AIA Group Limited (OTCPK:AAIGF)(OTCPK:AAGIY) was a stock we kept away from because we weren’t keen on anything dependent on China, as explained in our previous coverage. However, Chinese exposures have started to bottom out, and there is less temperature around the geopolitical considerations of Taiwan, with work on relocating or diversifying strategic reliance on Taiwan being a clear part of the European and US agenda. Moreover, there has, in general, been an economic reckoning in China that may drive sufficiently home the need to play at least a little nice on the global stage, having been one of the biggest beneficiaries of globalization in the world. AIA is an interesting pick on the basis of its business growth as well as its capital allocation, where they are doing a considerable buyback of around $5 billion this year, which is almost 10% of the company’s market cap. Still, as an insurance exposure with fixed income investments in an ailing economy, we aren’t crazy about their reserve portfolio. We wouldn’t be too optimistic about their other assets either. We prefer what is going on with less financially related exposures like Jardine Matheson (OTCPK:JMHLY) in a Chinese rate cutting environment. Within insurance, there is no competition in our view between a more complex Chinese equity over a similarly growing European insurer, of which there are several.

Results Discussion

The annual report contains the most comprehensive financials and not just the KPIs.

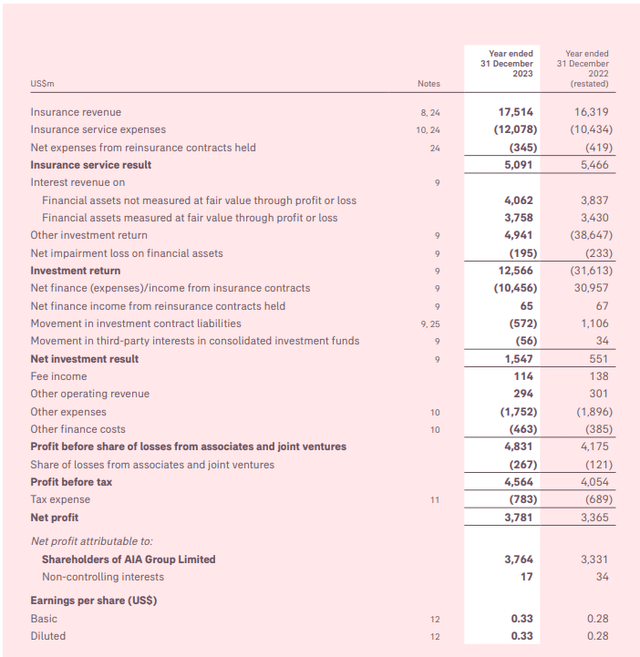

IS Snapshot (FY AR)

Investment return was up as the company’s financial investments, namely equity and also fixed income, performed better in the 2023 year than it did in 2022. Both asset classes performed badly in China, despite the fact that rates have been falling, although not as dramatically as expected for an economy whose construction markets, a plurality of GDP, are getting decimated. Ultimately, China’s status as an investable nation declined significantly in the wake of the fractiousness of geopolitics post Ukraine invasion.

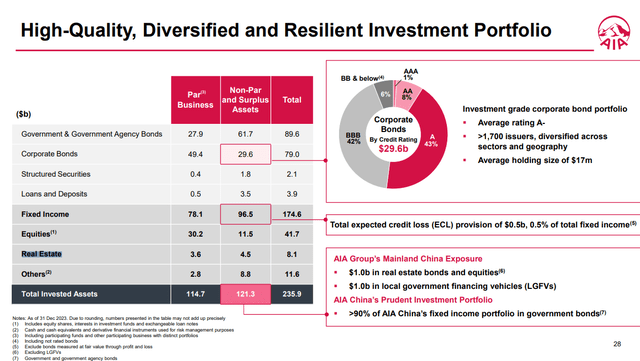

Investments (FY Pres)

As of the annual report, where the data is provided, investments remain substantially in China.

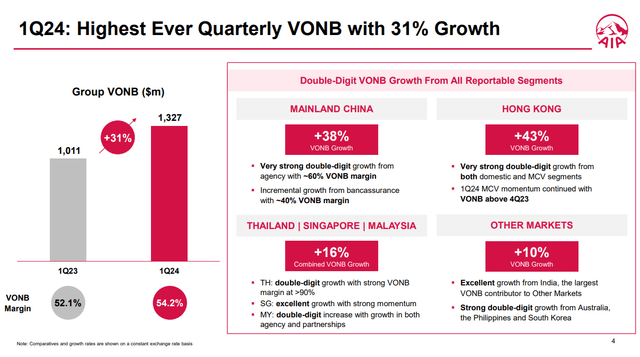

VONB Growth (Q1 Pres)

Getting to more updated figures, VONB is continuing to grow, which should support higher insurance revenues as those premiums become earned. The accounting figures will lag VONB as a KPI due to the need to recognise the insurance revenue over time. In general, AIA has been a grower now hitting record levels, and despite economic pressures in the Chinese economy, demand has been sufficient for their products.

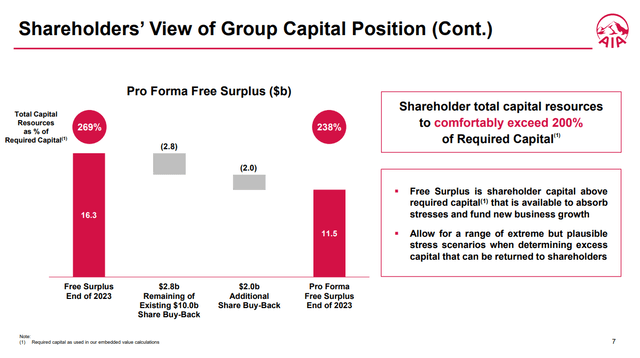

TTM PEs are still quite high at almost 20x, although payouts are looking strong with almost 10% in buyback yield in addition to a dividend. The company has pretty high payout policies on what it deems to be surplus liquidity over capital requirements that can be dispensed to shareholders.

Buybacks (Q1 Pres)

Growth in earnings will depend on more efficient underwriting, which has struggled from higher service costs in 2023, as well as a recovery in Chinese financial markets. The latter is where we have some concerns, and we don’t think appetite for Chinese securities is likely to rise. Moreover, while duration effects would be playing in AIA’s favour, the lack of appetite and capital appreciation as an investment return lever doesn’t gel well with an increasingly accommodative monetary regime, where fixed income investments will roll over into a market with progressively lower underlying “risk-free” rates from the People’s Bank of China.

Bottom Line

It does appear though that Chinese markets are beginning to bottom out a bit, with the bulk of negative fund flows likely coming to an end as allocators find comfortable new equilibriums. Chinese equities may be worth considering for some investors again, although you need a risk appetite.

AIA manages solid growth, but we think there are better propositions that carry the same China risk. We would be underweight financials in the region as the structural economic problems, and also emerging demographic issues, mean there will be downward pressures on rates in our view. We don’t think this will preclude growth, but it limits in from a 20x TTM PE. If we had to pick something in China, we’d go a different direction with Jardine Matheson, although AIA is a more consistent grower where some of Jardine’s interests are on the up and others on the down. On another note, there are cheaper insurance picks in China, like PICC (OTCPK:PPCCF). Even taking forward PEs, which are highly tentative on China’s market performance and these insurance companies’ investment income, AIA is looking pretty expensive at 13x or so forward PEs against other picks which are well below 10x. AIA’s growth in premiums is considerably more, but it’s not nonexistent in peers, and all carry the stain of being a Chinese equity in a day where concerns around capital control, economic nationalism and other geopolitical concerns are relevant for capital allocation decisions. Between AIA and a growing European insurance pick like Allianz (OTCPK:ALIZF) whose value of new business grows at comparable rates to AIA and which trades cheaper, it’s a no-brainer. Especially with those forward PEs being questionable as major assets like fixed income continue to tumble in China affecting rebound potential for the investment portfolio, AIA is still not for us even though we expect continued and consistent VONB performance in the coming quarters.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here