For anyone following Crescent Energy (NYSE:CRGY) since it has gone public, there was a time when the company made acquisitions in several areas. But it now appears that the Eagle Ford will be a core area, and it’s likely to become “the” core area. The acquisition of SilverBow (SBOW) resources was completed to enlarge the operations of the company in the Eagle Ford in a big way. The last article mentioned the bargain price of the Silver Bow acquisition. The means the location cost of future wells is likely to be cheap. That “cheapness” shows as above-average profitability (or return on equity).

It makes sense to serve as a rollup strategy for a lot of smaller operators in this area because often times the Eagle Ford outperforms the Permian when takeaway issues have meant that the Permian operators dealt with pricing discounts and expensive transportation to underperform expectations. Meanwhile, the Eagle Ford production was getting a premium at the same time.

Now, the future is hard to tell for an issue like that. But there’s still a whole lot of interest in the Permian. That’s what led to a takeaway capacity shortage the last few business cycles. So, let us see what happens in the future.

Post Combination Outlook

The standalone company was making some darn good progress with the acquisitions already made. A fair amount of that came from the Eagle Ford. Some of that should provide for an accelerated optimization process for the Silver Bow acquisition.

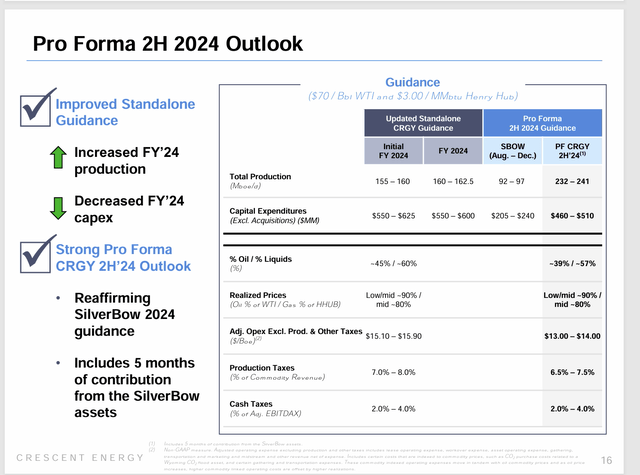

Crescent Energy Operational Improvements Effect On SilverBow Combination Guidance (Crescent Energy Earnings Conference Call Slides Second Quarter 2024)

During the conference call, it was mentioned that the production guidance for the standalone company was raised for the second time while (for the second time) using less capital to get there. Some of that will not have to be learned a second time with the SilverBow acquisition because the acquisition is largely “bolt-on”. Management is therefore at least somewhat familiar with the acreage and what works, based upon progress made with existing operations so far.

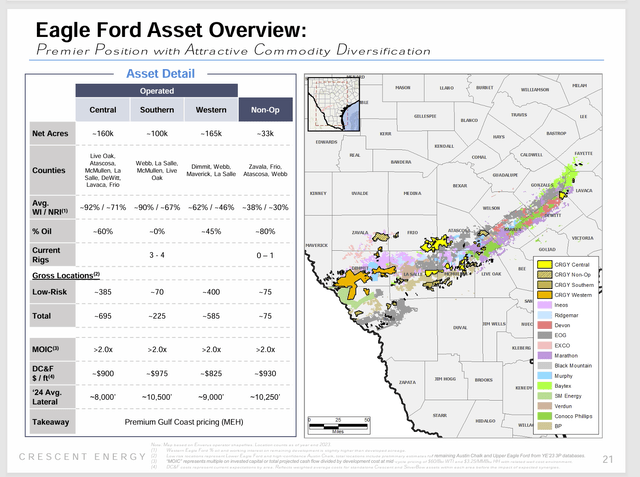

Crescent Energy Post SilverBow Combination Acreage Position (Crescent Energy Second Quarter 2024, Corporate Presentation)

Now the company has by far the largest significant position in the Eagle Ford compared to any other basin acreage. Even more important is that management has tried the Austin Chalk interval and reported during the conference call that the first few wells were encouraging. That’s going to add to the wells shown above as future possibilities. That can be noted as upside potential to at least some of the combinations made in the Eagle Ford.

Earnings

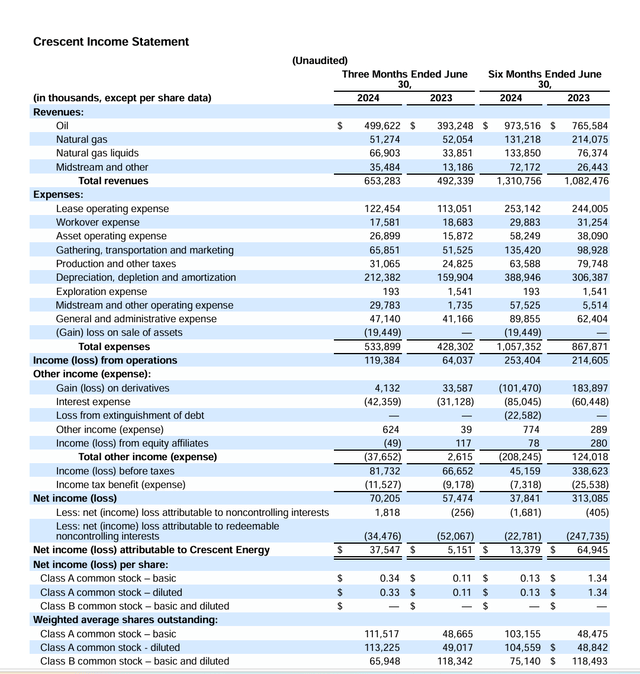

Note that management has the operating income moving forward despite all the acquisition activity.

Crescent Energy Second Quarter 2024, Earnings Summary (Crescent Energy Earnings Press Release Second Quarter 2024)

Clearly, the big swing in earnings for the six-month period is caused by the derivative line. That kind of overwhelms all the improvements that management is talking about.

The other thing to remember is that when management or any company buys operations or acquires the whole company, the immediate results posted are likely to be those of the predecessor organization for a bit. It takes time for optimization activities and new wells to predominate enough to show the results that management claims they are getting.

If there’s constant acquisition activity as there is here, then results may not show what management reports until the company gets large enough that each acquisition does not overwhelm the quarterly reports. SilverBow, for example, is a large acquisition where it will likely take at least six months for any improvements to begin to show on the income statement.

As a result, an evaluation of management is much more important here because the constant influx of acquisition ensure that quarterly comparisons are probably not the best thing to use to figure out progress. There’s simply too many adjustments for an investor to make and not enough information to make them.

Acquisition History

The whole idea of this company was to take advantage of large deals and “add value” to achieve an attractive record so that the company can likely be sold in the future for a decent profit.

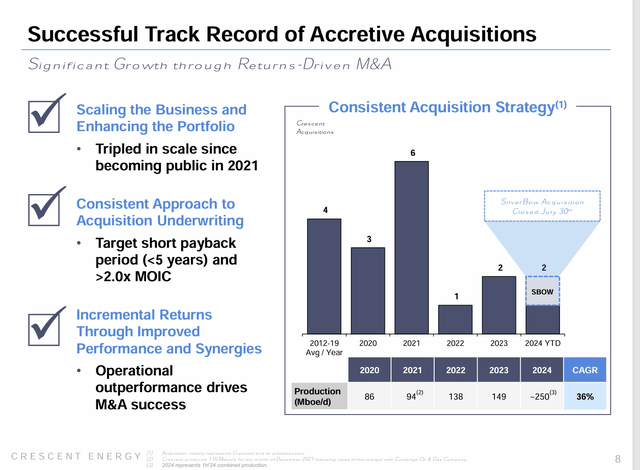

Crescent Energy Acquisition History (Crescent Energy Second Quarter 2024, Earnings Conference Call Slides)

The previous discussion means that the goals management claims to have achieved should become apparent in the near future. Despite the fact that SilverBow is a large acquisition, the operating improvements should begin to show on the income statement as a gradual lowering of the corporate breakeven point. This would be confirmed by increasing profitability a various commodity prices.

So far, Mr. Market has not been impressed. But the latest acquisition will dramatically increase public float. That should lead to more interest in the company. Similarly, if management is getting the improvements claimed, that should likewise begin to show through as the Eagle Ford operations is becoming sizable enough that the improvements should overwhelm any later acquisitions.

The increase in financial strength ratings is a sign from a third party that things are heading in the right direction.

Still, this is an attractive way right now to build an oil and gas company, as there are supposedly far more sellers than buyers. As long as that is the case, then this strategy makes sense.

Summary

Seldom does an investor get to investor alongside KKR in a public investment. Yet, that is the case here. Similarly, John Goff, Chairman of the Board, is another professional with an unrivaled reputation. That helps to assure an investor that the strategy chosen by the company is likely to succeed. Both are very experienced at building and selling companies.

But the early stages of building a company often makes the income statement fairly useless. Too many significant acquisitions prevent a useful comparison. There’s an additional complication here in that one class of shares converts to the publicly traded shares from time to time to change the income allocation between the two classes.

Therefore, there’s a fair amount of dependence upon the management report. It may stay that way for another year or so. At that point, the company should be large enough that the reported operational improvements should begin to show while the acquisitions begin to decrease in significance. That should make future quarterly comparisons more relevant.

Nonetheless, this remains a strong buy consideration based upon the reputation of both KKR and John Goff for building and profitably selling companies. The debt ratio is low, and the financial strength is climbing since the company went public. Now what’s needed is for the benefits of these acquisitions to become apparent enough to the market that the stock begins to appreciate. I like the chances of that happening.

Risks

Any upstream play has the risk of exposure to the volatility and low visibility of future commodity prices.

The KKR organization has the resources to minimize the loss of key personnel. Therefore, the risk of loss of services of a key person is reduced because KKR has a “deep bench” and therefore likely would be able to replace key personnel.

The company has a nontraditional setup with two classes of common stock. There has been a steady increase in the amount of stock available to trade as the conversion of one class of stock into the publicly traded stock continues since the company went public. The acquisition of SilverBow was accompanied by a large increase in the amount of publicly-traded stock. This may decrease the effect of the remaining stock that will eventually convert to publicly traded stock.

Read the full article here