Investment Thesis

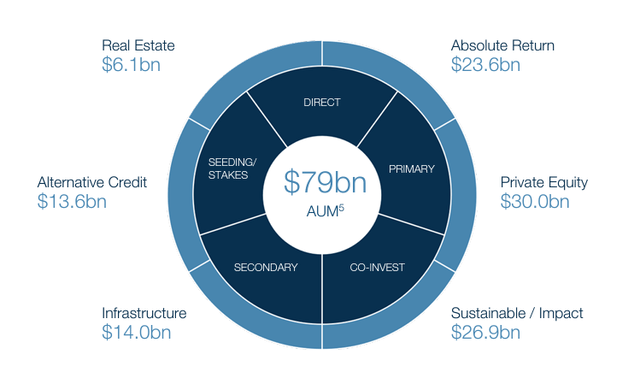

GCM Grosvenor (NASDAQ:GCMG) has seen a solid share price performance over the past YTD, up 20% at the time of writing. The company has seen positive developments such as raising new capital of $1.6 billion, increasing adjusted net income by 39% over last quarter, and significant growth in AUM to $79 billion as of March 31, 2024. Growing momentum in these fundamental metrics signal an improvement to the business, but the share price has already priced in many of these positives in my opinion. Furthermore, potential dilution from partnership units and other dilutive securities make this security potentially overvalued. In conclusion, I exercise caution to shareholders and rate this stock a hold.

Company Overview

GCM Grosvenor is an alternative asset manager that invests “across all major alternative investment strategies and are highly flexible in how we structure our solutions to meet each client’s specific needs” according to the annual report. With around $79 billion in AUM, the company has had a strong track record of delivering value to their clients in the form of competitive risk-adjusted returns.

Their clients consist of “large, sophisticated, global institutional investors and a growing individual investor client base”. They manage client money in customized separate accounts and properly take into account investment objectives to create satisfactory returns. Investments are made both in the private and public space, through absolute return funds, alternative investments, and real estate.

Q1 Earnings Presentation

I like how the company is quite flexible and diversified in terms of their investment strategies. This should make them pretty resilient to sector downturns as they have enough diversification to reduce the volatility of investment performance. Also, their combined experience in middle market, alternative credit, and infrastructure can allow management to see certain market trends to create more value for their clients.

The company collects management fees as a primary source of revenue for their services. These management fees and incentive fees are determined based on performance and assets under management. FPAUM, otherwise known as Fee-Paying AUM, “is a metric we use to measure the assets from which we earn management fees”. Investors should note this is where most of the money comes from, and that AUM plays a big role in how much revenue this company makes.

Overall, I believe the company is quite strong, but the share price already reflects these positive characteristics. The company is well diversified with a strong track record of delivering success to their clients. GCM Grosvenor’s emphasis on sustainable investments have evidently attracted and retained clients as many of our institutions have ESG mandates they must follow. Going forward, I expect the company to continue to do well and keep their AUMs growing, enhancing their reputation and value for both clients and shareholders alike.

Betting Big On Private Markets

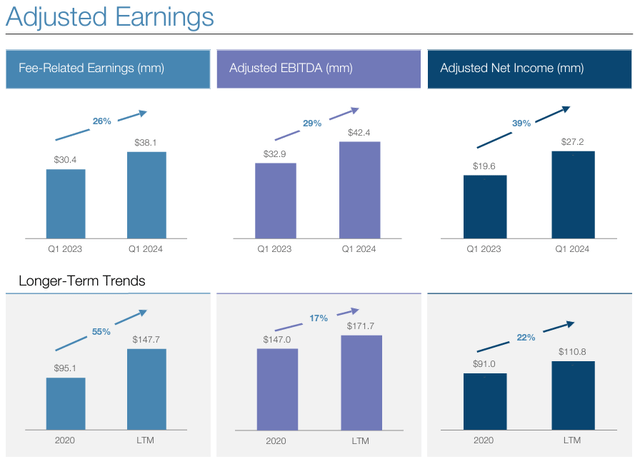

The company reported first quarter 2024 earnings on May 7, 2024 with the following results:

- First quarter 2024 GAAP Net Income attributable to GCM Grosvenor Inc. was $2.1 million

- First quarter Fee-Related Earnings increased 26% over prior year QTD

- First quarter Adjusted Net Income increased 39% over prior year QTD

Investors can see the first quarter earnings were pretty strong, with solid earnings growth that demonstrates management’s ability to deliver solid return while raising new capital to pursue investment opportunities. GAAP revenues increased 10% YoY compared to Q1 2023 sales, with adjusted EBITDA up 29% YoY as well. This positive growth shows me that alternative asset managers have benefited from an increased client interest in private credit and private equity investment solutions.

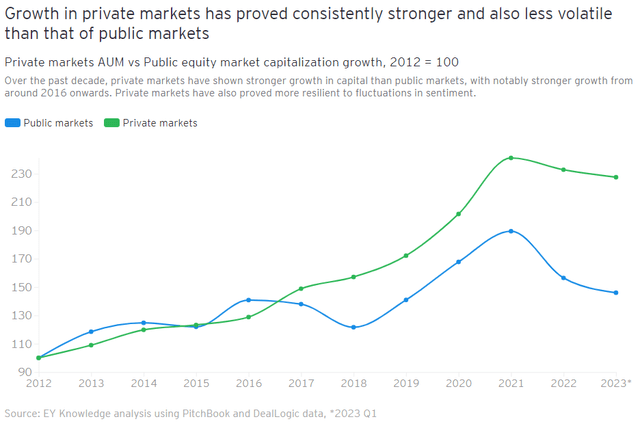

According to EY, “Private capital has shown great resilience in a volatile environment and presents tremendous opportunities for investors and entrepreneurs globally”. The report continues to show optimism for private investment opportunities as many companies choose to stay private to avoid the cost, headaches, and intense spotlight in the public markets. Therefore, I believe that alternative, private investment managers such as GCM Grosvenor are benefitting from this trend and are leaning more towards the private markets.

EY

The earnings transcript confirms this story on the emphasis and importance of private markets driving AUM and revenues,

Private markets continues to be a key growth driver, with private markets fee-paying AUM growing 7% year-over-year. As of quarter end our private markets business represents 70% of total AUM and 65% of our fee-paying AUM.

In conclusion, the story continues to show positive momentum as GCM Grosvenor leans more into investments in the private markets. This attractive area can provide more value to clients, as most of them are looking for resilient risk-adjusted returns in today’s economy. Most of their client base are pensions, so they are likely looking for stable, secure, and relatively low-risk solutions that fit well with what GCM Grosvenor is offering. Therefore, I expect more money to flow in the private markets which should increase both the AUM and management fees Grosvenor earns in this area.

Client Retention Should Remain Strong

GCM Grosvenor has a track record of solid client retention, around 90% average re-up rate on initial sale according to their Q1 earnings investor presentation. They use separately managed customized accounts to offer flexible and targeted investment solutions that fit the investment objectives of each unique client.

According to their annual report, “Our 25 largest clients by AUM have been with us for an average of approximately 14 years, and our existing clients are a key driver of our asset growth”. It looks like they get a lot of money from existing clients, having earned their trust through a successful track record of providing good returns.

Both the clients and money have demonstrated to be sticky, as many private and alternative investments require clients to lock up the money for a certain period of time. Because private investments are by nature illiquid, the revenues and management fees that GCM Grosvenor earns are recurring. For example, the long-term trend of adjusted net income has shown steady growth, up 22% since 2020.

Q1 Earnings Presentation

I expect the clients to continue to stay and remain committed to being long-term partners of GCM Grosvenor. Given the $1.6 billion in new capital fundraising, it is evident to me that their investment strategies and returns have been attractive to existing clients. Many of their private equity returns have beaten the S&P 500, demonstrating their skill and diligence in finding good deals. (Please note: past performance is no guarantee of future performance)

10-K

Any investment manager that can make 21.9% annualized returns since inception is likely to keep their clients in my view. The bottom line here is that client retention should continue to remain very strong, leading to steady growth in AUM and adjusted earnings for shareholders to reap.

Valuation – $6 Fair Value

To value this company, I will be using their adjusted earnings numbers as they better represent the true profitability of the company in my opinion. This is because adjusted net income does not take into account the noise that comes from net income/loss attributable to noncontrolling interests in GCMH and other partnership interest-based compensation.

In FY 2023 the company reported adjusted net income of $103.2 million. I believe $100 million is a good floor to project for adjusted net income going forward because the clients and AUMs all seem very sticky. Furthermore, the company reported adjusted net income of $27.2 million in Q1 2024. If we assume this quarterly rate to continue for FY 2024, then adjusted net income should total $100 million for FY 2024.

Divide $100 million by diluted shares outstanding of 187 million gets me $0.50 diluted EPS, rounded down. Apply a sector median FWD earnings multiple of 11.67x gets me around $6 fair value, rounded up. Investors can see that because of the potential dilution of shares outstanding from dilutive securities, the company can be seen as potentially overvalued.

Seeking Alpha

While the company is fantastic with excellent economics, the main concern I have is the steady increase in diluted shares outstanding. The company has a lot of ‘partnership units’ that if exchanged could dilute shareholders. Therefore, I exercise caution to shareholders because of potential excessive dilution that could reduce shareholder value.

Risks

As said before, the company has a lot of partnership units that if exercised would increase shares outstanding by 144,235,246, leading to a potential dilution of over 300%. Adjusted Net Income Per Share – Diluted is therefore much lower than investors would like, last reported at $0.55 for the FY 2023. The market doesn’t seem to have priced this risk in, leading me to exercise caution to shareholders today.

Past performance is no guarantee of future performance. Although GCM Grosvenor has had a marvelous past, if future headwinds show up in the alternative investment management space, the company could lose clients and AUM due to bad performance. Economic slowdowns and recessions could make the environment difficult to find high IRR opportunities.

Competition in this space is growing, as many private equity and alternative investments become more popular. As the market gets more crowded, past performance may be inflated as it becomes harder to find uncovered opportunities. Because capital tends to flow towards high IRR, eventually high IRR becomes mediocre IRR assuming perfect competition and information amongst competitors.

Hold GCM Grosvenor

Despite the optical overvaluation, the stock is a hold to me because as long as the market isn’t concerned about this potential dilution, then the shares should perform in-line with the sector at large. I’m not giving it a ‘sell’ because I think the fundamental strengths and clients GCM Grosvenor have are very impressive. Even without potential dilution, the stock trades at 15x FWD earnings, which is no longer cheap in my view. So, in any case I think the stock is not a buy and thus deserves a hold rating.

Read the full article here