Co-authored with Long Player.

Enterprise Products Partners L.P. (NYSE:EPD) is one of the largest midstream companies in the United States. While it is diversified, its operations are centered in Texas, which puts it near two of the lowest-cost basins in the country (the Eagle Ford and the Permian).

Note: EPD is a Master Limited Partnership (‘MLP’) that issues a Schedule K-1 for tax purposes.

EPD not only provides the usual midstream functions of transportation and storage but also has additional services that allow it to make more than one profit from each customer. Source.

EPD May 2024 Presentation

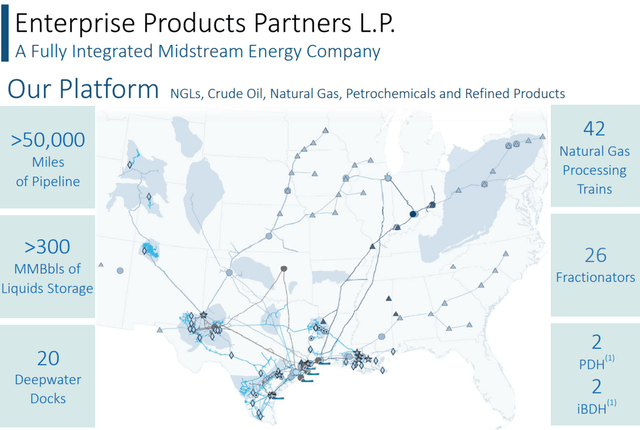

EPD is one of the few businesses that can gather the production and get it all the way to the ship for export. Many companies are rushing to join the export capability, but this company is already there, which is a huge competitive advantage.

The Handlers of Indispensable Resources

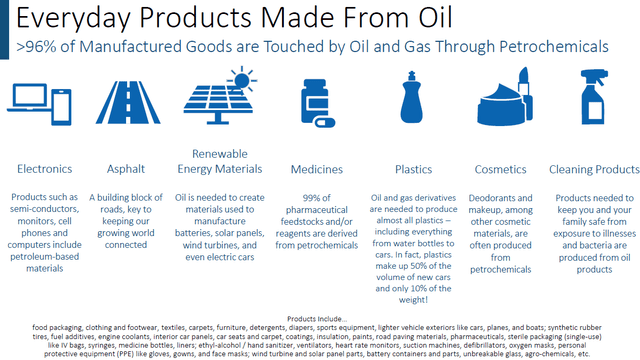

Oil and gas are necessary in almost every aspect of our daily lives, and that will not change anytime soon. The involvement of hydrocarbons is not just for energy, but everything we sit on, stand on, hold, and interact with is likely to be made up of the byproducts of petroleum.

EPD May 2024 Investor Presentation

There is almost no talk of replacing oil and gas as a source for any of the above products. It is simply not feasible.

In the history of humankind, we have never retired any source of energy completely; in this ever-hungry world, we have only added new sources to our overall energy mix. Despite obvious deficiencies compared to both oil and gas, even coal has yet to see global demand decline. Demand decline is not the same as decreasing market share, which has been happening for coal for a while. However, the demand for oil and gas is projected to grow for many years to come, simply because we cannot replace all their applications.

For these reasons, hydrocarbons have a bright future with continued demand growth for the decades to come. This makes their handlers, the midstream companies, excellent long-term investments.

Strong Balance Sheet

EPD is currently the only midstream with an A- debt rating. Management regularly ensures that the current debt profile is comfortable and that most of the debt is not due for a very long time.

With such a solid credit profile, the midstream company has no worries about access to more debt or refinancing on favorable terms. That means that the company has a lower cost of money borrowed than most of its competitors.

Even with the relatively low debt load and high debt rating, the company manages to deliver excellent returns on invested capital and returns to shareholders. The best companies in the midstream business use a minimal amount of financial leverage to achieve outstanding long-term returns. This goes against conventional thinking, where the belief is that a lot of debt is necessary for a fantastic return.

Consistent Shareholder Returns

EPD has a very long history of increasing shareholder returns.

EPD May 2024 Presentation

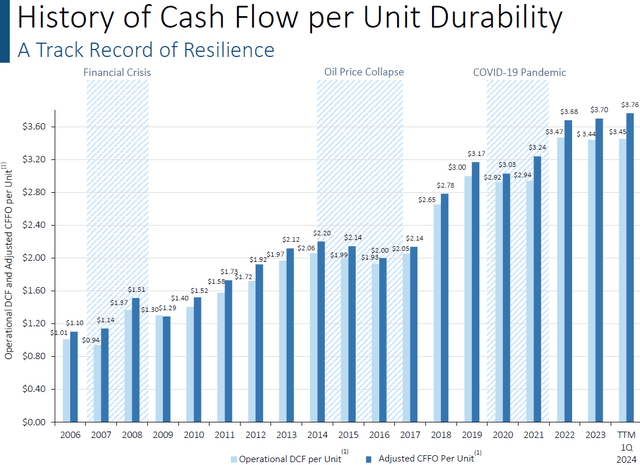

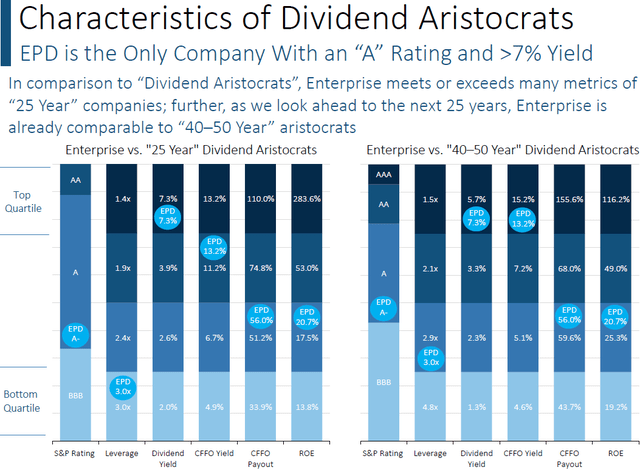

The business and profitability growth that underpins the “dividend aristocrat” status shows that this company, with its long history of distribution increases, has many more raises to deliver. EPD recently raised its distribution to $0.525/unit, reflecting a 5% YoY increase. In addition, during Q2, the partnership repurchased $40 million of its common units, bringing its total repurchases to $1 billion, of its authorized $2 billion buyback program. The company’s current yield calculates to a 7% annualized yield.

Recently, EPD has increased its distribution coverage so that it is far more conservative than it was. This allows for not only more distribution growth but also self-funded growth projects, which could accelerate distribution growth to a faster pace in the future as demand for industry products continues to grow.

The partnership has a massive footprint in Natural Gas Liquids. Ethane and propane are source materials for the rapidly growing plastics market. As long as demand for these products continues to grow, the capacity to securely process, store, and transport them will grow as well.

Immediately Accretive Growth Projects

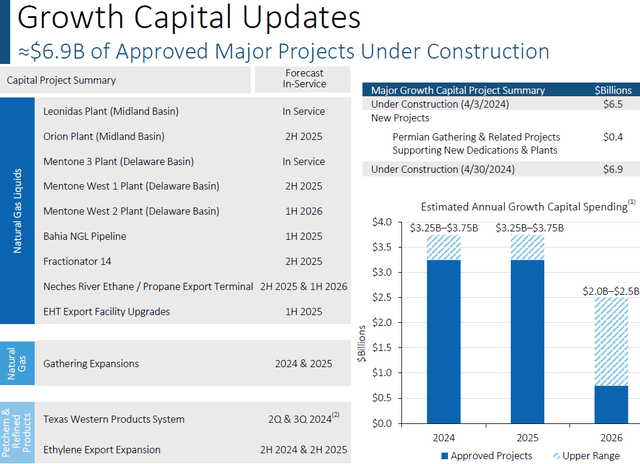

The long-term outlook for EPD’s growth projects continues to improve. As the upstream companies have recovered, there has been more demand for midstream capacity, and this partnership has been approving projects to meet those demands. Several of these projects are coming live in the next 12 months and are well-positioned to add to earnings as they are fully contracted before being placed in service.

EPD May 2024 Presentation

We are likely at the point in the upstream business cycle where there will be more demand in the coming years. Natural gas, in particular, has a lot of export capacity coming online. This could well lead to a boom in demand for midstream capacity to support all that export capacity coming online.

Enterprise Products Partners already has export capacity, which puts it ahead of many competitors, who either have projects under construction or are in the planning stages. This part of the business should become much more valuable in the future.

Predictable Earnings

Earnings for the second quarter will be reported on July 30th and should be very similar to the first quarter. The capital projects coming online should ensure about a 5% cash flow and earnings growth in the second half of the year. However, expenses from capital projects could distort that in the short term.

As long as the capital projects backlog keeps growing long-term, the long-term growth rate should likewise climb, although it is likely to remain in the single digits.

With EPD, we expect not only distribution growth but also unit price appreciation. The combined return for such a scenario is a rarely achieved feat for a company with such a long history of increasing distributions.

EPD May 2024 Presentation

The above comparison is one way to demonstrate how out of favor the midstream MLP sector is. EPD is clearly one of the best companies in the sector, with the highest debt rating and a long history of growth. Yet, it is undervalued compared to other industries and its C-corp peers despite its tax-deferred income potential. The yield alone is industry-leading, and it’s far better covered than is the case for many other dividend aristocrats.

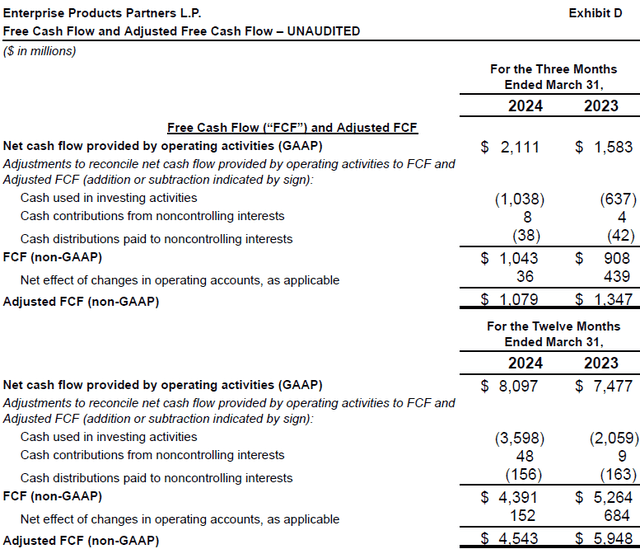

Growing FCF & Attractive Valuation

EPD management has decided to invest more cash flow into growth projects. That should surprise no one because one of the reasons for previous FCF (Free Cash Flow) growth was the ability to self-finance growth projects when demand arrived. We note that with EPD, management is on the same side as the investors, as insiders own 32% of the units outstanding.

Those expenditures mean that free cash flow will eventually begin to grow again once the initial build-up of demand is over.

EPD Q1 2024 Press Release

In the meantime, the yield of the enterprise value on the reduced cash flow remains in the middle to upper single digits, which is extremely high for an income vehicle. This also points to the fact that the company is well-positioned to grow while paying a generous distribution — that rarely happens with market-perceived income vehicles.

EBITDA for the last twelve months was roughly $9.5 billion. The market cap is in the $63 billion range, with debt at ~$30 billion. That makes an enterprise value in the $93 billion range. That is very cheap for a company that has generated nearly $10 billion in EBITDA in the past twelve months. Historically, that enterprise value should be closer to about $120 billion, which implies a fair amount of appreciation ahead.

As a growth and income play, EPD offers both income safety and total return potential. Therefore, it is an excellent investment for both growth and income investors in these uncertain economic conditions.

Conclusion

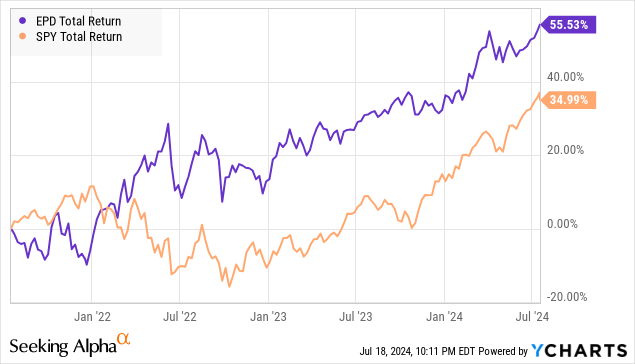

EPD is a unique midstream MLP with a track record of growing distributions and creating shareholder value. Since the economic recovery from the global pandemic, the energy sector has been in the spotlight. Despite elevated interest rates, this asset-rich business continues to outperform the broader market.

Our economy faces uncertainty, and our Investing Group is preparing by fortifying our portfolio with defensive sectors and security. EPD operates a wide network of critical assets across strategic locations. Its growing asset footprint, insensitivity to commodity prices, and the regulatory and high-cost barriers for new competition to enter this business provide a pathway for continued distribution growth for shareholders. We are scooping up this 7% tax-advantaged yield while the market continues to undervalue this MLP.

When it comes to retirement, having key holdings in your portfolio (those that you can set and forget in many regards) can massively reduce your stress and boost your enjoyment. Most of us don’t enjoy fretting and worrying over the health of our portfolio, so having rock-solid holdings can reduce the workload and dial down the worries. This way, you can enjoy the beautiful parts of your retirement — hobbies, travel, time with loved ones, and reduced stress due to not having to punch the clock daily. EPD can and will provide you with outstanding income, which enables you to unlock countless possibilities.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Read the full article here