I last wrote about the Simplify Enhanced Income ETF (NYSEARCA:HIGH), which focuses on T-bills with some options trading, in late 2023. In that article, I argued that HIGH’s strong 9.3% distribution yield, low volatility and drawdowns, made the fund a buy.

Since then, HIGH’s distributions are slightly down, while its returns increased. Share prices were generally quite stable, not a small feat for a fund yielding 9.3% focusing on safe assets, until the June dividend payment. Still, developments seem broadly favorable to the fund and its shareholders. HIGH remains a comparatively safe, high-yield ETF, and so the fund remains a buy.

HIGH – Quick Overview

A quick look at HIGH before analyzing some of its more recent developments.

HIGH invests most of its portfolio in simple T-bills. At current yields, these generate a significant amount of income for the fund. Federal Reserve cuts should start to pressure this source of income in the coming months.

HIGH also trades option spreads, generally on equities. Specifics vary, but most option spreads are structured so as to generate a modest amount of premiums / income at low risk.

The overall performance of these spreads is strongly dependent on their specifics, and of general management competence. Selecting the right options should generate a nice amount of income without significant increases to risk, volatility, or drawdowns. Picking the wrong ones should simply decrease returns, risk, volatility. and drawdowns. Risk management also matters: spreads must be carefully tailored to minimize risk.

The issues above matter for HIGH, unlike for many income investments or ETFs. Investors in T-bills do not have to pick the right T-bills to generate income, nor must they carefully construct their portfolios to minimize risk. Investors in T-bills simply receive around 5.25% in income per year. Investors in individual high-yield bonds could definitely boost their returns through smart bond selection, but they could also just buy an index ETF.

HIGH’s strategy has worked overall, with the fund outperforming T-bills since inception, by reasonably good margins. Drawdowns and volatility both seem quite low, although it took the fund a couple of months to find its bearings.

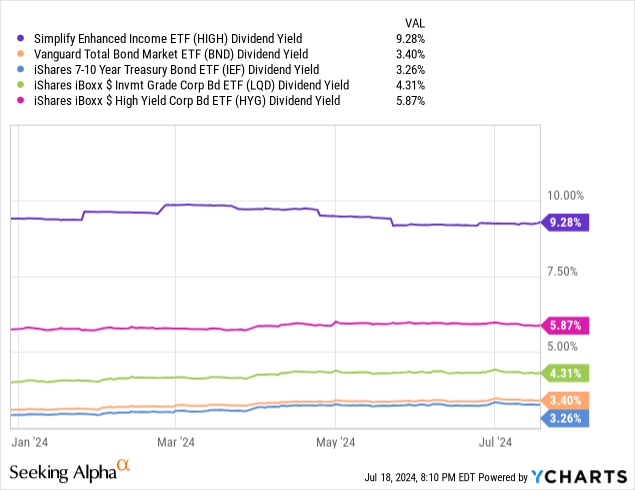

HIGH yields 9.3%, an incredibly strong yield on an absolute basis, and much higher than most bonds and bond sub-asset classes.

HIGH’s distributions are not fully covered by underlying generation of income or premiums. T-bills currently yield around 5.25%, and option spreads could not plausibly generate 4.00% in premiums every year. At least not the low-risk spreads that HIGH trades, especially so consistently. HIGH’s share price has steadily decreased since inception, consistent

HIGH’s distributions will only turn more unsustainable as the Federal Reserve cuts rates later in the year. It is my understanding that regulations almost compel HIGH into having somewhat unsustainable distributions. In most cases, ETFs must distribute any profits from options or derivatives to shareholders. So, if these are profitable, gains are distributed, and share prices remain stable. If these are unprofitable, share prices go down. Under these conditions, share prices can only go down long-term, although perhaps only very slowly.

Moving on, HIGH yields 9.3%, but only seems to generate around 7.0% – 8.0% in income every year.

High – Recent Developments

Lower Distributions

HIGH’s distributions were steady at $0.20 per month for close to a year, from early 2022 to early 2023. Distributions decreased from March to May but have since returned to $0.20. Distributions are down 5.2% for the entire year, compared to 2023.

HIGH’s distributions could have been cut for several reasons, including aligning these with the fund’s income, lower realized profits from its option trades, and other vagaries of ETF distribution requirements. It is my understanding that for funds with significant option investments, distributions are not necessarily reflective of underlying generation of income, so distribution cuts are not necessarily a negative.

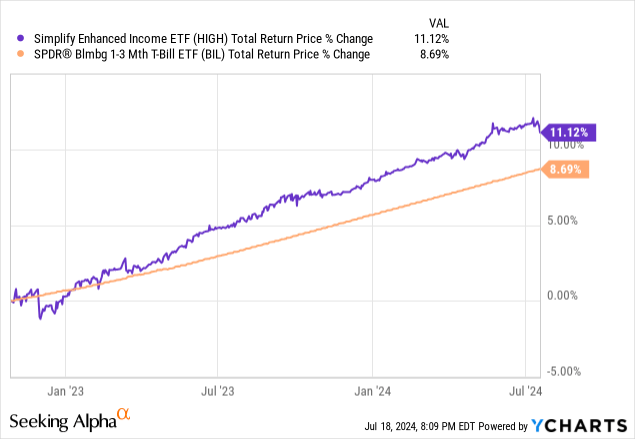

Higher Returns

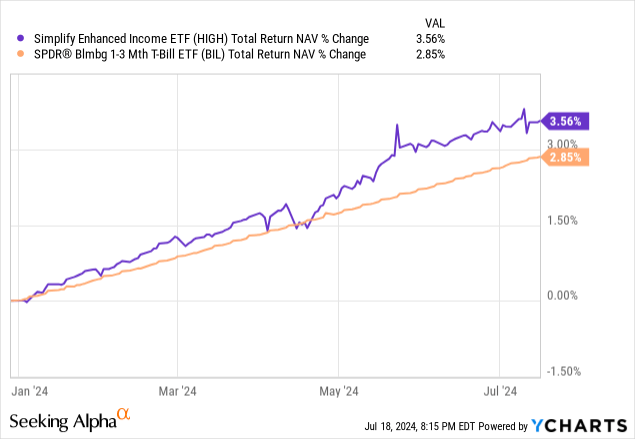

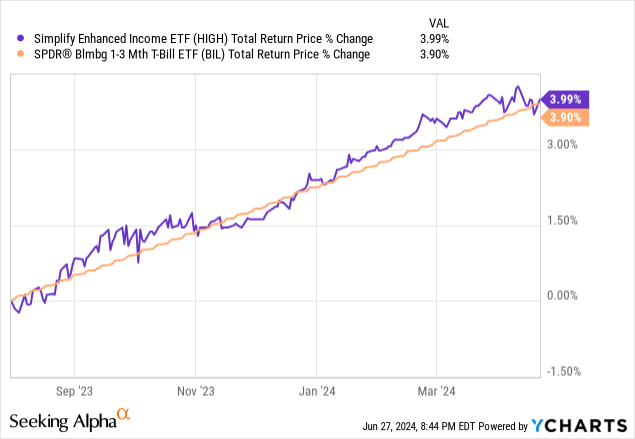

HIGH’s total returns have been reasonably good these past few months, with the fund outperforming T-bills YTD. Outperformance mostly occurred in May and June, with the fund mostly matching T-bills before.

Recent outperformance contrasts with prior performance. HIGH had matched the performance of T-bills from early August 2023 to late April 2024, a period of around 9 months.

Data by YCharts

HIGH’s option spreads were generating meager returns for 9 months. Although that is not a terribly long amount of time, most of the fund’s option spreads last for less than a month, so it is an awful lot of (mostly) unsuccessful trades. I think some investors had started to waver on the fund before, but the last few months should probably put any concerns to rest: HIGH’s strategy continues to work reasonably well.

As an aside, I think a cycle of outperformance and matching the performance of the index is about as good as investors can expect moving forward. Consistent outperformance would require consistent option profits, and few traders are that good, and the few that are don’t manage retail products.

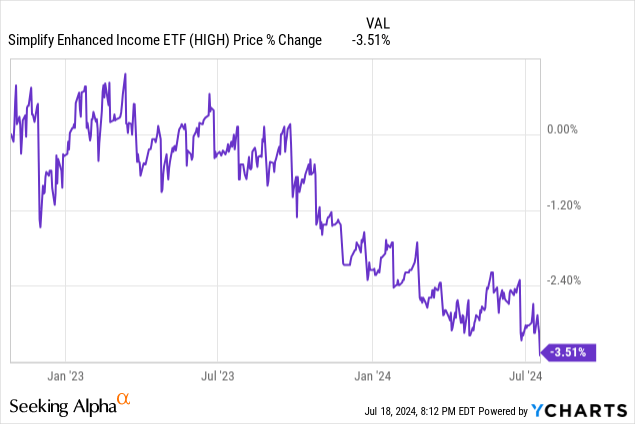

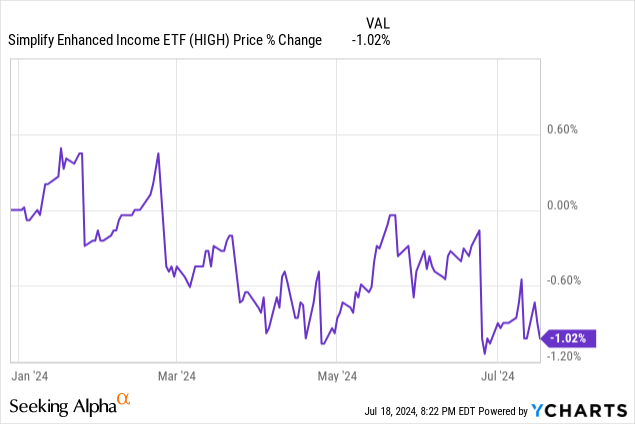

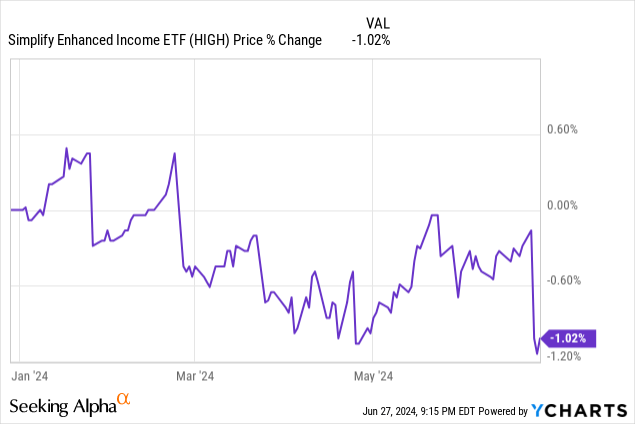

Somewhat Reduced Capital Losses – With a Caveat

The combination of lower distributions and higher returns almost mechanically resulted in somewhat more stable share prices. HIGH’s price was down only 0.30% until late June, a very small drop, and one which might have trended down towards 0.0% with a bit more luck or success.

HIGH then paid a full $0.20 distribution and prices dropped another 0.70%, for 1.0% in total.

Data by YCharts

For HIGH, monthly $0.20 distributions amounts to a 9.9% yield. Such a yield is plainly unsustainable, leading to small, but consistent, capital losses / lower share price, as happened this last June. Prior to June distributions averaged $0.168, amounting to a 8.3% yield. Said yield seemed much more sustainable, leading to much smaller, inconsistent capital losses.

Considering the above, I think yields in the 7.5% – 8.5% range are much more sustainable and healthier for the fund. HIGH must comply with applicable regulations in this area though, and I think these pull towards (somewhat) unsustainable distributions. Right now the fund yields 9.3%, which should result in small, but consistent, capital losses and distribution cuts. Total returns remain more than adequate, however.

Conclusion

HIGH’s strong 9.3% distribution yield and safe, stable, share price make the fund a buy. Income and returns are a tad lower than 9.3%, which should result in small, but consistent, capital losses and distribution cuts moving forward.

Read the full article here