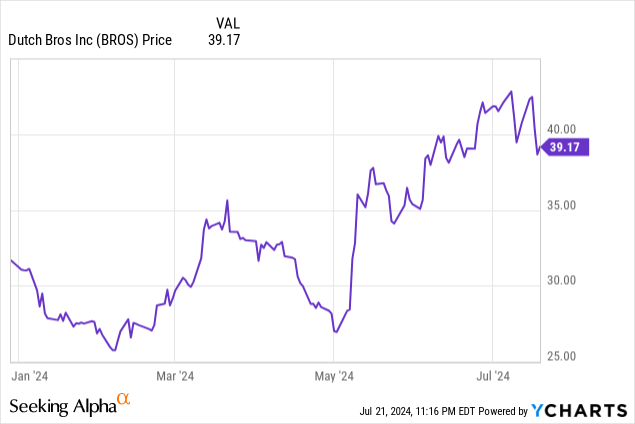

I’ll confess that I’ve been to a few Dutch Bros (NYSE:BROS) locations and have not loved its coffee (then again, I do tend to be partial to local roasters), but its stock is a different story. While Starbucks (SBUX) has missed out on the year-to-date rally and declined double digits this year owing to declining order counts and weakness particularly in China, Dutch Bros has thrived. The U.S.-based chain, which is headquartered in Oregon and has the deepest presence on the West Coast, has seen its share price soar more than 25% this year, edging out and beating the S&P 500.

Buoyed by its recent success, I’m initiating Dutch Bros at a buy rating. The core tenets of my bull case for this stock are:

- Dutch Bros is achieving tremendous same-store sales growth. Put aside the company’s aggressive location expansion, and we still get tremendous sales growth out of the company’s existing fleet of stores, as AUV (average unit volume) has continued to grow over time.

- Achieving significant margin leverage. The company is starting to mint healthy levels of adjusted EBITDA as more locations in its system mature and contribute positive profits.

- Though not a value stock, Dutch Bros can be considered cheap relative to peers in the restaurant space, especially when we consider its superior growth potential.

We note that with just over 800 locations in the U.S. versus Starbucks’ ~38,000 globally (~18,000 in North America), Dutch Bros still has plenty of headroom to expand its popular footprint. We note as well that Dutch Bros’ format, which emphasizes smaller locations (sometimes with just a drive-in counter), may be helping the company to distinguish itself versus its much larger rival in Starbucks, which in recent years has invested heavily in more complex store formats and building out its core “Reserve” cafes.

As the market has continued to climb and hover near all-time highs powered by tech stocks, I’m shifting more of my portfolio out of names that have already benefited from this year’s AI surge and into growth stocks from other industries. In my view, Dutch Bros is an excellent choice.

Fierce same-store sales growth

For investors who are newer to the restaurant and retail industries, same store sales growth is a measure of revenue growth that excludes the impact of new locations that didn’t exist in the prior-year comparison. This is a great measure for how the brand is doing, without factoring in the lumpiness of store openings and available capital to invest in new locations.

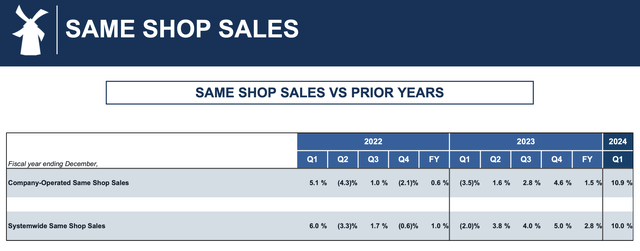

Dutch Bros’ same-store sales growth not only outstrips many of its peers in the restaurant industry, but it has also been consistently accelerating.

The chart below shows Dutch Bros’ sales growth trends:

Dutch Bros same-store sales growth (Dutch Bros Q1 earnings deck)

As shown above, in Dutch Bros’ most recent (March) quarter, same-store sales for the company’s company-operated stores were 10.9% y/y, accelerating more than double versus a 4.6% growth rate in Q4. In fact, growth has been accelerating each quarter since Q1 of 2023.

Note that roughly two-thirds of the company’s systemwide stores are company-owned, while the rest are franchised. Systemwide performance in Q1 was similar (only 90bps weaker) to company-operated stores, though systemwide outperformed company-operated by 130bps for the entirety of 2023.

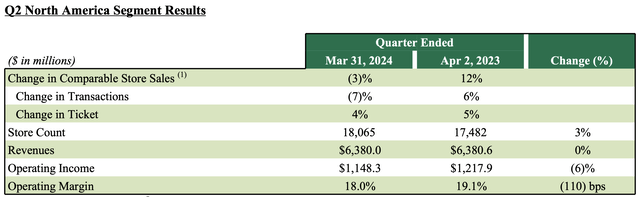

We note that Dutch Bros’ same store sales growth trounces that of Starbucks. The most relevant comp is to Starbucks’ North American division; which, as shown below, saw a -3% y/y decline in same-store sales in Q1. If it weren’t for a 4% increase in ticket pricing (due to Starbucks’ own price increases as well as customer order mix), same-store sales growth would have been even worse, with transaction volumes falling -7% y/y.

Starbucks North America results (Starbucks Q1 earnings release)

From this, it’s clear that Dutch Bros is gaining significant market share versus Starbucks on a same-store basis. We note as well that Dutch Bros’ same-store sales growth shows quite well versus other restaurant comparisons in the same time period. Chipotle (CMG), one of the largest fast-casual restaurant chains, reported 7% y/y same-store sales growth in Q1; Sweetgreen (SG), the salad chain, reported 5% growth, and CAVA (CAVA), the Mediterranean chain that went public recently, showed only 2% y/y growth.

Achieving significant operating leverage

Dutch Bros’ strength lies not just in growth, but in fantastic growth and operating leverage at scale.

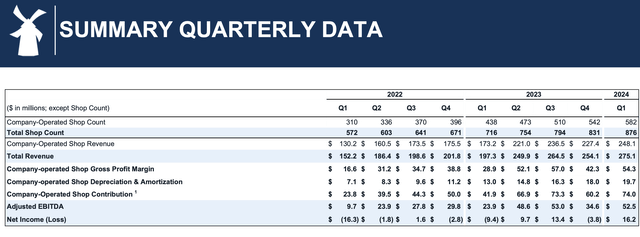

We note that the company has just started to pump out meaningful adjusted EBITDA profits. Adjusted EBITDA in Q1 grew more than 2x y/y to $52.5 million, representing a healthy 19% margin. Note that of the company’s current revenue profile, about 90% of revenue comes directly from company-owned store transactions, while the remaining 10% accrues from franchising fees.

Dutch Bros store count and EBITDA progression (Dutch Bros Q1 earnings deck)

Dutch Bros significantly expanded its store fleet last year, growing from 671 locations at the end of 2022 to 831 at the end of 2023 (a 24% increase). In Q1 alone, the company opened 45 net-new stores, of which 40 were company-owned.

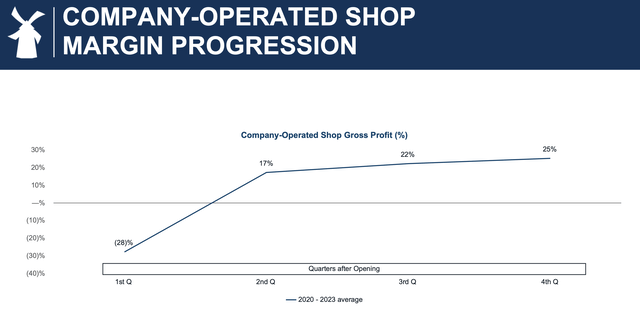

The key point here is that it takes time for each individual location to hit profitability. The chart below shows that in the first quarter of a company-owned store’s existence, it typically generates a negative gross margin, but levers to significant profitability by its fourth quarter of life.

Dutch Bros store profitability progression (Dutch Bros Q1 earnings deck)

This is a positive upward catalyst, as the company has 146 net-new openings in 2023 that will “fully mature” in 2024.

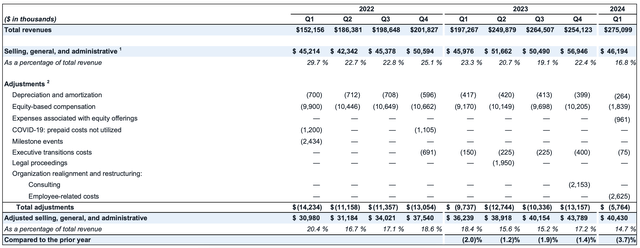

As store count and average store tenure has grown, the company’s overall SG&A costs and corporate overhead have shrunk as a percentage of revenue. Adjusted for depreciation and stock comp, we note in the chart below that adjusted SG&A costs dropped to a record low of 14.7% of revenue, 370bps lower than 18.4% in the year-ago quarter.

Dutch Bros SG&A leverage over time (Dutch Bros Q1 earnings deck)

Valuation, risks, and key takeaways

At current share prices just under $40, Dutch Bros trades at a market cap of $6.02 billion. After we net off the $262.7 million of cash and $233.6 million of debt on the company’s most recent balance sheet, its resulting enterprise value is $5.52 billion.

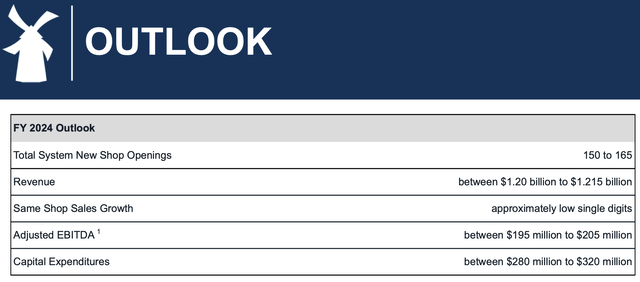

Dutch Bros outlook (Dutch Bros Q1 earnings deck)

This year, as shown above, the company is planning for significant expansion, with a range of 150-165 net-new store openings (versus 160 in 2023) and $1.20-$1.215 billion in systemwide revenue, representing 24-26% y/y growth. We note that this revenue estimate also leans on “low single digit” same-store sales growth, which may be conservative if the company exited Q1 at a 10% y/y growth rate.

Dutch Bros’ valuation multiples currently sit at:

- 4.6x EV/FY24 revenue, or 3.2x on a FTM (forward twelve-month) basis

- 18.4x EV/FY24 adjusted EBITDA

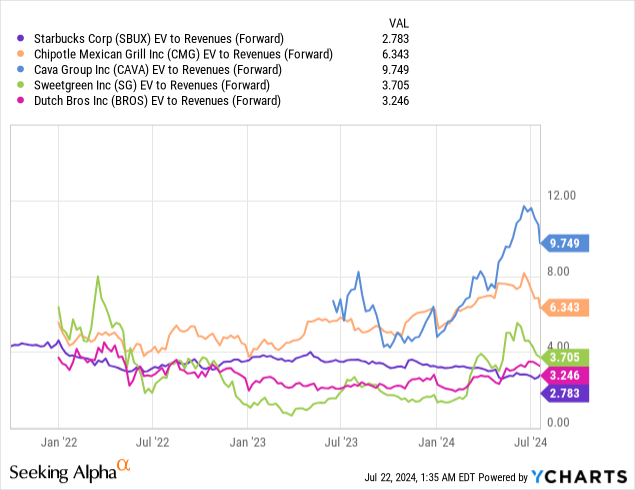

Given the rapid clip at which EBITDA is growing this year owing to large portions of the store portfolio maturing from last year’s openings, I’d prefer to lean on revenue multiples. Dutch Bros’ 3.2x FTM revenue multiple is slightly richer than Starbucks (2.8x), but enjoys a substantial growth premium to its larger rival which is seeing declining same-store sales. Dutch Bros also trades at lower revenue multiples than a basket of growing restaurant stocks:

There are risks to consider, of course. Dutch Bros’ current stronghold is on the West Coast and in Texas; it plans to expand its footprint further, which may A) either cannibalize existing locations if it increases density on the West Coast or B) not have much brand recognition to gain meaningful sales traction on the East Coast. Higher inflation and labor costs may also eat into its margin expansion; the company’s investments into automation have been minimal, unlike salad chain Sweetgreen, which has invested heavily into fully-automated ordering and salad-making robotics.

Still, given strong same-store sales growth and an appealing revenue multiple, I’d say Dutch Bros still has plenty of room to rally further.

Read the full article here