Ardagh Metal Packaging S.A. (NYSE:AMBP), the beverage metal can manufacturer, is going to report its Q2 results in late July. The quarter comes after Ardagh has reported turbulent financials in the European market, resulting in a weakening profitability for the company in the past couple of years.

Previously, I wrote an article on the company with the title “Ardagh Metal Packaging: Debt Levels Pose A Risk“. In the article, published on the 23rd of August in 2023, I initiated Ardagh at Hold, noting the company’s incredibly high debt and weakening profitability, but corresponding valuation. Since, the stock has returned 17%, trailing S&P 500’s return of 25% in the same period by a small margin.

My Rating History on AMBP (Seeking Alpha)

Q2 Earnings Preview: Watching the European Performance

Ardagh is going to report the company’s Q2 earnings on the 25th of July in pre-market hours. The company anticipates adjusted EBITDA to come in at around $170 million, as told in the Q1 earnings call and explained to better strength in both American and European operations. The figure compares to $134 million achieved in Q1 and $151 million in the prior Q2 – after turbulent and weakening profitability in most of the recently reported quarters, Q2 is expected to show signs of improvements.

Wall Street analysts have adjusted estimates into Ardagh’s own expectations corresponding to an expected normalized EPS of $0.05 and a revenue estimate of $1.32 billion, a 5.0% growth year-over-year.

The second quarter comes after Ardagh reported only a 0.9% revenue growth in Q1. Ardagh has experienced weaker demand especially in the European market as Ardagh’s customers have destocked inventories to adjust for slightly slower consumption. While shipments already grew by 3% in Europe in Q1 after a sharp decline in Q4, profitability in the market still took a hit due to higher operating costs. The North American and Brazil markets have performed more stably, showing improving growth in markets in Q1. Ardagh seems confident in an upcoming recovery in Europe as customers seem to have churned through excess inventories, and as the positive shipment trends in Q1 have followed into at least April.

As turbulent macroeconomic conditions persist in Europe with an already turbulent financial past in the market for Ardagh, I believe that investors should still watch the market’s performance closely in Q2 – with the company’s high remaining debt generating healthier margins is critical for Ardagh, also making a recovery in the market critical.

Is the High Dividend Safe?

On the surface, Ardagh may seem incredibly attractive due to its very high dividend – currently, the stock yields 11.11% in dividend payments which the company has kept despite the earnings turbulence.

I believe that the dividend isn’t safe. Subtracting working capital changes Ardagh’s trailing free cash flow stands at just $37 million ($535m CFFO – $193m Change in Net Operating Assets – $305m CapEx), the earnings currently only provide cash flows for a $0.06 dividend instead of the current $0.40 before even accounting for the company’s increasingly high debt.

As such, I believe that the $0.40 dividend is highly unsustainable at the current cash flow level, as Ardagh won’t be able to push for higher cash flows from lowering the working capital level sustainably.

The long-term debt of $3509 million, of which $224 million is in the current payable portion, makes the dividend safety worse – the trailing interest expenses of $157 million already push levered cash flows negative with Ardagh’s $173 million trailing debt payments at the current earnings level.

Improvements should happen to cash flows in the short- to mid-term. The European market’s recovery should aid profitability quite well also raising cash flows considerably. Also, Ardagh has plans to lower the growth-related capital expenditures into just $100 million in 2024 and lower them further in 2025, as told in the Q1 press release, aiding cash flows quite well. I still believe that investors should remain cautious of the current dividend level’s safety with the currently bleak cash flow view, though.

Ardagh’s thin ability to pay out the dividend also makes upcoming earnings more critical for investors, as the profitability improvement is quite urgently needed for the dividend not to be cut.

Updated Valuation

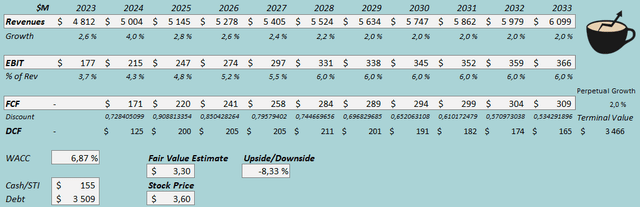

I updated my discounted cash flow [DCF] model to estimate an updated fair value for the stock. In the model, I now estimate a 4% revenue growth in 2024 in line with Ardagh’s guidance, followed by a gradual growth slowdown into 2% perpetual growth – the industry’s growth outlook is overall quite slow over the long term, and Ardagh’s slower growth investments don’t allow for very high growth. The growth estimates are down slightly from the previous model.

With the European market’s recovery, I estimate Ardagh’s profitability to rise back in the coming years into an EBIT margin of 6.0%, near Ardagh’s 2019 operating margin of 6.3% – while a better margin could be possible, I believe that the margin is a fair estimate due to Ardagh’s low gross margin level.

Due to Ardagh’s low planned investments and high amortization, I now estimate the cash flow conversion to be great going forward.

DCF Model (Author’s Calculation)

The estimates put Ardagh’s fair value estimate at $3.30, 8% below the stock price at the time of writing – I don’t believe that the current stock price provides a very great risk-to-reward for the investment, especially with the great dividend being in risk of being cut considerably disappointing shareholders. The fair value estimate is up slightly from $3.18 previously.

The valuation is still extremely volatile due to Ardagh’s debt, and higher growth or margin recovery could still make the stock attractive. On the other hand, continued struggles can make the stock increasingly unattractive.

CAPM

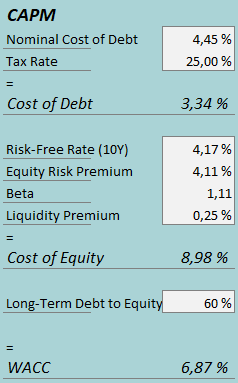

A weighted average cost of capital of 6.87% is used in the DCF model. The used WACC is derived from a capital asset pricing model:

CAPM (Author’s Calculation)

In Q1, Ardagh had $39 million in interest expenses, making the company’s interest rate 4.45% with the current amount of interest-bearing debt. I now estimate a long-term debt-to-equity ratio of 60%, up from 40% previously.

To estimate the cost of equity, I use the 10-year bond yield of 4.17% as the risk-free rate. The equity risk premium of 4.11% is Professor Aswath Damodaran’s estimate for the US, updated in July. Seeking Alpha estimates Ardagh’s beta at 1.11. With a liquidity premium of 0.25%, the cost of equity stands at 8.98% and the WACC at 6.87%.

Takeaway

Ardagh is looking to report a gradual recovery in the European market after turbulence in the past couple of years from customer destocking and a worse macroeconomic sentiment, already expecting EBITDA growth for the soon-to-be-reported Q2 in the market. I believe that investors should keep a close eye on the quarter – the European market’s recovery is critical to recover Ardagh’s profitability, and the incredibly high debt still leverages the investment very widely. Ardagh has stuck with a potentially unsustainably high dividend, making earnings improvements even more critical in the short term.

The stock’s valuation isn’t attractive yet with Ardagh’s high remain debt. With a fairly balanced risk-to-reward, worsened by the potential of a dividend cut, I still remain at a Hold rating for Ardagh Metal Packaging, but note the potential threats.

Read the full article here