Investment Thesis

New York Mortgage Trust (NASDAQ:NYMT) recently missed top-line and bottom-line estimates in the last quarter earnings, igniting a sell-off in the stock over the past trading week. I believe the stock is now trading at an attractive discount to adjusted book value, with strong liquidity to enhance the balance sheet in a potentially weakening economy. Management has shown to be strong capital allocators and excited for opportunistic growth opportunities in their mortgage portfolio. All of this spells a buy rating in my opinion, as I believe shares have bottomed and the fundamentals should trend more attractive going forward.

Company Overview

New York Mortgage Trust is “an internally-managed REIT for U.S. federal income tax purposes, in the business of acquiring, investing in, financing and managing primarily mortgage-related single-family and multi-family residential assets” according to their annual report. They invest in mortgage back securities, specifically focused on agency RMBS.

Their current investment portfolio consists of “credit sensitive single-family and multi-family assets, as well as more traditional types of fixed-income investments that provide coupon income, such as Agency RMBS”. In essence, they profit from making the spread between the interest earned on their assets and the interest paid on their liabilities.

Leverage sits at a pretty conservative level, at around 2.1x at the time of this writing. I believe management has confidence in the risk profile of their assets, so they are slowly amping up leverage to amplify returns for their shareholders. New York Mortgage seems to have managed risk well by focusing on Agency RMBS, which have lower credit risk due to their government backed guarantee.

In the company’s own words in their 10-K, “We believe that Agency RMBS is a compelling asset class to invest in over the near term, as the sector is trading at historically widespread levels resulting from volatility in interest rates and reduced demand from regional banks and the Federal Reserve”. This focus has led the fundamentals to perform resiliently, as second quarter adjusted income increased 63% compared to the same period last year.

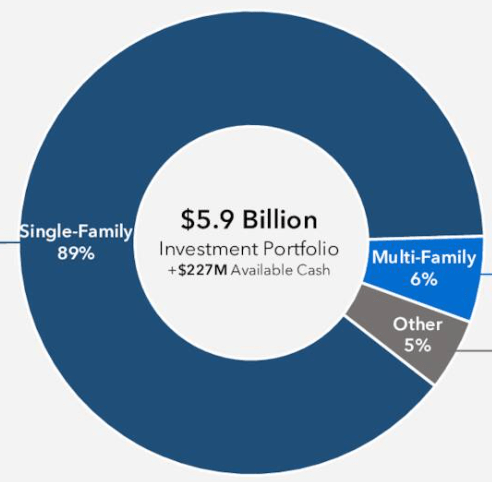

Investor Presentation

With a $5.9 billion investment portfolio and most of it tied up in single-family assets, management seems to have leaned heavily into agency RMBS that are performing well for shareholders. My opinion is that these assets seem to have lower-risk, as the average coupon on these single-family agency RMBS is 5.84%, according to the investor presentation. In their own presentation, their focus on the agency RMBS gives investors “high carry and compelling risk-adjusted returns”. Therefore, investors should note that most of their asset portfolio is concentrated in single-family residential loans.

Growing The Portfolio

New York Mortgage reported Q2 2024 earnings with the following results:

- Net loss of attributable to Company’s common stockholders of $26.028 million

- Yield on average interest earning assets of 6.46%

- Net interest income of $19.044 million

- Adjusted book value per share of $11.02

Overall, the asset portfolio has continued to grow despite a declining share price, highlighting the resiliency of the portfolio in my view. In particular, the company “purchased approximately $467.5 million of Agency RMBS with an average coupon of 6.00%” and “purchased approximately $420.7 million in residential loans with an average gross coupon of 10.42%” according to the press release.

I believe this signals the overall strength of the portfolio and shows how important liquidity can be in this current period of the MBS markets. NYMT’s strong cash balance and liquidity position allows them to play offensive and grow their adjusted current income for the next few quarters.

Furthermore, management comments, “with potential excess liquidity of $424 million, or 42% of NYMT’s market capitalization at the end of the second quarter, we are focused on meaningfully raising current income in subsequent quarters”. Management shows to be adept in rotating capital out of lower-earning assets into higher-earning ones, with increases in net interest income confirming my bullish take.

In conclusion, the quarter was quite bullish for investors in my opinion as it highlights management’s ability to rotate capital, a strong balance sheet with excess liquidity, and a growing investment portfolio with opportunistic investments. I like what I see here and expect a gradual turnaround in the share price.

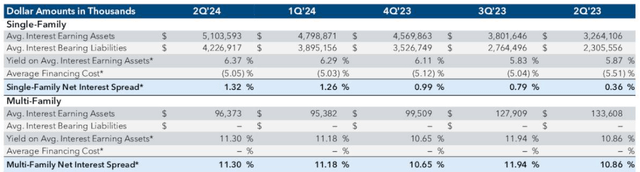

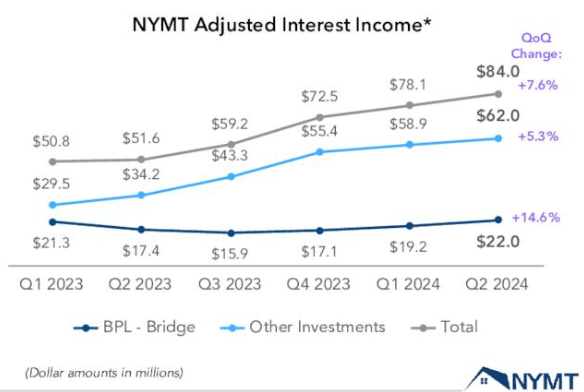

Agency RMBS Becomes More Attractive

I believe profitability will improve for NYMT because of the widening spreads that we are seeing across single-family and multi-family assets in their portfolio. According to their investor presentation appendix, investors can see the improvement in spreads:

Investor presentation

This gradual improvement has been unnoticed by the market, in my opinion, with the stock still selling at a too big a discount to adjusted book value. Adjusted net interest income continues to rise as management focuses on acquiring lower-risk, agency RMBS that have a solid track record of performance. With an average FICO score of 727 for their agency RMBS portfolio according to their presentation, I believe the agency RMBS are a good choice in this market for their solid coupons and significantly reduced credit risk.

Investor presentation

As spreads continue to widen in my opinion going forward, I expect NYMT’s profitability to trend higher. Given that these loans are also backed by GSEs, I’m also not too worried about credit risk. All in all, I believe the focus on agency RMBS is attractive in this market environment as single-family loans are set to potentially outperform in an economic downturn. Management elaborates in the earnings call,

We believe that Agency RMBS is a liquid asset class that can outperform through a future rate easing cycle. It also can exhibit resiliency through a recessionary environment at which time we can rotate the capital into discounted higher return opportunities.

Therefore, I think Agency RMBS is a good pocket in the market that NYMT is correctly focusing on as part of their investment strategy. With strong liquidity and wider spread levels, I expect overall earnings to grow and book value to stabilize. The dividend should be well-covered, giving income investors a nice double-digit yield that in my view should be sustainable.

Valuation – $11 Fair Value

I believe the stock deserves a fair value equal to its book value, given the increasing confidence I have in the earnings capability of NYMT. Therefore, my $11 price target is equal to the adjusted book value per share as of the last quarterly earnings report.

Investors are getting a nice dividend yield of over 12% at the time of this writing, which I believe at this point can be sustained. Management has shown to be prudent capital allocators and have strengthened the balance sheet with excess liquidity. They have more money than they need, so at this point management seems to be on the offensive.

Furthermore, recent buybacks signal that management believes their stock to be undervalued on their earnings call,

As reinvestments accelerate and we continue to build out interest income, we evaluate opportunities to repurchase shares at a significant discount against our high performing book that contains elevated concentrations of agency and cash on balance sheet.

A combination of Agency RMBS and cash can be seen as the most liquid, low-risk assets there can be on the market, in my opinion. Therefore, the adjusted book value is pretty safe in my view due to its high liquidity. I expect share buybacks to ramp up as it presents a high hurdle rate for management to beat when they assess reinvestment opportunities.

Risks

Americans seem to be strapped for cash at the moment, as more of them are living paycheck to paycheck in today’s economy. With recent news of a potential recession incoming, it may be hard for more borrowers to make interest payments on their debts. While this may not affect the Agency RMBS as they are government guaranteed, a potential recession may trigger more defaults and delinquencies, which may cause the market values of non-agency MBS to decline, affecting a part of NYMT’s investment portfolio.

The real estate market continues to be unaffordable for most Americans, making it potentially difficult for NYMT to achieve sustainable growth. There are only so many Americans out there that can safely afford a home, and as home prices continue to be out of reach for most, this could pose a challenge to long-term growth in earnings for NYMT.

Increase in leverage could give shareholders pause because even though they increase returns, they amplify the risk on the balance sheet as well. Failure to manage their liabilities carefully could result in potential liquidity challenges. Although liquidity is strong now, poor market and investment performance could weaken the increasingly levered balance sheet.

Buy New York Mortgage Trust

I believe that the mREIT stocks in general are too cheap as a whole, and I’ve handpicked a couple of them in my recent articles that I believe are solid buys. Not all mREITs are created equal of course, but NYMT stood out has a nice turnaround play with improving fundamentals to back up the bull thesis. With a focus on Agency RMBS, they are uniquely positioned to weather an economic downturn.

All in all, this stock may be interesting to income investors who are looking for solid dividends in their portfolio. If the common is too risky for readers, they can also check out the preferred (NASDAQ:NYMTN) and even the senior notes (NASDAQ:NYMTI) for nice income as well. The company overall should be able to pay out dividends for all these securities in my opinion, but I think the common is the most attractive out of all the available securities and rate these shares as a buy.

Read the full article here