Investment Thesis

Since my last coverage three years ago, Oaktree Specialty Lending Corporation (NASDAQ:OCSL) has seen its stock price decline by nearly 10%. It has underperformed the broader market, returning 23%, below the broader market’s 29% return. Despite this underperformance, OCSL presents an attractive entry point, trading at a 0.95x Price/NAV multiple.

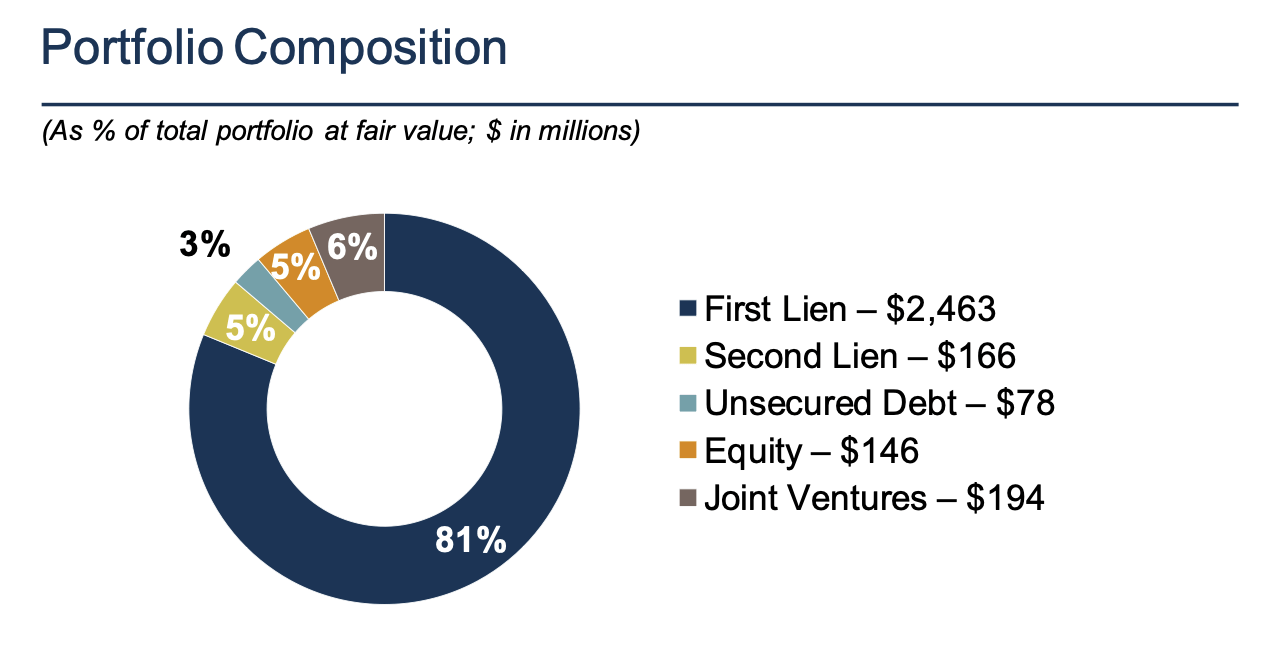

OCSL’s portfolio comprises first-lien loans, accounting for 81% of total investments. High-priority debt instruments strongly protect against defaults, underpinning income stability and asset valuation. The decline of non-accrual investments from $120.7 million to $69.1 million in Q2 2024 further captures the improvement that has been made in credit quality, thereby providing further stability to net asset value (NAV) and boosting overall financial health.

The recent cut in OCSL’s base management fee from 1.50% to 1.00% will likely benefit net investment income and increase the earnings available for distribution to shareholders. Also, considering $1 billion in liquidity and a 1.02x net debt-to-equity ratio, OCSL is well positioned to take advantage of new investment opportunities and continue to make distributions consistently, thus showing robust cash flow and financial stability. Such factors all support a bullish outlook on OCSL, thus earning the buy rating.

$3 Billion Portfolio: A Fortress of Senior Secured Debt and Strategic Diversification

Oaktree Specialty Lending has a diversified and intelligently structured investment portfolio that helps mitigate risk and enhance returns. As of Q2 2024, the portfolio was $3.0 billion across 151 companies. The portfolio is skewed towards senior secured debt, which accounts for around 86% of the total investments. This includes 81% in first-lien loans, emphasizing debt instruments that would offer high-priority protection against potential defaults by portfolio companies.

An excess majority of senior secured debt, especially first-lien loans, makes a supreme effort to manage risk in this portfolio. First-lien loans are ranked the highest in the repayment waterfall, and thus, OCSL has the highest claim on a borrower’s assets in the case of liquidation. This strategic choice allows for reducing possible losses and, at the same time, generating reasonable interest income, thus adding stability and safety to the whole portfolio.

OCSL

Strategic Tech Sector Diversification

OCSL’s broad diversification across multiple industries helps cushion the impact of sector-specific downturns. The software sector commands the most significant industry exposure, which carries some concentration risk at 19% but also denotes confidence in this sector’s robust growth and resilience. Biotechnology and industrial machinery follow, thus further diversifying and exposing it to high-potential growth areas.

OCSL’s 19% exposure to the technology sector, particularly in software, is strategically mitigated through several robust financial and structural measures. The software portfolio, valued at $579 million and comprising 24 companies, focuses on mission-critical solutions that ensure high customer retention and recurring revenues. This selection criterion inherently reduces revenue volatility and default risks. Additionally, the diversification across various end markets, including application software (16.3%), IT consulting & other services (12.2%), and alternative carriers (9.4%), minimizes the impact of downturns in any single sub-sector. Such diversification spreads the risk and stabilizes overall portfolio performance.

Despite technology companies often lacking tangible assets, first-lien loans protect OCSL significantly. These loans ensure priority claims on valuable intangible assets such as intellectual property, software, patents, and customer contracts. They also secure rights to structured cash flows and receivables, which can be substantial in the tech sector. First lien status includes strict covenants, offering control and oversight over the borrower’s financial activities, and historically results in higher recovery rates even for intangible assets. Therefore, first-lien loans in tech investments offer OCSL critical security and stability, effectively managing risk in its portfolio.

Furthermore, 90.3% of the software portfolio consists of first-lien loans, which provide top-tier protection against defaults by giving OCSL the highest claim on a borrower’s assets in case of liquidation. This structural preference for first-lien investments ensures better recovery rates and lowers the risk of capital loss. The portfolio’s solid financial metrics further enhance its stability; with an average portfolio company revenue of $577 million and an average loan-to-value (LTV) ratio of 39%, the loans are well-secured by collateral. Low LTV ratios mean the loans are less risky as they are backed by significant collateral value.

Assessing the Financial Health of OCSL’s Application Technology Investments Through FV

OCSL’s total cost invested in the application software industry is $408.91 million, with a fair value (FV) of $404.22 million. This results in a fair value loss of $4.69 million, or approximately 1.15%. FV is crucial for OCSL as a debt investor, particularly in first-lien loans, as it reflects the current market valuation and recoverable amount of secured assets in the event of borrower default. A decrease in FV signals potential risks such as declining asset quality and financial performance of the borrowers. It’s important to note that the 19% exposure to the technology sector also includes other industries like IT consulting, alternative carriers, and interactive media, which are not included in this analysis.

| Company | Cost (Millions) | Fair Value (Millions) | FV Gain/Loss (Millions) |

|---|---|---|---|

| Acquia Inc. | $32.54 | $32.66 | $0.12 |

| Avalara, Inc. | $49.66 | $50.34 | $0.68 |

| Astra Acquisition Corp. | $13.24 | $10.12 | -$3.12 |

| Coupa Holdings, LLC | $12.87 | $12.96 | $0.09 |

| Digital.AI Software Holdings, Inc. | $57.66 | $57.11 | -$0.55 |

| Enverus Holdings, Inc. | $24.47 | $24.51 | $0.04 |

| Evergreen IX Borrower 2023, LLC | $14.32 | $14.65 | $0.33 |

| Finastra USA, Inc. | $11.73 | $11.51 | -$0.22 |

| Icefall Parent, Inc. | $10.24 | $10.25 | $0.01 |

| iCIMS, Inc. | $28.27 | $27.72 | -$0.55 |

| IPC Corp. | $40.04 | $38.76 | -$1.28 |

| Monotype Imaging Holdings Inc. | $37.82 | $37.86 | $0.04 |

| MRI Software LLC | $34.78 | $34.73 | -$0.05 |

| OEConnection LLC | $9.22 | $9.20 | -$0.02 |

| Relativity ODA LLC | $32.11 | $31.84 | -$0.27 |

Source: OCSL’s 10Q

Therefore, these factors collectively mitigate the perceived concentration risk, making OCSL’s technology sector investments a sound and strategically managed part of its portfolio.

OCSL’s Yield Advantage: Floating Rates Propel Strong 12.2% Returns Amid Economic Shifts

The weighted average yield on the debt investments remains strong at 12.2%. The average yield of new debt investments during the quarter stood at 11.1%. This is an excellent rate, considering that interest rates are rising and notwithstanding the competitive environment. This critical yield is necessary for income generation to be distributed back to shareholders as dividends by OCSL.

Rising interest rates have benefited the company by increasing interest income on its predominantly floating-rate loan portfolio. Thus, floating-rate instruments form about 85% of OCSL’s debt portfolio, which has been committed to benefiting from rising interest rates. Therefore, the income from these investments will increase with rate rises. The macroeconomic environment must be closely monitored to help manage the possible impacts on borrower stability and repayment ability. Lower interest rates may also improve portfolio companies’ financial health by reducing their debt servicing costs, potentially leading to decreased non-accrual investments and improving overall portfolio stability.

Additionally, through interest rate swaps, Oaktree Specialty Lending reduces its exposure to adverse changes in interest rates. For instance, OCSL has entered into swap agreements to manage the impact of interest rate changes on its debt. One of the interest rate swap agreements as of September 30, 2023, allows OCSL to pay a floating rate based on the three-month SOFR plus 3.1255% on a notional amount of $300 million. This strategy is undertaken to stabilize interest expense and reduce the risk that rising interest rates would hurt the company’s overall operating performance.

Conversely, a drop in interest rates would significantly impact OCSL’s portfolio by reducing interest income from its floating-rate loans, compressing portfolio yields, and potentially lowering NII and shareholder distributions. To mitigate these effects, OCSL might seek higher-yielding investments or increase fixed-rate debt exposure, though these strategies come with added risks. Lower rates could improve the financial health of portfolio companies by reducing debt servicing costs and potentially decreasing non-accrual investments. OCSL’s strong liquidity and disciplined leverage management provide resilience against interest rate volatility, ensuring financial stability and flexibility.

Robust Liquidity and Strategic Risk Management, A $1 Billion Buffer

OCSL ensures a strong liquidity position through $125 million in cash and $888 million in undrawn capacities on credit facilities for a total of $1 billion available from its liquidity. This will provide a sound liquidity buffer for ongoing investment activities and capture new opportunities without jeopardizing financial stability.

Its net debt-to-equity ratio stands at 1.02 times, reflecting prudent leverage management that ensures the company can meet its obligations while pursuing growth. Risk Management and Credit Quality Risk management forms one entity of the investment strategy at OCSL. The reduction of exposure to second lien structures from 16% in September 2022 to 5% as of Q2 2024 resettles and underscores the firm’s de-risking efforts for its portfolio. With an increased focus on first-lien investments, OCSL reduces the volatility and severity of potential loss related to subordinated debt instruments.

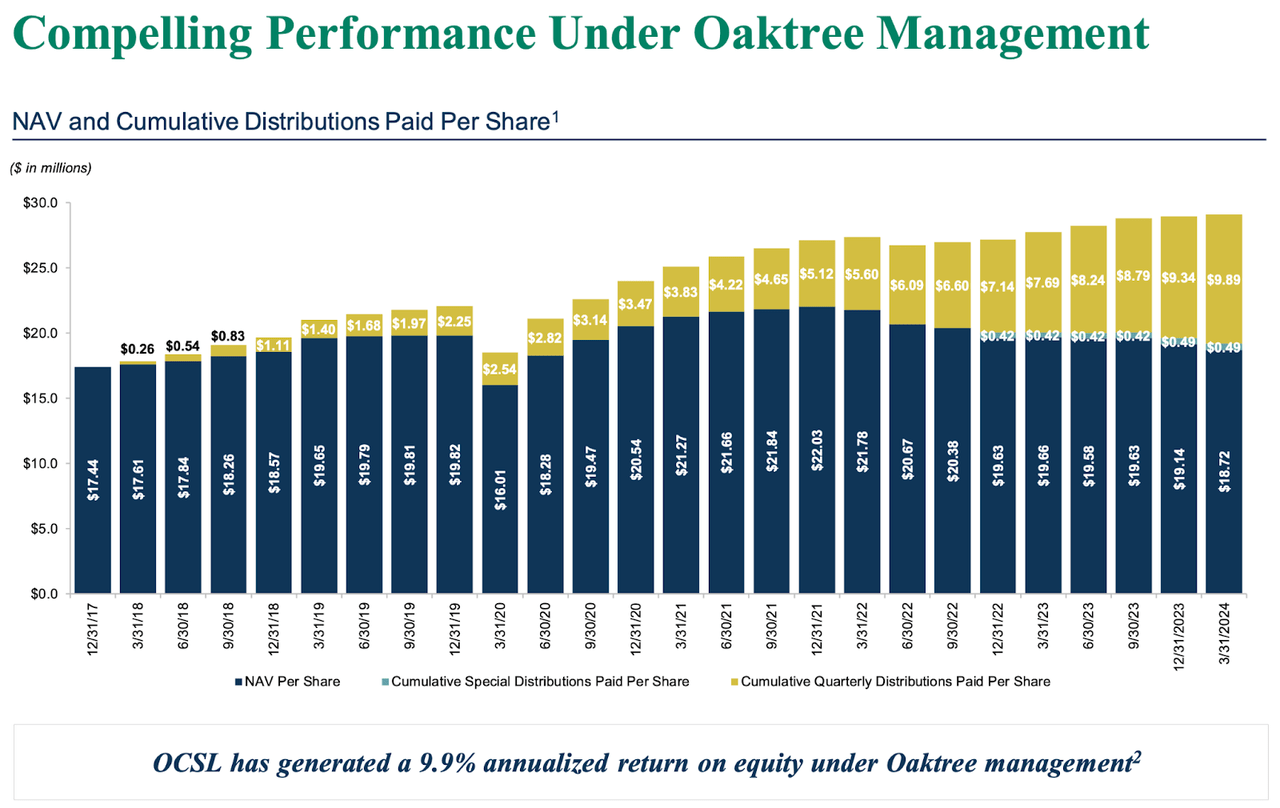

Q2 NAV Drops to $18.72 Amid Market Volatility and Strategic Shifts

As of March 31, 2024, OCSL had a net asset value of $18.72 per share, compared to $19.14 last quarter. The decline in net asset value was linked to both realized and unrealized losses from certain debt and equity investments. Net asset value is an important metric because it signals the value per share of the firm’s total assets less liabilities, and changes in it give information about a firm’s financial health and performance.

The drop in NAV was mainly due to realized and unrealized losses from some of the debt and equity investments, which could be prompted by deteriorating market conditions, decreasing credit quality, or strategic repositioning of an investment portfolio. This quarter, adjusted net realized and unrealized losses comprised $35.3 million, influenced by these market dynamics and investment decisions.

The adjusted total investment income for the quarter was $97.3 million, slightly below the previous quarter, due to lower interest income. This decline in income was partially offset by a reduction in net expenses, which decreased $1.1 million primarily due to lower part I incentive fees, professional fees, and interest expenses.

The strategic shift from second-lien to first-lien investments contributes to slight yield spread compression. This move will de-risk the portfolio with an increased percentage of first-lien senior secured debt. However, such a shift lowers yields and thus affects overall income generation, impacting NAV.

OCSL

The level of non-accrual investments also impacts NAV. As of March 31, 2024, non-accrual investments at fair value were $69.1 million, or about 2.4% of the total debt investments at fair value. This compares to $120.7 million in the prior quarter, indicating improved credit quality and potentially fewer defaults. Lower non-accruals generally help stabilize NAV by reducing the potential for large write-downs.

Although NAV has dropped, OCSL still went ahead with its dividend distributions, announcing $0.55 per share to be distributed for the fifth straight quarter. Consistency in paying dividends assures stable cash flows and speaks highly of the management concerning the company’s sound financial health. These distributions will help maintain shareholder value even when the base NAV is under short-term pressure.

Takeaway

Focusing on first-lien loans provides high-priority protection and stability, although elevated interest rates may challenge borrowers. The company’s cautious, selective investment approach and robust liquidity of $1 billion enable it to navigate volatility effectively. Oaktree’s expertise further supports prudent risk management, ensuring long-term performance and consistent dividends. Continuous monitoring of economic conditions and borrower performance is essential to sustain financial health and maximize shareholder value.

Read the full article here