BSR Real Estate Investment Trust (OTCPK:BSRTF), Global Medical REIT Inc. (GMRE), and CTO Realty Growth, Inc. (CTO) share 3 characteristics:

- Strong fundamentals

- Substantial variable rate debt relative to market cap

- Deeply discounted trading multiples.

Substantial variable rate debt and low adjusted funds from operations (“AFFO”) multiples are likely related. The market sees impending doom as hedges are set to expire over the coming years. What is presently hedged to cheap debt in the 3%-4.5% range looked like it would have to be reset to much higher rates, but recent changes to the yield curve suggest they might be able to keep their cheap rates.

We shall begin with a look at the fundamentals and debt loads of these 3 companies, and then follow with how their valuations have been impacted by speculation about their debt. Finally, we will conclude by showing that their variable rate debt has been largely derisked, which warrants significant multiple expansion.

Fundamentals

BSR REIT is a sunbelt-focused apartment REIT with relatively new properties in high population and job growth submarkets. We see substantial AFFO/share growth ahead as a new supply fails to meet incremental demand starting in 2026. More extensive fundamental analysis can be found here.

Global Medical REIT owns medical office properties with long-term triple net leases to healthcare operators. With the operating environment improving, market rental rates are ticking up, which along with contractual lease escalators should provide steady growth. Our full thesis can be found here.

CTO Realty is labeled as diversified, but the bulk of its value is in retail properties which are benefiting from a paucity of new supply over the last 2 decades, creating an imbalanced leasing environment favoring landlords. We anticipate substantial rental rate growth, more fully outlined here.

Large variable rate debt loads

BSR is a highly levered company with $833 million of debt against a market cap of $750 million. It appears more levered than it is when looking at market figures because it trades at a substantial discount to book. Actual debt to gross book value is 46.7%, which is still fairly high.

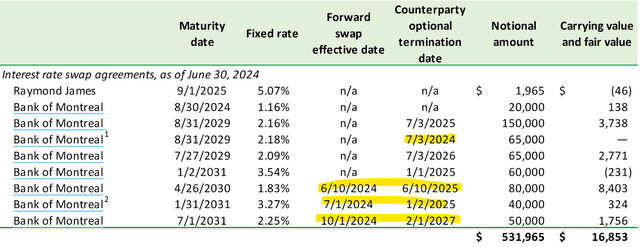

Much of that debt is a variable rate that has been temporarily fixed via swaps, as seen below.

BSRTF filing

These swaps have allowed BSRTF to maintain a very low cost of debt in the mid-3% range.

However, many of their swaps are approaching expiry in 2025-2027. As these expire, BSRTF would likely have to refinance at higher market rates. Given how much variable rate debt the company has relative to its market cap, the hit to earnings due to interest expense is potentially quite substantial. We believe this, along with a discount for being Canadian-listed, is why BSRTF is trading at a massive discount to peers.

BSRTF is trading at 15.2X AFFO while the apartment sector is at an average of 20X AFFO.

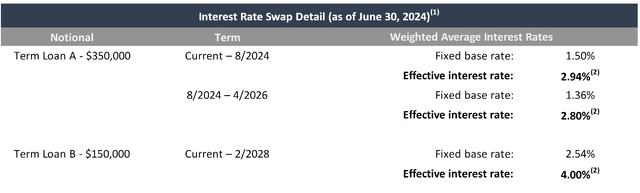

GMRE is similarly high leverage, with $500 million of hedged variable rate debt against a market cap of $689 million. Its debt is also swapped to be quite cheap with the following hedges in place.

Supplemental

The big $350 million Term Loan A swap expires on 4/2026 which could potentially increase interest expense significantly as the swapped cap of 1.3% is much lower than the current SOFR.

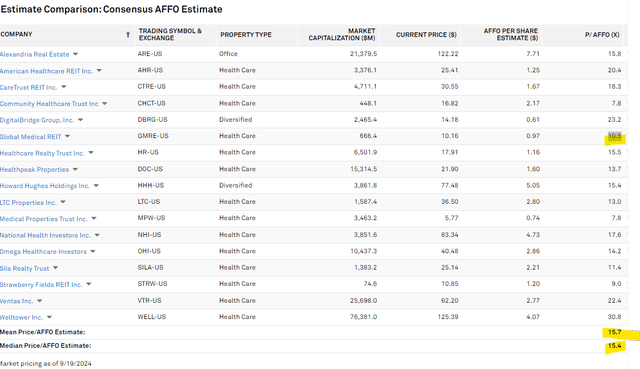

We believe worries about this impending refinancing could be why GMRE trades at such a steep discount with a 10.5X AFFO multiple compared to a healthcare sector average of 15.7X.

S&P Global Market Intelligence

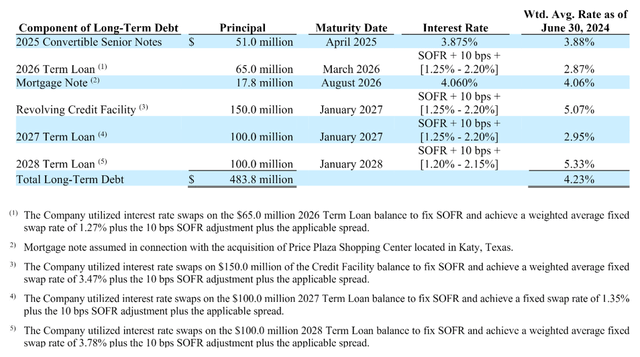

CTO Realty, as you can probably surmise from the theme, also has a rather large debt load at $483 million long-term debt against a market cap of $445 million. Again, the leverage looks bigger than it is because of the discount at which it trades. CTO’s asset value is just over $1B, so the debt to property value is still high, but reasonable.

CTO’s debt is also hedged with swaps, keeping its cost of debt at a comfortable weighted average of 4.23%.

2Q24 supplemental

As detailed in their supplemental above, the hedges expire between April 2025 and January 2028. These will presumably have to be refinanced at the then-current market rates, and worry about this refinancing event could be a big contributor to why the CTO trades at such a discount.

CTO is trading at 10X AFFO compared to the shopping center average of 17.6X.

Refinancing is being derisked

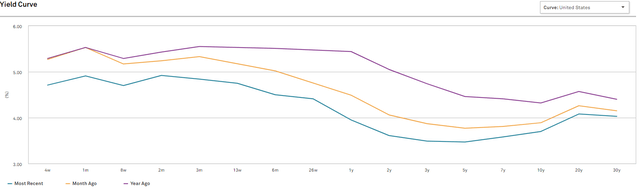

In the last month, much of the yield curve has fallen materially.

S&P Global Market Intelligence

The short end has gotten most of the buzz lately with the Fed cutting 50 basis points and as you can see above, the blue line (NOW) is almost exactly 50 basis points lower than the 1 month-ago line on the short end.

More interesting to me is what is going on in the center of the curve. 1-year rates are below 4% and 3-to-5 year rates are around 3.5%. The center part of the curve has come down a full percentage point in the last year.

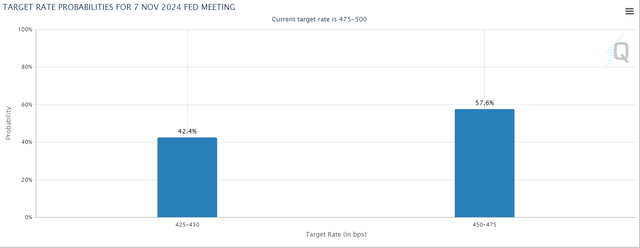

Further interest rate cuts are expected. In the November meeting, the market is calling for a 57% chance of a 25 basis point cut and a 42% chance of another 50.

CME Group

Per usual, the market’s guess is as good as mine as to how much will be cut and when, so I won’t opine on the matter.

The key aspect of this thesis is that it is broadly anticipated that there will be significantly more cutting in the next 6 months to 2 years.

This schedule of interest rate cutting is particularly relevant for the aforementioned REITs because if market consensus is anywhere near correct, it will be a much lower interest rate environment when their hedges expire.

As such, the debt refinancing boogeyman might not be so scary after all. If the yield curve moves as anticipated, these REITs will be able to refinance with minimal change to interest expense.

With this looming threat becoming much less threatening, I anticipate their multiples will move much closer to peer averages.

These companies have strong fundamentals with significant organic growth. The growth has simply not been reflected in forward estimates because until very recently it was anticipated the AFFO growth would be offset by higher interest expense. It takes a bit for the now better outlook to get reflected in consensus estimates, but if interest rates decline as anticipated, I think there will be a wave of higher estimates for 2025 and 2026 AFFO for each of these REITs.

I believe BSRTF, GMRE, and CTO will outperform the market going forward.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here