while slightly increasing (proportionately speaking) its off-balance sheet net long TBA MBS position. The size of DX’s investment portfolio increase was slightly larger vs. what I anticipated, which directly led to a very minor quarterly BV underperformance (see table below). DX also slightly increased the company’s net (short) U.S. Treasury futures and entered into a very minor interest rate payer swaps position. The size of DX’s derivatives portfolio net (short) increase was slightly smaller versus what I anticipated, which directly led to a very minor quarterly BV underperformance (see table below). DX’s bulk issuance of common stock, in addition to continued use of the company’s “at-the-market” (“ATM”) equity offering program, directly led to some minor BV dilution (correctly anticipated).

I was a bit surprised (and impressed) by DX’s notable core earnings/EAD outperformance. This was mainly due to a combination of the following during Q2 2024 versus my expectations: 1) Outperformance within DX’s net interest income (larger MBS balance + moved higher up in coupon), 2) less severe net dollar roll loss (also moved higher up in coupon), and 3) larger decrease in share-based/equity compensation expense.

Due to DX’s notable quarterly core earnings/EAD improvement (even more than I anticipated), I believe a 2.5% percentage recommendation range “upgrade” is warranted. That said, an unchanged risk/performance rating of 3.5 for DX remains appropriate in the current environment/over the foreseeable future.

We will use many terms in this article that may be unfamiliar to readers. We’ve created a glossary for those that are interested.

BV Performance (Actual Vs. Estimated)

The REIT Forum

Change or Maintain

- BV/NAV Adjustment (BV/NAV Used Interchangeably): Our projection for current BV/NAV per share was adjusted: Unchanged (To Account for the $0.00 Actual 6/30/2024 BV/NAV Vs. Prior Projection + Matching of BV Thus Far in July 2024). Price targets have already been adjusted to reflect the change in BV/NAV. The update is included in the card below and the subscriber spreadsheets.

- Percentage Recommendation Range (Relative to CURRENT BV/NAV): 2.5% Upgrade (Due to Notable Improvement of Core Earnings/EAD).

- Risk/Performance Rating: No Change. Remains at 3.5.

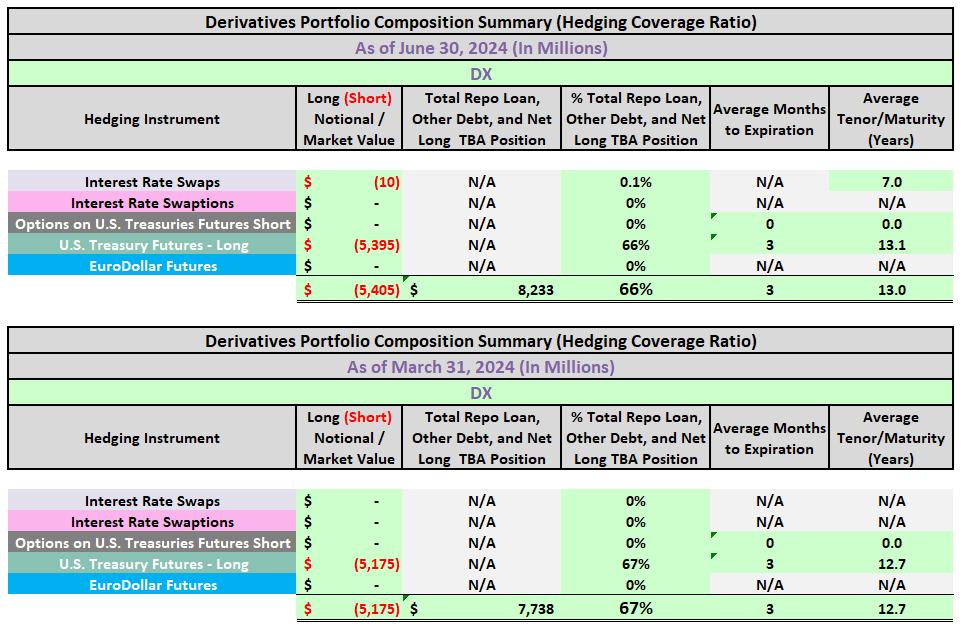

Hedging

- Hedging Coverage Ratio: Decrease from 67% to 66%.

The REIT Forum

Earnings Results

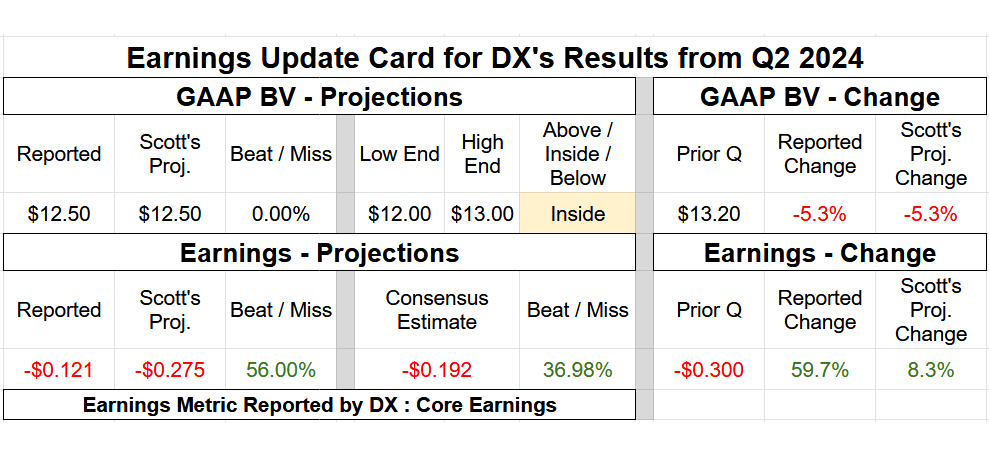

Quarterly BV Fluctuation: An Exact Match (No Variance).

- Core Earnings/EAD: Notable Outperformance.

The REIT Forum

Note: BV at the end of the quarter. Subscriber spreadsheets and targets use current estimates, not trailing values.

Valuation

The REIT Forum

Ending Notes/Commentary

As stated in prior DX earnings assessment articles, there’s a notable caveat to the company’s core earnings/EAD metric in the recent, current, and projected near-term environment. I would point out that the company’s current core earnings/EAD metric is “flawed” when trying to assess dividend sustainability. Simply put, the equivalent to DX’s current period hedging income, through the use of U.S. Treasury futures, is not a part of the company’s core earnings/EAD calculation/metric. Per GAAP, this income equivalent is part of DX’s realized gains (losses) and is excluded from core earnings/EAD. In comparison, per GAAP, current period hedging income from interest rate payer (receiver) swaps is part of a company’s core earnings/EAD calculation/metric. So, in a nutshell, a large portion of DX’s “true” operational income/gains is excluded from core earnings/EAD. This is why DX experienced a very rapid decline in core earnings/EAD during 2022-2023. DX chose not to utilize interest rate payer (receiver) swaps in lieu of net (short) U.S. Treasuries. Very important to understand.

I would continue to encourage DX to begin providing quarterly estimated REIT taxable income (“ERTI”) per share metrics in the future (the actual total ERTI figure/amount; not just the amount assigned to U.S. Treasury futures, as there are various/many reconciliations that make up ERTI versus core earnings/EAD).

DX’s projected BV increase of 2% during July 2024 (through 7/19/2024) was also an exact match versus my projection of a 2% increase.

I believe DX’s dividend should remain stable over the foreseeable future.

Read the full article here