The headline figures for AMMO’s (NASDAQ:POWW) first quarter 2024 results looked pretty bad. AMMO saw a massive YoY drop in revenue from $60.8 million in the prior quarter to $34.3 million in the current quarter. Just taking this at face value may lead one to think that the company is in dire straits and that its stock would continue on its free-fall.

However, POWW stock has been relatively unchanged since that announcement. The stock is only slightly down from the pre-earnings close of $2.07 to the current price as of writing of $1.96. That is a small decline of 5.6% in two weeks. I view the divergence between headline news and price action as a signal that there could be a potential buying opportunity.

Bad Top-line Revenues Hide the Transformation

Looking underneath the hood though shows that the company is weathering the current macro-economic conditions quite well. It shouldn’t be news to anyone that consumers worldwide have been feeling a pinch in their pocketbooks due to inflation. Coupled with the threat of a recession, consumers have been dialing back significantly their discretionary spending.

One such spending that is seeing a hit is firearms and related spending. As a leading provider of ammunition and its components, AMMO has these factors impact its revenues.

This is why the company has undergone a pivot and corporate restructuring at the beginning of the year. Looking at AMMO’s 10-Q results, this strategic pivot is starting to show results. The company’s adjusted Net Income has been solid despite the huge drop in top-line revenue. AMMO reported an adjusted Net Income per Share of $0.05 compared to last year’s $0.07.

The main driving factor for these results is the change in the sales mix. By focusing on sales from higher-margin Ammunition Casings, the company was able to increase its gross margin percentage to 40.9% compared to 29.8% in the prior period. So while top-line revenue declined massively due to the drop in sales of commoditized ammo offerings, Ammunition Casings doubled from $3.3 million in June 2022 to $6.2 million in June 2023.

Revenue Mix (Company 10-Q)

Company executives expect the growth in this casings business to continue in the foreseeable future. They believe that casings could grow to be 25% to 35% of business based on statements made during their earnings call. Currently, casings represent about 18% of AMMOs $34.3 million revenue indicating a long runway for growth.

AMMO also expects casings prices to remain stable thus continuing to preserve this high margin. The new 185,000 sqft manufacturing plant brought online last year also ensures the company has room to drive further process improvements and efficiencies in scale. To double its castings business in the span of a few months amidst a tough economic environment shows that AMMO has a good management team on hand.

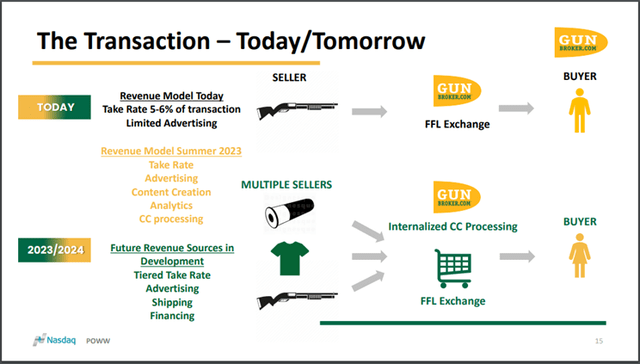

GunBroker is Another Source of Upside

GunBroker is the company’s online marketplace dedicated to the lawful sale of firearms and related products. It essentially works like a two-sided marketplace with an added layer of compliance due to the nature of the products being sold.

Based on the company’s latest 10-K filing, there are approximately 7.8 million users and 35,000 federally licensed firearms dealers/transfer agents on the platform. One of the key things when investing in a company that I look for is an “Economic Moat”. GunBroker has this through its expertise in navigating the complex regulatory requirements when purchasing firearms and related products. In other words, I don’t envision Facebook marketplace (META) or Amazon (AMZN) entering this niche market anytime soon.

AMMO is currently in the process of improving the GunBroker platform through several key initiatives. One of these initiatives is to improve upon the consumer experience such as ensuring seamless transactions following all regulatory requirements, improving the UX to suggest products, and even a valet service for Gun sales.

GunBroker is also targeting margin expansion via Seller driven advertisements and lifestyle content creation to increase product awareness. The final initiative is centered around building out proper shopping cart functions, carding, and the establishment of financing options.

Gunbroker future state (Company presentation)

Ammunition for Stock Buybacks

AMMO’s stock is currently trading near all-time lows. No doubt, a lot of the investor pessimism levied on POWW stock is due to the unfavorable macroeconomic environment.

Looking at the latest data from the National Shooting Sports Foundation’s analysis of FBI background check data, we can see that 2023 has so far been a terrible year for the industry. In Q2 2023 there were 3.6 million sales which was a decline of 6.7% from last year and a 67% decline from 2020’s all-time high.

This decline in sales is nothing to be surprised about. Firearms have always been a somewhat cyclical industry. When investing in cyclical stocks like POWW, I always like to see how they perform in adverse economic environments. It’s easy to perform well when the economy is hot. But it is a lot harder to do the same in tougher environments.

So far, I like how AMMO has been navigating this inflation/recession combination. The company has been making smart long-term decisions while generating cash in the present. In the latest quarter, the company generated $13 million in cash from operations more than double the $5.2 million last year. This should support the company’s stated buyback goal of $30 million worth of shares. The company repurchased 739,000 shares this last quarter.

Conclusion

AMMO’s stock is currently trading at extremely depressed valuations making this a potential value play for when the economy turns around. Firearms and related product sales tend to be cyclical. While we are now currently on a downturn compared to the highs of 2020, it should still be very clear that the over-all trajectory is still upwards.

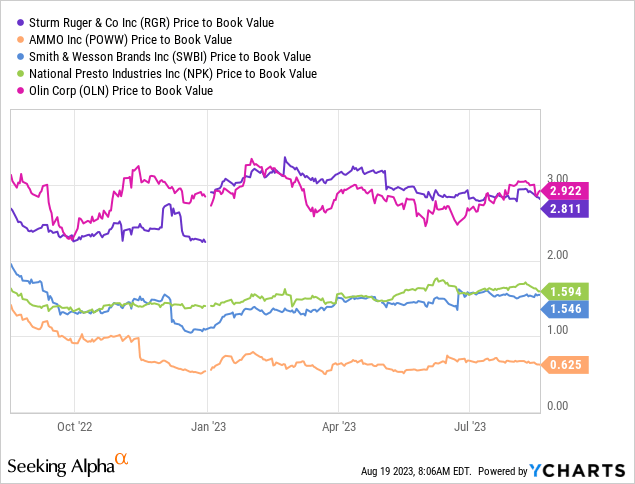

AMMO stock has an upside simply from a valuation perspective. Looking at AMMO’s peers, it can be seen that the company is trading at a massive discount on its book value. Simply by using a book value multiplier of 1x, I arrived at a target price of $3.14 which is around 50% above the current price. This is still fairly conservative in my view as the company’s peers in the firearms industry trade at 1.5x to 2x book value.

Of course, there are risks to this investment in the form of legislative risks (i.e. “gun control”) and a long recession. But I believe that POWW stock is a BUY given the cheap valuation and potential upside scenarios from its shift to higher margin products and GunBroker.

Read the full article here