NLCP’s Cannabis REIT Investment Thesis Remains Robust

We previously covered Innovative Industrial Properties (NYSE:IIPR) discussing its sustainable and profitable REIT operations, despite the uncertain federal legalization process and elevated interest rate environment.

For this particular article, we will be looking at NewLake Capital Partners (OTCQX:NLCP) and sharing our findings about the stock, continuing the theme surrounding the cannabis REIT sector.

For the uninitiated, NLCP is a REIT focusing on state-licensed cannabis operators while providing the usual sale-leaseback transactions, third-party purchases, and funding for build-to-suit projects.

With the cannabis REIT set to report its upcoming FQ2’24 earnings call on August 8, 2024, readers may want to monitor a few metrics ahead, with these underscoring its near-term prospects.

1. Tenant Health & Rental Collection

With the state-level legalized cannabis market being relatively small, it is unsurprising that NLCP’s tenant concentration is relatively high with the biggest tenant, Curaleaf (OTCPK:CURLF) representing the largest aggregate annualized rental revenues at 23.8% in FY2023 (+0.8 points YoY), Cresco Labs (OTCQX:CRLBF) at 13.6% (+0.5 points YoY), and Trulieve (OTCQX:TCNNF) at 11.6% (+0.4 points YoY).

For now, these three tenants have continued to report improving adj EBITDA and Free Cash Flow profitability on a QoQ/ YoY basis, after the painful cannabis meltdown in 2022/ 2023.

These developments further underscore why NLCP has been able to report six consecutive quarters of top/ bottom-line beats, with the FQ2’23 misses only attributed to the Revolutionary Clinics rental delinquency.

With the Rev Clinic issue fully resolved (page 52), we expect the cannabis REIT to sustain its robust top/ bottom-line performance moving forward, as observed over the past three years at an impressive CAGR of +59.3% and +15% (AFFO per share), respectively.

Much of NLCP’s tailwinds are naturally attributed to its elongated weighted average lease term remaining of 14.1 years and the rather generous 2.6% in annual rental escalations, compared to the average increases based on changes in the CPI at ~2%.

Combined with the relatively low general and administrative expense with an annualized ratio of 1.6% of total assets – similar to IIPR at 1.6%, it is unsurprising that NCLP reports a relatively rich spread of 11.7%, naturally assuming that all rent is collected.

Even so, readers may want to pay attention to NLCP’s upcoming earnings call, since the uncertain macroeconomic outlook and uncertain federal legalization may pose headwinds to its tenants’ intermediate-term prospects.

2. Dividend Safety

The whole point of investing in stocks, in my humble opinion, is to achieve capital appreciation and/ or dividend payouts, depending on individual investor’s portfolio allocation and investing trajectory.

With NLCP being a REIT and required to “distribute at least 90 percent of their taxable income to shareholders as dividends,” the most obvious reward (for now) is its rich dividend yields of 9.07%.

This is compared to the 4Y average of 7.29%, the general REIT sector of 4.36%, and the US Treasury Yields of between 4.09% and 5.33%.

NLCP’s dividend investment thesis appears to be robust as well, thanks to the growing AFFO per share and the recent dividend hike by +4.8% to an annualized sum of $1.72, building upon the robust 3Y Dividend Growth at a CAGR of +9.7%.

This is especially given the consistent moderation in the US core CPI to 3.3% by June 2024 (-0.1 points MoM/-1.5 YoY), with us nearer to the pre-pandemic averages of 2% than the September 2022 peak of 6.2%.

As a result of the cooling inflation on a QoQ and YoY basis, the market has already priced in a Fed rate cut in the September 2024 FOMC meeting, with the European Central Bank [ECB] also announcing a rate cut from 4% to 3.75% by June 2024 while joining other countries such as Canada, Sweden and Switzerland.

Combined with the likely reclassification of cannabis from Schedule 1 to Schedule 3 drug and the eventual SAFER Banking Act, we believe that NLCP’s dividend investment thesis remains highly attractive for those seeking steady incomes during a disinflationary and Fed rate cutting environment over the next two years.

On the one hand, readers may want to pay attention to NLCP’s execution over the next few quarters, since the current FWD AFFO payout ratio of 79% is lower than its target AFFO payout ratio of between 80% and 90% and the 91.1% reported in FQ1’23.

This implies that there is a moderate cushion for further dividend payout hike, significantly aided by the cannabis REIT’s inherent lack of long-term debt and minimal reliance on Revolving Credit Facility at $4M in FQ1’24.

On the other hand, anyone concerned about NLCP’s overly rich payout ratios need not fret, since the same trend has been reported by IIPR at 85.9% in FQ1’24 (+5.1 points YoY), well beyond the general REIT averages of 74.5%, further exemplifying the cannabis REITs’ compelling dividend investment thesis.

This is especially since the cannabis REIT market is currently dominated by both NLCP and IIPR, with their expertise in the market offering the significant lead and advantage over general REITs in the event of federal legalization.

If anything, there is a good chance that cannabis REITs may be potential takeover targets by bigger REIT players, such as Realty Income (O) or VICI Properties (VICI), given their diversification efforts thus far, with it offering capital appreciation prospects upon the speculative event.

Only time may tell.

So, Is NLCP Stock A Buy, Sell, or Hold?

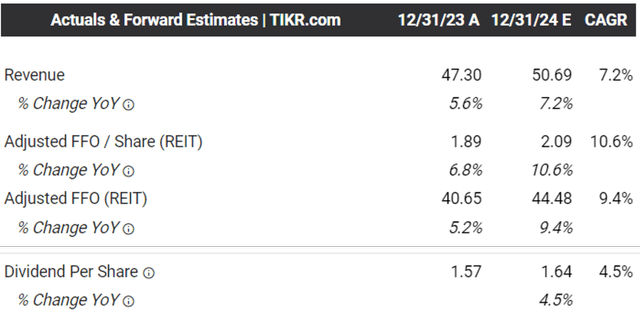

The Consensus Forward Estimates

Tikr Terminal

For now, BDSA has projected an excellent US cannabis market size growth CAGR of +10.5% through 2027, implying NLCP’s robust prospects no matter the uncertain legalization.

The same has been observed in the promising consensus forward estimates, with the cannabis REIT expected to generate a promising YoY growth in top-line by +7.2% and AFFO per share growth by +10.6% in FY2024.

This builds upon the FQ1’24 performance at +10.4% YoY/ +15.5% YoY and the 3Y historical performance at a CAGR of +59.3%/ +15%, respectively.

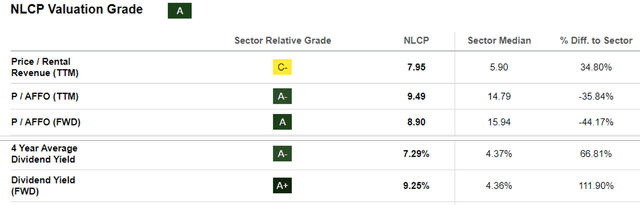

NLCP Valuations

Seeking Alpha

As a result of the robust performance thus far, we believe that NLCP remains overly discounted at FWD Price/ AFFO valuation of 8.90x, though upgraded from its 1Y mean of 8.50x – still lower than the 3Y mean of 10.15x and the general REIT sector of 15.94x.

At the same time, NLCP looks cheap compared to IIPR at 13.27x, given that the latter is only expected to generate an inline AFFO per share YoY performance in FY2024.

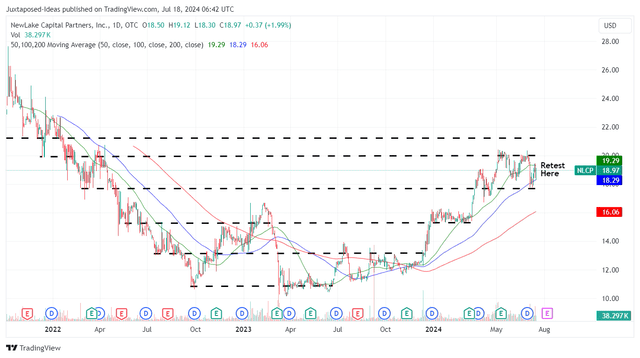

NLCP 3Y Stock Price

Trading View

Based on its discounted stock valuations of FWD Price/ AFFO valuation of 8.90x and the consensus FY2024 AFFO per share estimates of $2.09, NLCP is also trading near to our fair value estimates of $18.60.

Assuming an upward rerating in the stock’s valuations nearer to its peer at ~13x and a sustained bottom-line growth at a CAGR of +10% to an estimated FY2025 AFFO per share of ~$2.29, we are looking at a bull-case 2Y price target of $29.70 as well, implying an excellent upside potential of +56% from current levels.

As a result of the attractive risk/ reward at current levels, we are initiating a Buy rating for NLCP here.

It goes without saying that the REIT’s involvement in a relatively risky cannabis sector implies that the stock may be exposed to further volatility, depending on the uncertain federal legalization and the ongoing US elections.

As a result of the potential volatility, anyone whom buy NLCP may also want to size their portfolios according to their dollar cost averages and risk appetite, as we await the upcoming FQ2’24 earnings call on August 8, 2024.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here