Introduction

Shares of Dine Brands Global (NYSE:DIN) have fallen 16% YTD. Despite the fact that the company’s share price is currently under pressure, I believe that investors have an attractive entry point for opening long positions.

Investment thesis

I believe that lower inflation in the second half of 2023 could lead to more traffic in the US market (the company’s main market), while the company’s average check remains stable, although I admit that we may see higher product prices in the following quarters. In addition, I like the company’s strategy to reduce the number of own restaurants and focus on franchisee income, as this helps to restore profitability and reduce some of the risks.

Company overview

Dine Brands is a restaurant franchisor under the Applebee’s (1,674 restaurants), International House of Pancakes (IHOP) (1,803 restaurants) and Fuzzy’s (137 restaurants) brands. In addition, the company receives income from rental and financial operations. The company primarily operates in the US market.

2Q 2023 Earnings Review

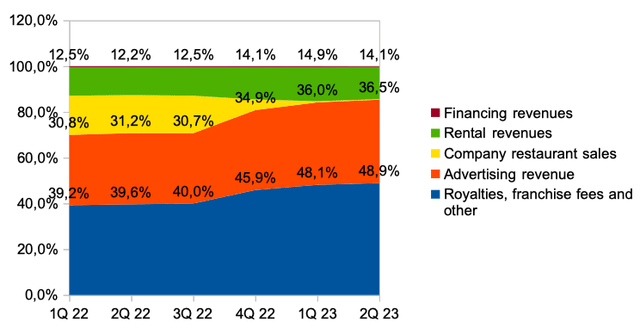

The company’s revenue decreased by 12.4% YoY. The largest contribution to revenue growth was made by the “Royalties, franchise fees and other” and “advertising” segments, where revenue increased by 8.3% YoY and 2.5% YoY, respectively, while in the “Company restaurant sales” segment, the company’s revenue decreased by 98.8% YoY. I would like to emphasize that the decrease in revenue in the Company restaurant sales segment is due to the sale of 69 restaurants under the Applebee’s brand. A slight slowdown in revenue is due to a slowdown in traffic in the chain’s restaurants, while the average bill remains stable. You can see the details of the revenue mix change in the chart below.

Revenue mix (Company’s information)

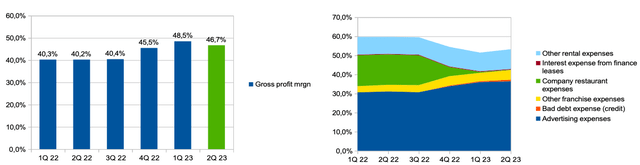

Gross profit margin increased from 40.2% in Q2 2022 to 46.7% in Q2 2023 due to cost reductions associated with operating own restaurants. You can see the details in the chart below.

Gross profit margin & cost of revenue mix (% of revenue) (Company’s information)

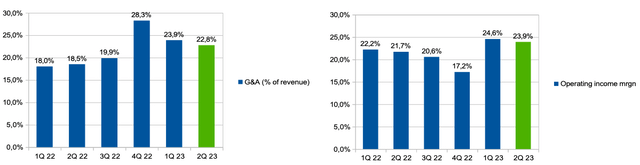

G&A spending (% of revenue) increased from 18.5% in Q2 2022 to 22.8% in Q2 2023 due to one-time expenses related to IHOP-branded restaurants. Thus, the operating margin increased from 21.7% in Q2 2022 to 23.9% in Q2 2023.

G&A expenses & op. income (Company’s information)

My expectations

I believe that in the coming quarters we may see both revenue growth and an improvement in the profitability of the business. First, I think that lower inflation in the second half of the year will support real consumer incomes, which may help restore traffic in the restaurants of the chain and, accordingly, the pace of revenue growth in restaurants. In addition, lower inflation could lead to lower raw materials costs, which could also boost restaurant margins.

Secondly, I believe that at the moment the company refuses to raise prices at the Applebee’s restaurant due to pressure on traffic during the 2nd quarter, however, management admits this possibility if they see the stabilization of traffic trends in the stores of the network. My assumptions are confirmed by management comments during the Earnings Call following the release of Q2 2023 results.

And when I look back at 2022 and in the first two quarters of this year’s, our franchisees, in terms of pricing, they’ve been very modest, especially relative to the category to mitigate the traffic pressure and while at the same time protecting and recovering their margins. So they’ve been very prudent. And as inflation moderates, right as we expect some favorability in our basket in the balance of the year as disposable income improves and then it improves, we’re going to – you’ll find that we’ll be very well positioned to capture more share.

Drivers

Revenue: growth in the average bill due to the addition of new menu items (Benedict sweet and savory crepes), investment in marketing and virtual brands (IHOP branded coffee at grocery and retailers), traffic recovery, restaurant redesign and entry into new markets (Central America, Latin America) can contribute to the growth of business revenue.

Margin: reducing operating costs for raw materials, as well as increasing operational efficiency due to increased sales per 1 square meter, can help improve business profitability.

Risks

Margin: an increase in payroll and raw materials costs due to higher inflation, as well as an increase in marketing costs due to increased competition, can have a negative impact on the operating profitability of a business.

Valuation

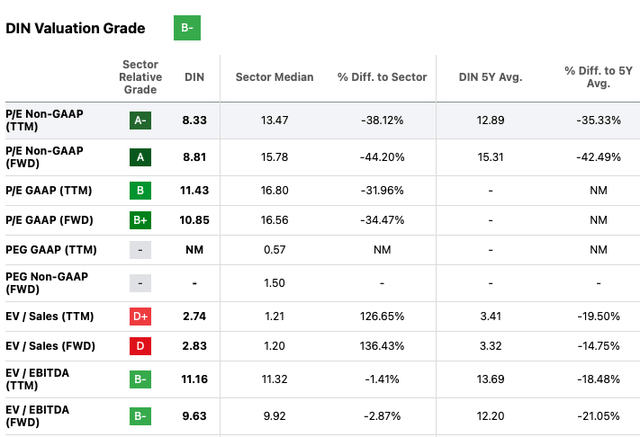

The current Valuation Grade is B-. Under P/E (FWD) and EV/EBITDA (FWD) multiples, the company trades at 8.8x and 9.6x, respectively, implying a discount to the sector median of around 44% and 3%, respectively. In addition, the multiples are still lower than the 5-year averages. I believe that the current level of valuation is favorable for a long-term investor.

Valuation (SA)

Conclusion

Thus, my recommendation is Buy. I predict that the recovery in traffic and the potential for higher prices could have a positive impact on the financials. In addition, I like the current level of valuation in accordance with the multiples, confirmation of guidance on the opening of restaurants under the IHOP brand, innovations in the menu and renewal of restaurants.

Read the full article here