Note:

I have covered Lordstown Motors Corp. (OTC:RIDEQ) previously, so investors should view this as an update to my earlier articles on the company.

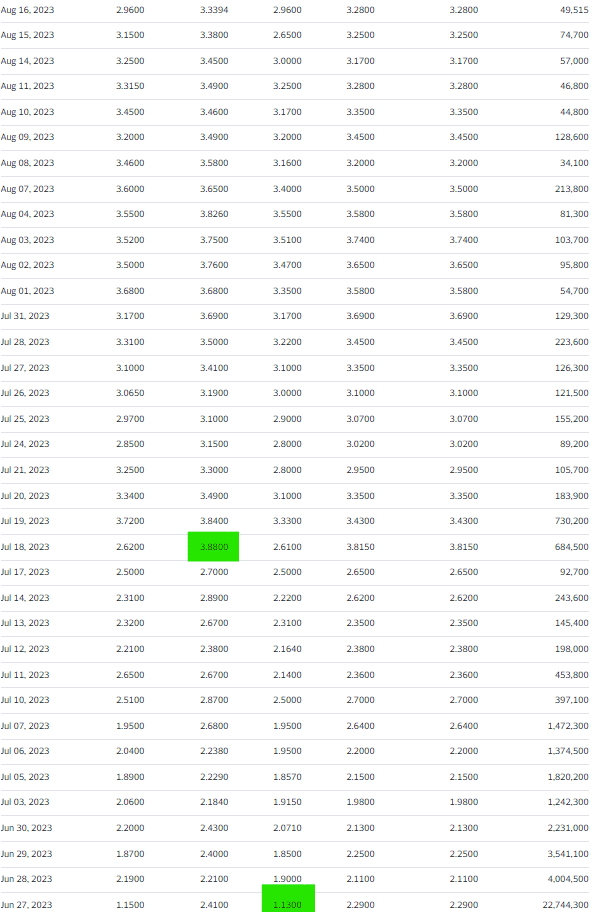

Since filing for bankruptcy protection in late June and subsequent delisting by Nasdaq, shares of embattled electric vehicle (“EV”) start-up Lordstown Motors Corp. or “Lordstown” have staged a surprise rally on the Pink Sheets:

Yahoo Finance

At their peak, shares were up by almost 250% from their June 27 low, likely due to the fact that, according to court documents, the company entered bankruptcy proceedings with $137.7 million in cash on hand while claiming “billions of damages” under its adversary complaint against former strategic partner Hon Hai Precision Industry Co., Ltd. (“Foxconn”).

Not surprisingly, Foxconn has filed a motion to dismiss the Chapter 11 petition or convert it to Chapter 7 liquidation asserting that the company sought Chapter 11 protection “in bad faith and without a valid bankruptcy purpose.“

The motion also states the low level of disputed trade payables among the company’s thirty largest creditors (approximately $20 million) and even points to a potential distribution to equity holders in Chapter 7 (emphasis added by author):

Many of the same elements that favor dismissal of the Chapter 11 Cases also support conversion. First, the administrative expenses of a panel chapter 7 trustee would be substantially less than the costs of administering the estate in chapter 11. This is not a “no asset” case or one where there is no equity, such that the chapter 7 estate would be run exclusively for the benefit of a secured creditor. A chapter 7 trustee may expeditiously and fairly resolve the various disputed claims against the Debtors in a centralized forum and make distributions to all unsecured creditors and, potentially, to equity.

However, the company is currently incurring approximately $6.2 million in monthly cash expenses and has reserved $35 million in connection with ongoing securities litigation.

Earlier this week, Lordstown Motors agreed to settle long-standing litigation with Karma Automotive LLC (“Karma”) ahead of a scheduled trial against a $40 million cash payment.

Perhaps most important, the Karma settlement filing also contained a cautionary note regarding trading in the company’s common stock (emphasis added by author):

The Company’s stockholders are cautioned that trading in shares of the Company’s Class A common stock during the pendency of the Chapter 11 Cases will be highly speculative and will pose substantial risks.

The Company cannot be certain that holders of the Class A common stock will receive any payment or other distribution on account of those shares following the Chapter 11 Cases.

As a result, the Company expects that its currently outstanding shares of Class A common stock may have little or no value.

Trading prices for the Company’s Class A common stock may bear little or no relation to actual recovery, if any, by holders thereof in the Company’s Chapter 11 Cases.

Accordingly, the Company urges extreme caution with respect to existing and future investments in its Class A common stock.

Earlier this week, the company filed its second quarter report on form 10-Q with the SEC which shows approximately $85 million of “liabilities subject to compromise“:

Regulatory Filing

However (emphasis added by author):

This accrual does not reflect a full range of possible outcomes for these proceedings or the full amount of any damages alleged, which are significantly higher. Any such additional losses may be significant; however, the Company cannot presently estimate a possible loss contingency or range of reasonably possible loss contingencies beyond current accruals. Estimating probable losses requires the analysis of multiple forecasted factors that often depend on judgments and potential actions by third parties.

The Bankruptcy Court has not established the deadline by which parties are required to file proofs of claim in the Chapter 11 Cases. There is substantial risk of additional litigation and claims against the Company or its indemnified directors and officers, as well as other claims by third parties that may be known or unknown and the Company does not have the resources to adequately defend or dispute due to the Chapter 11 Cases. The Company cannot provide any assurances regarding when such deadline will be, the amount or nature of the claims that may be filed by such deadline, or what the Company’s total estimated liabilities based on such claims will be.

With the vast majority of the company’s remaining funds likely to be spent on settlement payments and satisfying unsecured creditors’ claims as well as covering the administrative expenses of the chapter 11 proceedings, a meaningful recovery for common shareholders will largely depend on potential damages awarded in the Foxconn litigation as I do not expect the upcoming auction of the company’s assets to yield substantial proceeds.

Lastly, investors should note that Foxconn owns $30 million of the company’s Series A Convertible Preferred Stock which ranks ahead of common equity. On the flip side, Lordstown Motors has filed a motion for equitable subordination pursuant to Section 510(c) of the U.S. Bankruptcy Code.

Given the recent rally in the shares and very real chances for a wipeout, I am downgrading shares from “Hold” to “Sell“.

Risks

As discussed above, a material award under the Foxconn litigation would vastly improve prospects for common equity holders.

Bottom Line

As bankruptcy proceedings continue, Lordstown Motors has officially warned investors of its shares potentially having “little or no value” and absent any material award under the ongoing Foxconn litigation, I tend to agree with the company’s assessment.

Given the recent rally in the shares and very real chances for a wipeout, I am revising my rating on the shares from “Hold” to “Sell“.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here