Investment Rundown

The growth of the share price for Accuray Incorporated (NASDAQ:ARAY) has been impressive. The company has been able to display itself as a growth opportunity to investors seeking exposure to the healthcare equipment market. The last report showed ARAY able to grow the revenues by 22.8% YoY, and as we aren’t far off from the next report I think that we will see momentum maintained and that constitutes a buy in my book.

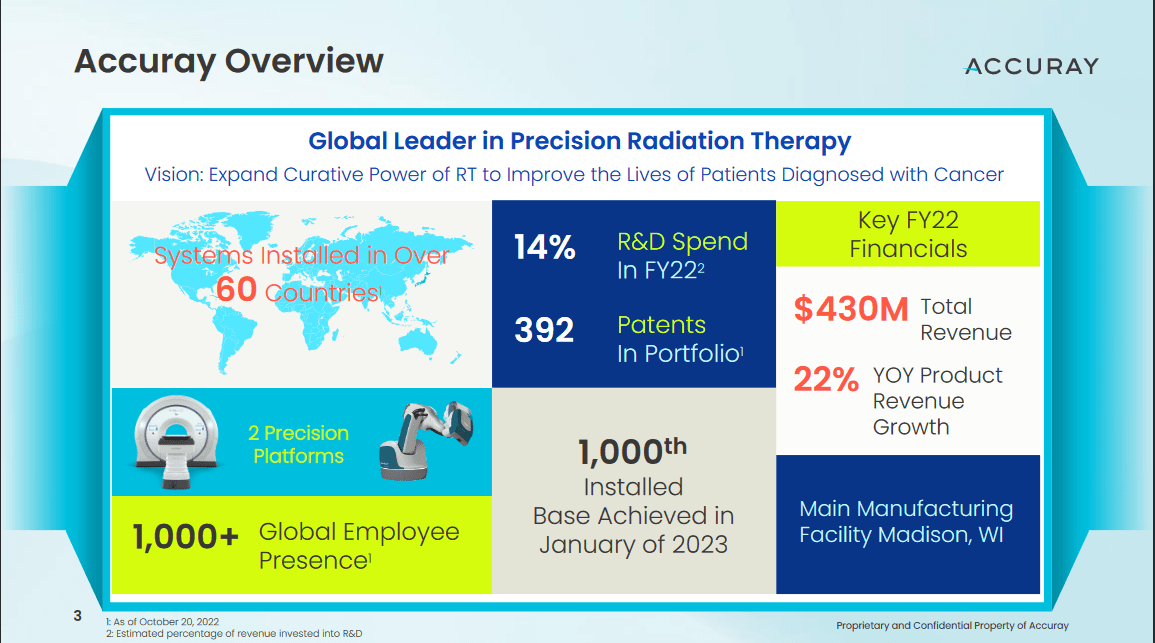

The valuation is appealing and ARAY is becoming a leader in the precision radiation therapy market. The company has managed to gather up 392 various patterns and has R&D expenses relatively low still at 14%. The market outlook is very positive, and I think ARAY will be a big winner in the years to come. It has already had incredible growth in the last 12 months, but I am not afraid to be rating it a buy nonetheless.

Company Segments

ARAY engages in the design, development, manufacturing, and distribution of cutting-edge radiosurgery and radiation therapy systems. These innovative systems play a pivotal role in the battle against tumors, shaping the landscape of medical care across diverse regions including the Americas, Europe, the Middle East, India, Africa, Japan, China, and the broader Asia Pacific.

Company Overview (Investor Presentation)

The technology that ARAY is providing is widely used and an incredibly important part of treating cancer patients, as around 60% undergo radiation therapy. The differentiated solutions that ARAY has been working on have lent them able to grow revenues quickly and also grow orders for it, which was up by 3% YoY. The gross orders constantly were at $76 million, and I do think we will see a further increase in the coming report here. Depending on how much, will likely impact the share price to the upside?

Products (Investor Presentation)

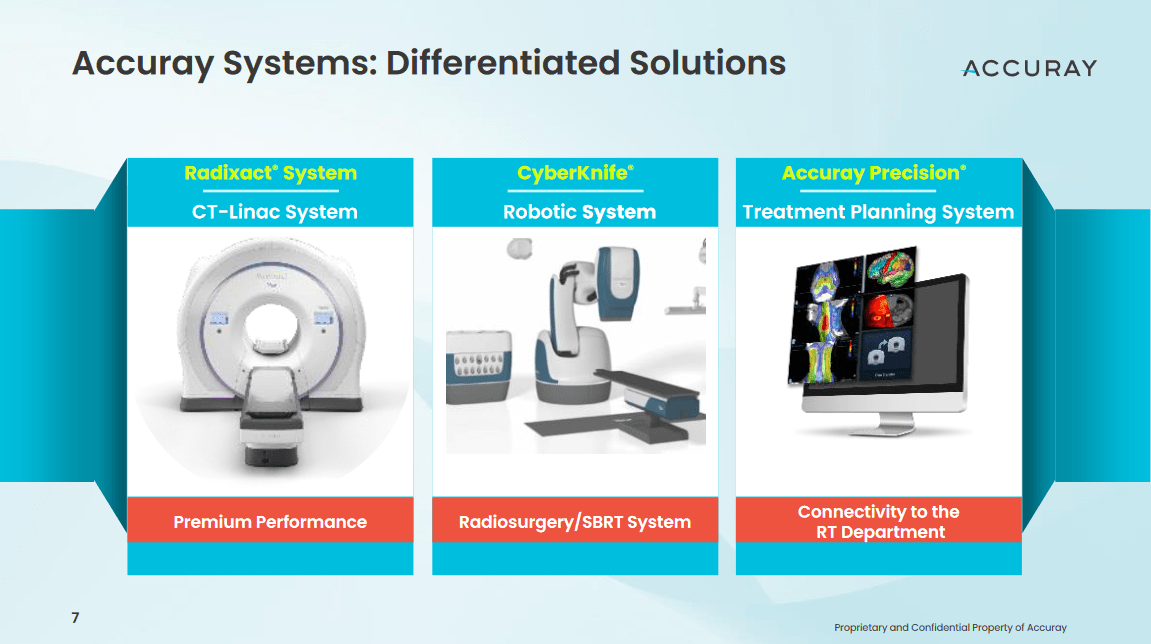

At the core of Accuray’s groundbreaking offerings lies the CyberKnife System. This robotic stereotactic radiosurgery and stereotactic body radiation therapy system has been widely adopted and used in the field. The CyberKnife System represents a fusion of precision, technology

Market Overlook (Investor Presentation)

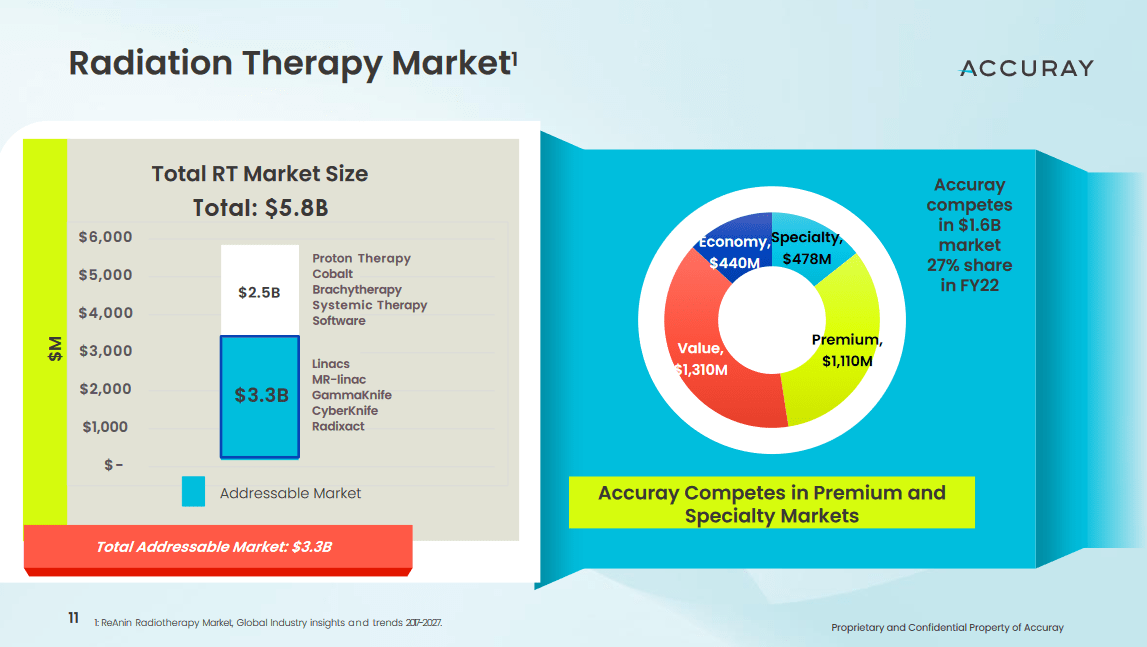

Looking at the market that ARAY can tap into, it is quite massive. Valued at $5.8 billion, the progress that ARAY can make in terms of speeding up production will have an immediate effect on the revenues. Demand and size to tap into are there, and it’s more now up to ARAY to satisfy that. Some of the big markers that are helping this grow are China and Brazil. China alone stands at a $500 – $600 million market to tap into, one that is also expected to grow around 12% annually in the next several years. Given that ARAY has already gathered up an international customer base, it seems they are in a strong position to be able to move into counties like China and Brazil without a lot of upfront expenses.

Q2 Highlights (Earnings Presentation)

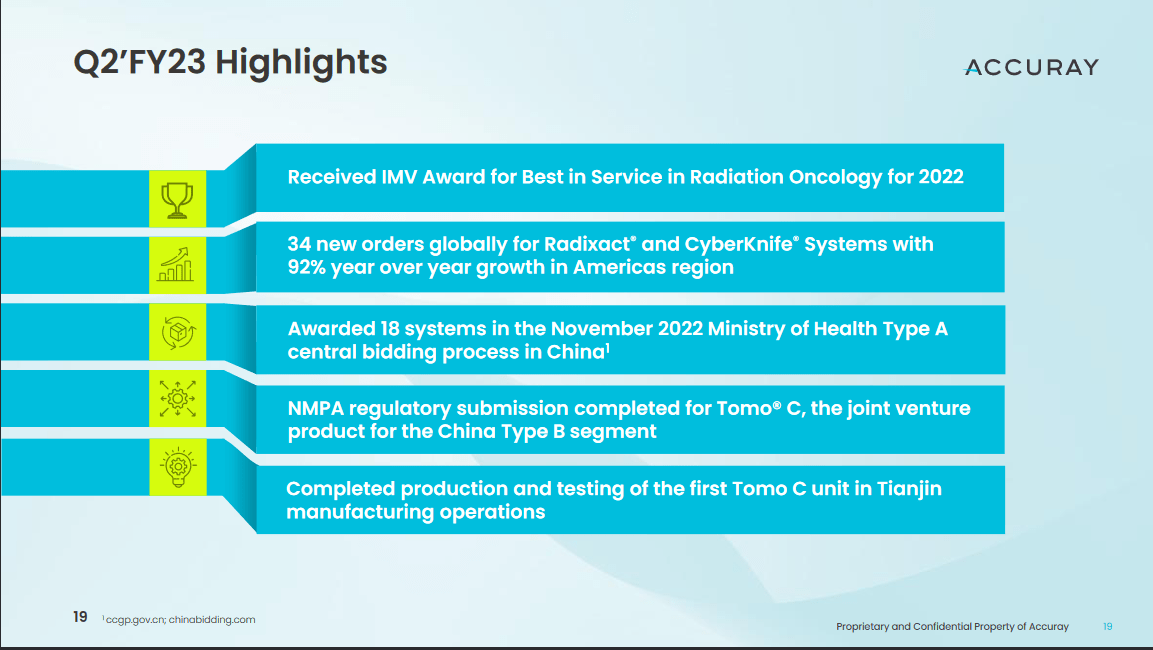

Going forward, seeing strong demand from the American market seems reasonable, both in terms of that it makes up nearly half of the total market and also that the capital and investments in this region seem to outdo other parts of the world. Just looking at the last report from ARAY they experienced a 92% growth for CyberKnife orders in this region.

Risks

Efforts to enhance margins continue to be a focal point for the company, as it grapples with ongoing challenges stemming from its supply chain dynamics. Notably, the gross margin faced a notable decline, shrinking by 340 basis points compared to the previous year and a more substantial 460 basis points every quarter, settling at 32.8%. This margin contraction appears to be influenced, at least in part, by a shift in the product mix.

Focus Areas (Investor Presentation)

Navigating the intricate landscape of medical technology, ARAY experiences a degree of variability in the quarter-to-quarter composition of its product offerings. Specifically, the blend of its advanced CyberKnife and Radixact systems can fluctuate, creating an intricate dance of quarter-to-quarter dynamics that can impact financial metrics. This underscores the inherent complexities of the healthcare industry, where the interplay of technological advancements and market conditions can shape financial outcomes.

Industry Comparison

Going over the valuation of ARAY we can quite quickly see that the bottom line is negative, however, by 2024 as demand picks up and ARAY can focus on earnings growth it’s estimated to be around $0.1 instead. This would value ARAY at a P/E of 41, which is too high by most standards to pay for any company. But as the market share that the company has is strong and demand is picking up, the expected strong EPS growth YoY seems valid. A 20% EPS growth in the coming several years would indicate that right now, ARAY does make sense as a long-term investment.

An EPS of $0.21 would put ARAY at a P/E of 20, which is fair given the growth and business model it has. With a 20% CAGR of the EPS, we would hit that target in 2028. That is a few years out, but as the company grows its share of the market, I don’t think they are likely to give too much up either. As orders are amounting, ARAY seems poised to be a leader in the space. That means paying a premium now to capitalize on future returns is worth it.

Final Words

For investors that want exposure to a rapidly growing market and one that will stay in high demand, then ARAY offers that. They are a part of the radiation therapy market, one where they hold a strong share of the market and have recently seen strong order growth too.

I think that long-term, the company will do extremely well and yield a solid ROI for investors. As a result, I am rating ARAY a buy right now.

Read the full article here