With lithium prices well off their recent highs, many companies across the industry have been the victims of significant value destruction as investors have fled for more stable investments. Lithium Americas (Argentina) (NYSE:LAAC) has been one of the companies most affected by this, shedding over half of its value since separating from Lithium Americas (LAC). This article seeks to examine why the lithium selloff as a whole seems to have been largely overdone, and why LAAC may have the most to gain in a rejuvenated market.

The Lithium Cycle

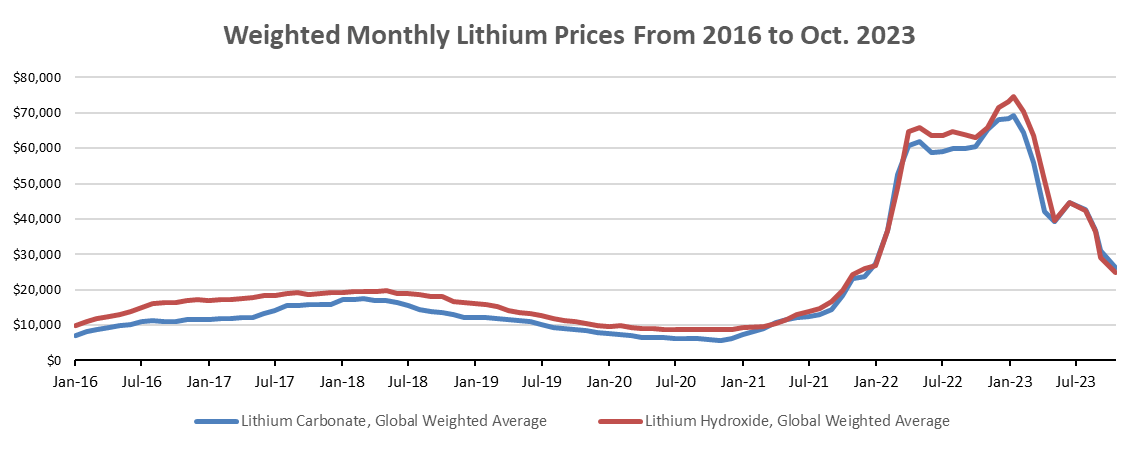

Since December, lithium spot prices have remained relatively stable as carbonate has traded between $12,000/tonne and $16,000/tonne. Now, a 33% variance may not seem like the classic definition of “stability” but, in the lithium industry, that’s what passes as a period of relative market stability.

Benchmark Mineral Intelligence

As noted in the chart above, lithium prices have been quite volatile since 2016, though the 83% drop in prices from 2022 highs is certainly more volatile than the norm. Rather than the normal cycle in 2021, a steep supply shortage caused markets to react aggressively and push lithium prices up 1,300% from 2020 lows. This dramatic swing has kickstarted a new era of price volatility, as market participants are now forced to overreact on either end of the spectrum.

While Fastmarkets originally forecasted a 33,000 tonne supply surplus for the year, slower than expected demand growth could mean that the market is oversupplied by as much as 250,000 tonnes. It’s this extreme imbalance, a 20% oversupply, which has producers and investors alike spooked about the long-term strength of lithium prices.

Back in 2020, we saw something similar as prices fell 67% from over $17,000/tonne in 2018 to below $6,000/tonne (adjusted to 2023 dollars) after supply exceeded demand by 21% (see graphic above). This introduces another critical concept to my analysis – the lithium market is fundamentally stronger than it was just four years ago.

USGS & Author’s Calculations

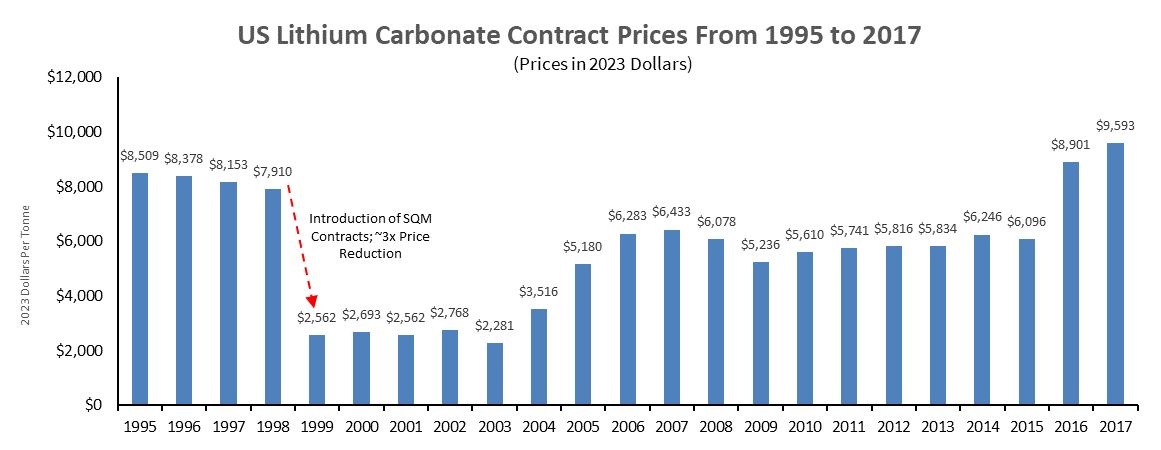

As we can plainly see, prices of ~$6,000/tonne were the long-term norm leading up to 2016, at which point a few Chinese suppliers artificially squeezed the market. So, if market conditions are so similar to 2020, why is the price still more than double?

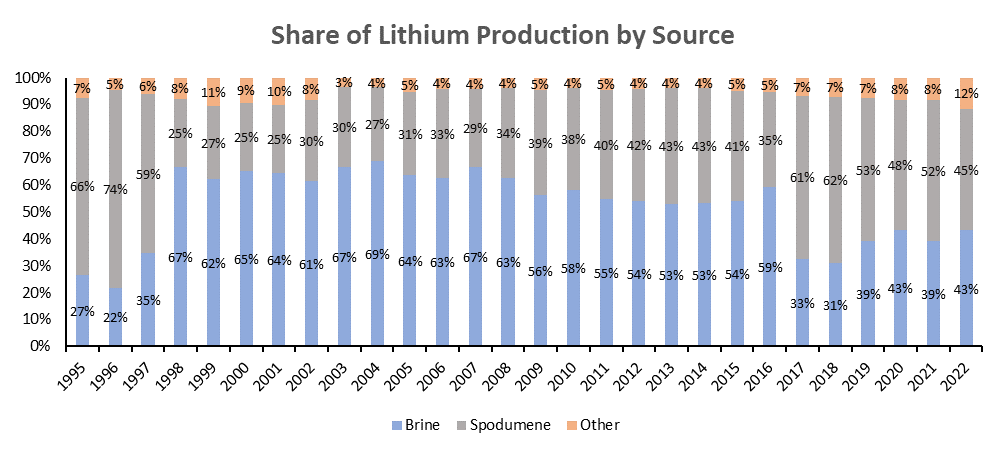

To answer this question, we must first ask another. Why did the commissioning of SQM’s (SQM) first lithium operation have such an incredible impact on global lithium prices? The short answer – production costs. Brine projects, such as those operated by Albemarle (ALB) and SQM in Chile have substantially lower operating costs compared to hard rock pit mines.

When SQM launched its project, it sought to undercut its peers by such a significant amount that customers would be willing to break their long-term contracts in order to switch over to SQM. Almost overnight, eight hard rock projects closed, and only one remained in operation. Brine’s share of the lithium supply shot from 22% in 1996 to 67% by 1998. But fast-forward to today, and brine projects haven’t been able to keep up with demand, opening the door for hard-rock to recapture its dominance with 57% of total lithium supply.

USGS & Author’s Calculations

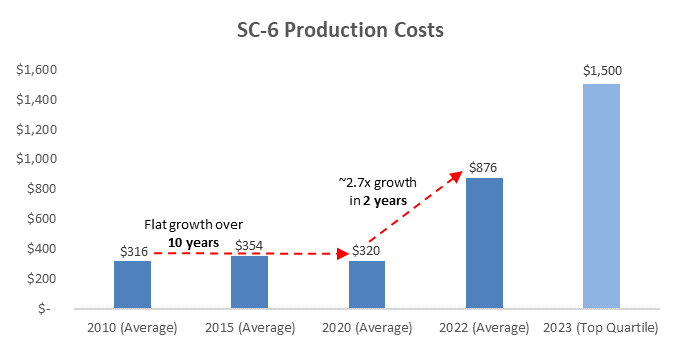

Though, this transition began back in 2017, so this still only answers part of the question. The other half of the equation comes down to the quality of new hard-rock operations. In order to remain even somewhat competitive with brine resources, lithium producers had to be extremely selective in the hard-rock assets they chose to develop as prices slowly crept back up to the long-term average. But this all changed when lithium prices soared above $85,000/tonne.

USGS & Author’s Calculations

6% spodumene concentrate, or SC-6, is the raw material produced from most hard-rock mines and is eventually refined into lithium carbonate or hydroxide. When prices skyrocketed, production costs became secondary to time to market as all lithium projects, regardless of quality, were outrageously profitable.

Hard-rock mines can be commercialized significantly faster than brine operations (as little as 2 years compared to at least 8 for brine), meaning they were the primary tool used to respond to the undersupply created in 2021. Lower quality operations could be commercialized even faster, thus increasing the price floor at which the current market can be sustained. For low-cost operations, i.e. brine, this is great news.

Okay, so we’ve seen this before, but what comes next? Well now investments into lithium projects have ground to a halt, a few mines have been placed in care and maintenance, and prices have pretty much stalled at their new bottom.

Despite the significant oversupply, lithium demand is still expected to grow 34% YoY in 2024 and is on pace for a similar level of growth in 2025. If this materializes, the industry would once again find itself in a shortage and, while $80,000/tonne may be out of reach, $35,000/tonne does seem fairly reasonable given lepidolite production costs.

The extreme volatility of the lithium market often materializes in dramatic cycles where prices, and investments, can swing violently in response to the market supply dynamic. From the second half of 2021 to the first half of 2022, $4.2 billion was spent in M&A activity – a 9x increase from the previous 12-month period, as producers sought to reap the rewards of sky-high lithium prices.

This influx of investment activity in the sector contributed to the present oversupply (given 2-3 year lead times for hard-rock mines), which has now led to a lull in new project investment. By the time this activity resumes, the market will already be back in a shortage and, most likely, another influx of capital will result in a subsequent oversupply after a couple of years. And thus, the cycle continues.

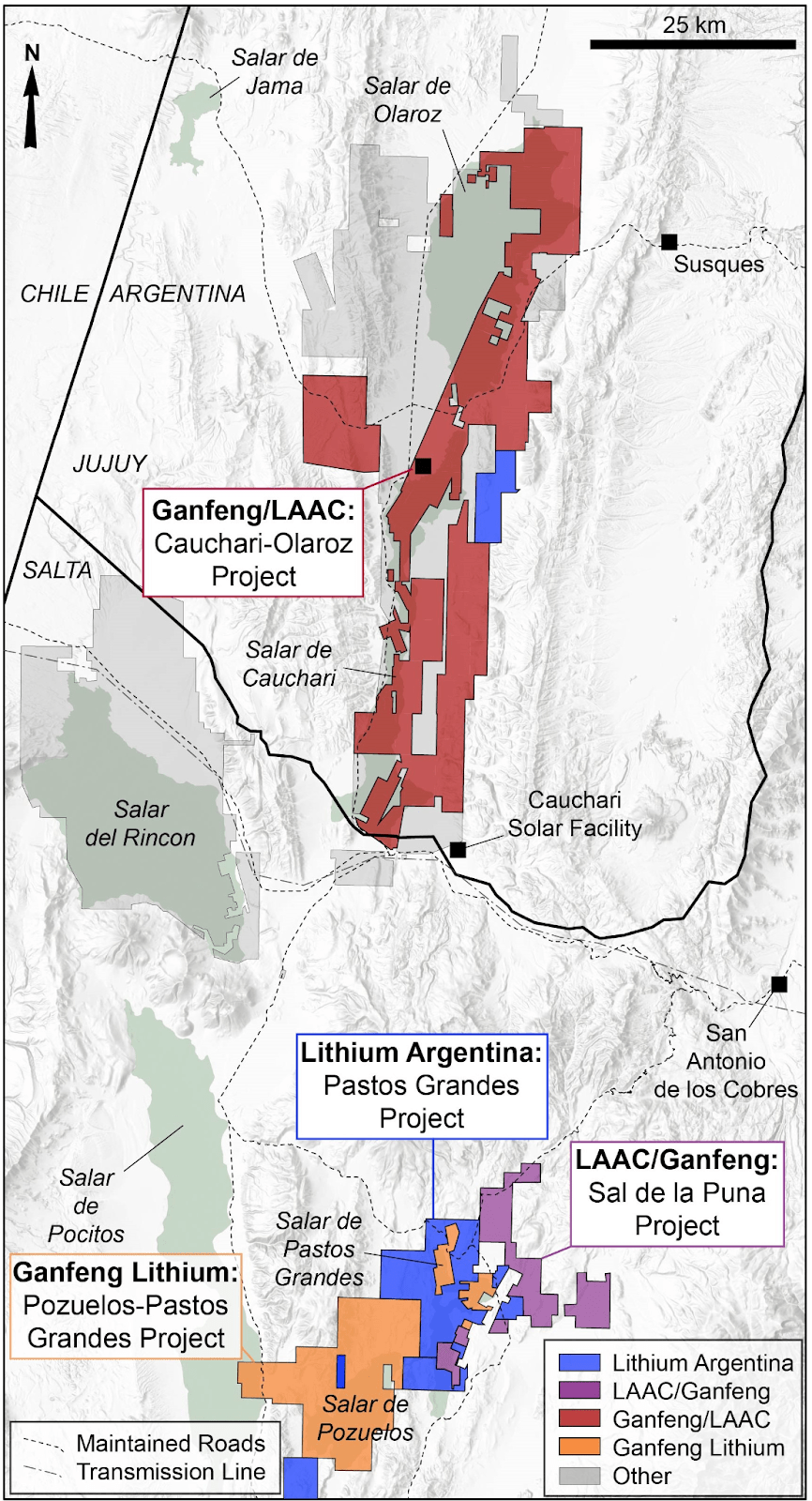

Cauchari-Olaroz

Cauchari-Olaroz is LAAC’s premier asset, where it is currently ramping production of lithium carbonate, hoping to reach 40,000 tonnes per year. According to its DFS, finalized at the end of 2020, operating costs will be $3,579/tonne. For reference, at an average production cost of $876/tonne SC-6, producing lithium carbonate from spodumene now costs an average of $11,000/tonne for an integrated operation (8 tonnes of SC-6 per tonne lithium carbonate / hydroxide + refining costs).

Funny enough, the Cauchari-Olaroz DFS was heavily criticized when it came out for utilizing a sales estimate of $12,000/tonne given prevailing market prices were below $6,000/tonne at the time. Fortunately, this allows us to do some basic valuation work with little price downside after having identified a floor of $12,000/tonne in the post-COVID lithium market.

Utilizing an 8% discount rate and the above estimates, the Cauchari-Olaroz project has a post-tax NPV of $1.957 billion. That means, at current lithium prices and factoring in the company’s 44.8% ownership of the project, Cauchari-Olaroz is worth $877 million to LAAC’s shareholders. Ganfeng Lithium (OTCPK:GNENF), one of the largest lithium producers in the world, owns 46.7% while the local provincial government owns the remaining 8.5%.

Keep in mind, NPV takes into account all phases of the project, including construction (now complete), and is heavily biased toward its earlier years. As such, the NPV at its current stage would be substantially higher than what was originally published in the DFS.

Furthermore, the DFS was published before the company made plans to eventually expand production up to 60,000 tonnes per annum (“tpa”). The expansion was originally planned for three years after initial production at Cauchari-Olaroz, but this has likely been pushed back.

Additional Holdings

In addition to Cauchari-Olaroz, LAAC acquired properties from Millennial Lithium and Arena Minerals in 2022 and 2023 respectively. Ganfeng holds a 35% interest in the property acquired from Arena Minerals, which it held prior to LAAC’s acquisition, and a 15% interest in the property acquired from Millennial Lithium after a recent investment of $70 million.

Lithium Americas Argentina

You may note that Ganfeng also holds its own property within the same basins – the Pastos Grandes and Pozuelos salars. Ganfeng acquired this property from Lithea after LAAC outbid it on Millennial Lithium, though the two companies didn’t compete on the Arena acquisition.

This dynamic is beginning to evolve rather nicely to form something similar to Cauchari-Olaroz – a massive brine operation spanning two salars. Between the two companies, they own almost the entirety of both salars and, as part of Ganfeng’s $70 million investment, the two companies have agreed to finalize a joint regional development plan that covers both salars.

Prior to its acquisition, Millennial Lithium posted a DFS in 2019 where it estimated operating costs of $3,388/tonne and production of 24,000tpa. Arena was much less advanced when LAAC acquired it, so no such studies are available, but it did apply for a permit for a 40,000tpa lithium chloride facility just before it was acquired, which would be about 12,000tpa lithium carbonate. This isn’t representative of the project’s ultimate potential, but does indicate a minimum expected production level at the project’s rather juvenile stage of development and exploration.

Thesis Risks

The greatest source of upside in this thesis comes from a recovery in lithium prices, which is certainly not guaranteed. However, it is clear that LAAC’s projects would be profitable at current lithium prices and, as will be discussed later, lithium price recovery is not required for a successful investment thesis.

That said, this investment is at its best with a recovery of lithium prices to my projected figure of $35,000/tonne. While the cyclicality of the lithium industry does provide a certain level of confidence that this mark will be reached, the pricing forecasts of lithium are incredibly speculative in nature. Furthermore, if the market does reach this level, it will likely be followed by another period of contracting prices following an oversupply where, although still quite profitable, the strength of the investment does decline.

I do not expect lithium prices to begin to reach a level of stability until closer to 2030, perhaps even past then, at which point I believe prices will stabilize closer to $24,000/tonne. Though, this wouldn’t be a consideration for medium-term investors.

Geographically, Argentina isn’t the most stable region in the world. Earlier this year, the Catamarca province halted new mining permits pending an environmental study. While this doesn’t impact LAAC, who has projects in Jujuy and Salta, it may be something to keep an eye on.

However, the Country passed the Large Investments’ Incentive Regime earlier this month, which seems to take a favorable outlook on foreign investments in a number of Argentinian industries including mining. The bill requires at least $200 million to be spent on development of the project, with 40% spent within two years and 20% of investments must go to local suppliers.

Applications for new projects and expansions that meet these requirements are now open and the corporate tax rate for projects that meet these requirements has been lowered from 35% to 25% though provinces may charge a 5% royalty (previously 3%). Export proceeds can also remain in USD from year 4 of the project onward (20% in year 2, 40% in year 3), though projects where the investment exceeds $1 billion have this timeline accelerated by a year.

At this stage of the company’s life, funding isn’t too much of a concern anymore. The first stage of Cauchari-Olaroz has already been fully constructed and the company had $86.2 million in cash and equivalents at the end of Q1 with $95 million of available debt it has yet to draw on. The company posted a net loss of $10.2 million in the first quarter, indicating quite a significant capital runway for its current operations.

To fund future operations, the company has its aforementioned undrawn debt, as well as Ganfeng’s $70 million investment into the Pastos Grandes project which is expected to close in the current quarter. The company should also be able to utilize its existing operations to help fund future projects and expansions, or raise additional capital as needed with more favorable terms once it is profitable.

It is worth noting that the company has $225 million in outstanding 1.75% convertible notes due in 2027 with an effective redemption price of $16.96 per share (~450% upside from current price; 36/64 separation ratio). While it is possible that this debt will be converted into shares, investors shouldn’t necessarily expect this given the significant price appreciation required.

Regarding execution risk, Ganfeng lends significant credibility to all of LAAC’s projects as one of the largest lithium producers in the world with its own operational brine assets. Furthermore, LAAC has already contracted 80% of its Phase 1 offtake to various customers at market prices, further reducing the company’s future risk.

Valuation

As I’ve already discussed, by some of the most conservative metrics available, Cauchari-Olaroz alone is worth around $877 million to LAAC’s shareholders. This doesn’t factor in the expansion, consider that the production ramp is still expected to be completed by year-end (or early 2025), nor acknowledge the potential for lithium prices to climb above their current levels.

Even without any increase in lithium prices, at a P/E of 10, LAAC would be trading at a value of ~$1 billion (following the new Argentinian tax legislature) upon reaching nameplate capacity at Cauchari-Olaroz. Given the planned 20,000tpa expansion and the company’s additional holdings in the Pastos Grandes and Pozuelos salars, this is likely a conservative multiple.

At the company’s current valuation of around $470 million (at the time of writing), there’s about 85% implied upside to the NPV of Cauchari-Olaroz or about 115% upside upon reaching nameplate capacity at Cauchari-Olaroz with current lithium prices. At prices of $35,000/tonne and a P/E of 10, LAAC would trade at ~$4 billion or over 700% upside.

While this may seem like quite a quick turnaround, note how quickly lithium prices can change based on prevailing market conditions. If there is indeed a shortage by next year, prices would likely reach this level before the year’s end.

For those that are interested in LAAC as a long-term hold, consider the following but recognize that it is highly speculative in nature given the volatility of the lithium market and lack of guidance regarding production volumes at Pastos Grandes and Pozuelos.

At full commercialization across all of its projects, assuming a P/E of 5 and sales price of $24,000/tonne, LAAC would trade above $5 billion. This provides over 1,000% upside, though the timeline for this would likely be over five years.

Investor Takeaway

At a time where every other facet of the market seems to be booming, it can be a hard pitch to move capital into an underperforming area with somewhat speculative upside. That said, the upside that LAAC offers, even without any improvement to current lithium prices, makes it an extraordinarily compelling case for investors that are willing to have some patience and potentially ride out some share price weakness.

Even without its expansion, Cauchari-Olaroz is the largest new brine project since SQM Atacama project came online back in 1997, allowing the company to occupy the lowest end of the cost curve at a time where new hard-rock projects have substantially increased the average cost to produce lithium. This is an incredibly rare asset to be able to invest in for the industry, especially at this stage of development. The company’s holdings in the Pastos Grandes and Pozuelos salars have the potential to rival Cauchari-Olaroz in terms of production scale, giving investors a cheap entry into two of the world’s premier lithium assets.

Right now I like LAAC more than its North American brother LAC, as the latter faces dilution concerns with its General Motors (GM) investment and is still a few years away from starting commercial production. While LAC may offer greater speculative upside, LAAC’s experienced partner and project maturity make it the better investment right now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here