Bar Harbor Bankshares (NYSE:BHB) is a regional bank in the New England area and a stock that has been relatively stable. Now, along with many in the sector, it is at a 52-week-high. At these levels, we are neutral on the bank, but we do like that the bank continues to raise its dividend (apart from in the pandemic-impacted year), making it attractive for dividend growth investors.

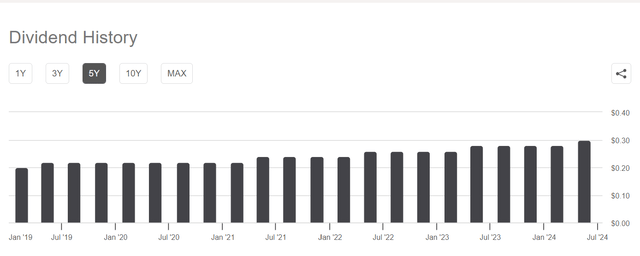

Seeking Alpha BHB Dividend History

Regional bank stocks had a tough 2023, but we got bullish in H2 2023 for a rebound in 2024. With a bit of a rotation recently out of big tech and into other sectors, bank stocks have done well. We like BHB and think if and when it pulls back into the $20’s, it is one to consider for income. The yield is 4% here, and as you can see, it reliably grows the dividend. The company just reported earnings, and the bank is performing well in this tough macro environment. We continue our coverage of regional bank Q2 earnings with this quality company.

Top line stabilizing

In its just-announced quarter, Bar Harbor saw revenues that were down slightly from last year, but better than expected. This came on an increase in loans and margins during Q2. Revenues reached $37.4 million, reflecting a mere 1% year-over-year decline. Margins for regional banks have bottomed as a whole, and we are on record with that position. Net interest margin was 3.09% compared to 3.22% in the second quarter of 2023. However, it was down from 3.14% in Q1 2024 as well.

As we said, not every bank is the same. The decrease was primarily driven by higher cost of funds, partially offset by lower borrowing costs. The yield on loans grew 42 basis points to 5.41% up from 4.99% in the same quarter 2023. Costs of interest-bearing deposits increased to 2.35% from 1.45% in Q1 2023 driven by the competitive pricing within the interest rate environment and change in deposit mix. Combined with non-interest income that grew $0.6 million to $9.6 million, we saw net income of $10.3 million or $0.67 per share. While this is down from last year, the stock is at highs, and it is on hopes for a better environment in the near future. This comes as loans grow and deposits are holding up.

Bar Harbor loans and deposits

We were encouraged by the loan growth at the bank, especially in the commercial segment. Total loans grew $52.5 million or 7% on an annualized basis. Very promising was that commercial loans grew by $68.6 million or 14% annualized. This was driven by a $59.9 million, or 15% increase in commercial real estate, and an $8.7 million, or 8%, increase in commercial and industrial loans. In contrast, residential loans decreased by $18.5 million, or 8% annualized, compared to the sequential quarter.

However, this is strategic, as the company is focused on higher-yielding commercial loans. Consumer loans increased $3.9 million, or 16% annualized, driven by new home equity line originations. Deposits also held firm from the sequential quarter at $3.1 billion.

Return metrics

In terms of return metrics, Bar Harbor Bankshares performs well. The return on assets has shown significant improvement over the last 3 quarters. The return on assets came in at 1.03% while the return on equity also hit 9.46%. This was weaker than a year ago, but has improved in the last 2 reports. The efficiency ratio remains weaker than in the past at 62.96%, but this is still a respectable figure.

One item to watch on asset quality is the non-performing asset ratio, which decreased to 0.16% from 0.27% a year ago, which is positive. Charged-off loans were $106 million, the lowest in three quarters, while the provision for credit losses was a paltry $0.58 million.

Final thoughts

We are neutral at these levels on Bar Harbor. Overall, the bank is performing well and still offers solid income and a dividend that continues to grow. The bank’s asset quality is strong, loans are growing, and deposits are holding up. While we would like to see better margins, we are encouraged that commercial activity is picking up, which is bringing in higher-yield loans.

Read the full article here