Team of Business people working at workplace with tablet and document, doing planning analyzing Tax financial report, business plan investment, finance analysis Economic business discussions.

Oaktree Specialty Lending (NASDAQ:OCSL) is one of the highest yielding stocks out there. Boasting a juicy 11% yield, it pays out buckets of income. Although the company’s stock has never gone anywhere, the macroeconomic environment is changing in a way that could make Oaktree’s future better than its recent past. Interest rates have been rising for several years, and when interest rates rise, lenders make more money.

This point applies to banks as well as non-bank lenders like Oaktree, but the latter don’t have to worry as much about inverted yield curves squeezing their margins. As long as Oaktree’s borrowings have the same term to maturity as its loans, it faces no pressure from the inverted yield curve. In fact, the company just completed a bond offering at a 7.1% yield, which is far lower than the yield on its portfolio. This is a good thing because it shows that Oaktree can capture a wide spread and pass it on to investors in the form of a dividend.

Oaktree’s portfolio yield is 12.3%. That’s higher than OSCL’s dividend yield, which makes sense because the company does not pass on 100% of its earnings to investors. It has about a 90% payout ratio, which is high but basically workable if the company can borrow at rates lower than what it can lend at. The “inverted yield curve”–a problem for banks–is not a problem for Oaktree, because it can simply borrow at the same terms-to-maturity at which it lends.

In this article I make the case that Oaktree Specialty Lending is a good value at today’s prices. I address the company’s historical performance, explain why its long-term downward sloping stock chart is misleading, and why today’s macro environment favors the company. I will start with the company’s history and then move on to where it stands today.

Oaktree Specialty Lending: The History

Oaktree Specialty Lending was founded in 2007 as a business development company. A business development company (“BDC”) is a company that invests in small-to-medium sized businesses, often distressed ones. Congress invented them back in the 80s to help stimulate the economy. Often, the companies that BDCs lend to are struggling. This makes them risky, but also makes the yields high. If the portfolio managers at BDCs are quite smart, they can make loans to struggling companies that are not “struggling” as much as the markets think they are. OCSL is backed by Howard Marks, who has a 20% CAGR track record and is well connected with other highly intelligent financial professionals. So, there is reason to think that OCSL is in fact lending responsibly.

One aspect of Oaktree Specialty Lending’s history that some people object to is the long term decline in the stock price. Ignoring the reverse stock split, the company went public at $38.59. It trades for $20 today. So, those who invested in the early days would appear to have lost money, had they held the entire time. However, looks can be deceiving. OCSL has always paid very generous dividends, as a chart on Seeking Alpha Quant shows. Over the course of Oaktree’s history the dividends have summed to $13.82. So, on a total return basis OCSL is only “down” 12.3%, rather than the severe 40% loss the stock chart implies.

But there’s a key point that investors must keep in mind:

We were in a low interest rate environment for most of the last 16 years, the period in which Oaktree Specialty Lending has been a going concern. At one point, the federal funds rate was all the way down to 0.15%! Today, the Federal Funds Rate is 5.5%, and Oaktree has plenty of room to make money. As long as it borrows for less than the rates it lends at, it will be able to pass many generous dividends on to investors.

The Nature of the Business

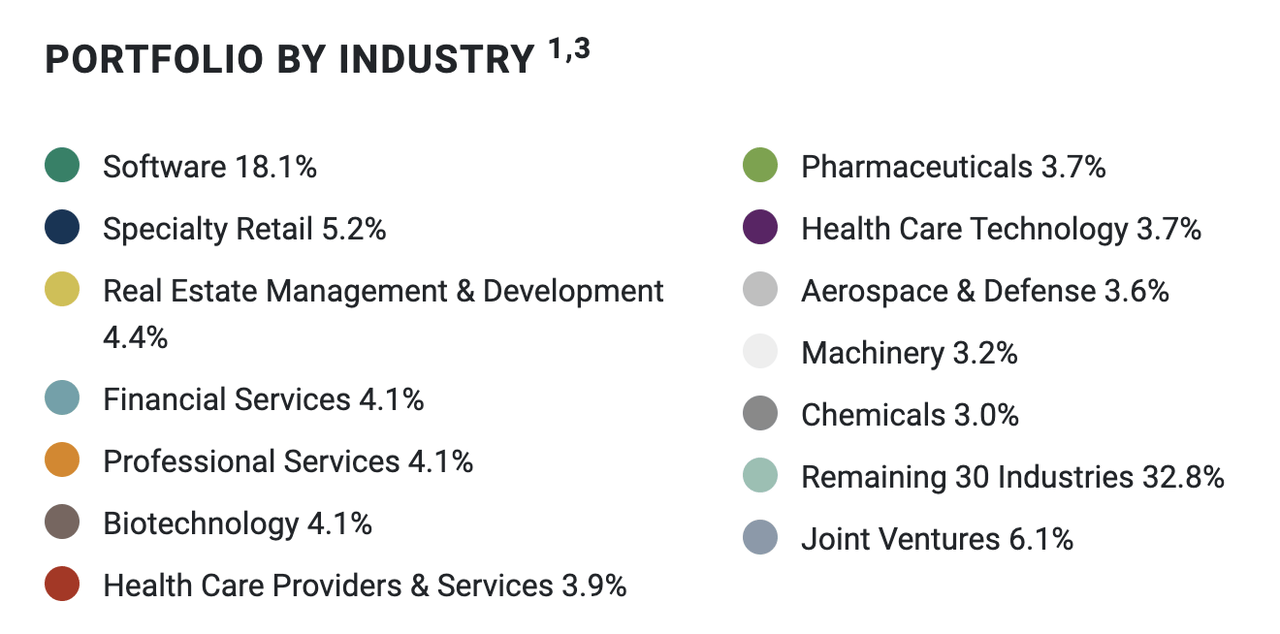

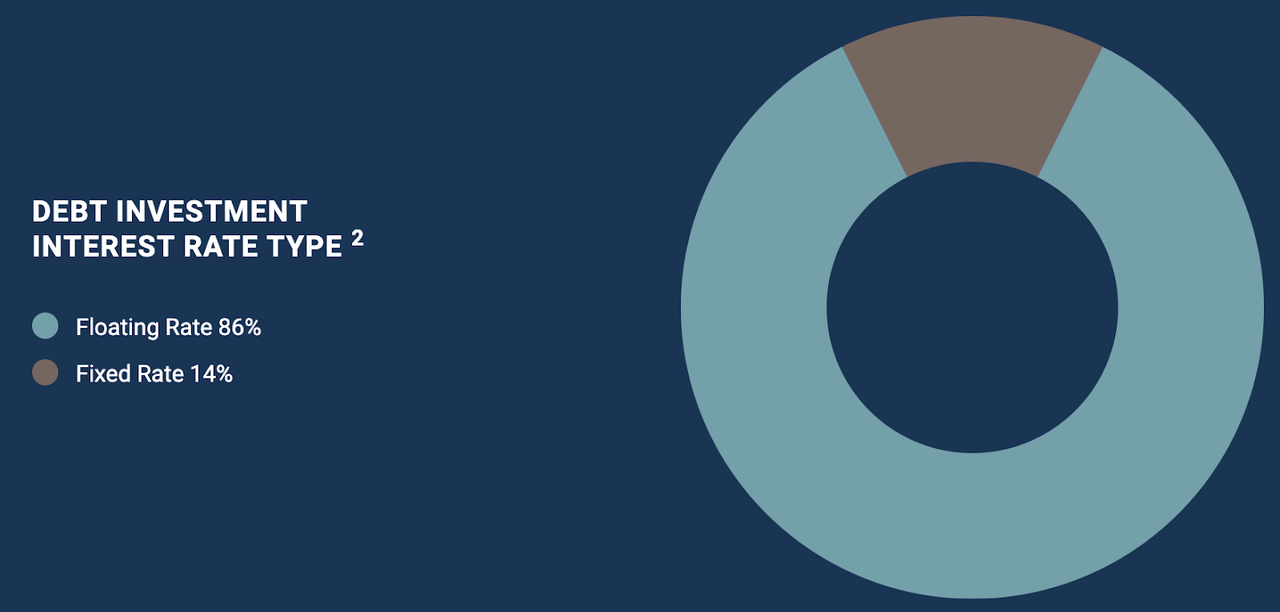

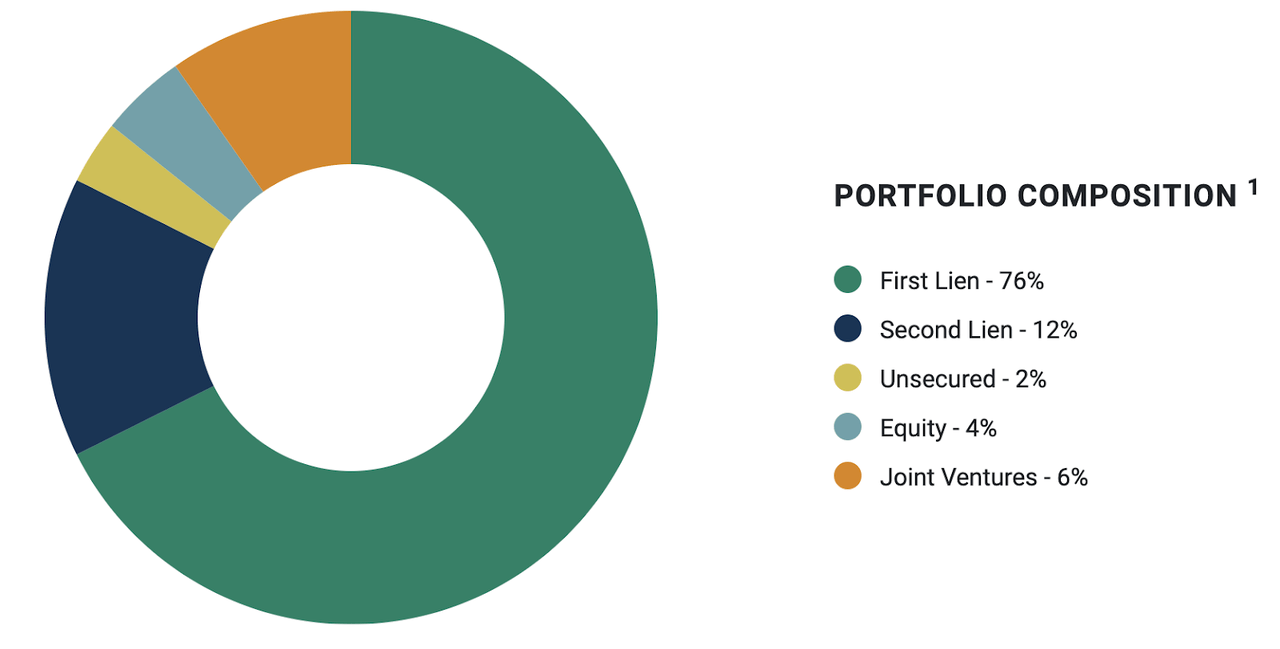

Oaktree Specialty Lending’s objective is to lend money to small to midsize businesses with unique needs. Its lending mix is pretty diversified, consisting of tech companies, specialty retail and real estate. Its debt investments are overwhelmingly (86%) floating rate. Its portfolio consists of 76% first lien debt. The diversified mix of industries and the high percentage of first lien debt are unambiguous positives. The “floating rate” thing is a positive if you think the Fed will keep hiking or keep interest rates where they are.

OCSL Industries (Oaktree Specialty Lending) OCSL fixed vs floating (Oaktree Specialty Lending)

OCSL portfolio composition (Oaktree Specialty Lending)

From the charts above, we can see that Oaktree’s portfolio is:

-

Diversified.

-

High quality.

-

Able to take advantage of interest rate hikes should more of them materialize.

It’s a great package of characteristics to begin with.

But there’s more to the story than just that.

In addition to having a diversified high yield portfolio, Oaktree is also financially sound. According to Seeking Alpha Quant, it boasts the following balance sheet metrics:

-

$3.33 billion in assets.

-

$1.826 billion in liabilities.

-

$1.509 billion in equity.

-

$1.779 billion in debt.

-

$183 million in current assets.

-

$46.9 million in current liabilities.

The current ratio, 3.90, is excellent. The higher this ratio is, the better.

The 1.17 debt to equity ratio is good for a lender. Normally, we want this ratio to be below one. However, it’s almost always astronomically high for banks, as their deposits are a “debt” and they are often about 5 to 10 times equity. So, compared to your average bank, Oaktree Specialty Lending is not very leveraged.

In addition to being financially sound, Oaktree Specialty Lending is also profitable, boasting the following profit metrics:

-

A 100% gross margin.

-

A 76% EBIT margin.

-

A 24% net margin.

-

A 21.35% levered free cash flow margin.

-

A 6.1% return on equity.

Overall, these are some impressive profitability figures. Between these and the balance sheet ratios, we have significant evidence that OCSL is a high quality company.

Recent Earnings

Oaktree Specialty Lending’s most recent quarter was pretty good, boasting the following metrics:

-

$1.32 in investment income per share, unchanged.

-

GAAP net investment income of $48.6 million, up 5.65%.

-

$19.58 in net asset value (“NAV”), down slightly from $19.66.

-

$251 million in new loans originated.

Overall, it was a pretty good showing. The slight miss did not change the fact that earnings were more than enough to keep the dividends being paid. As a pure dividend play, the bullish thesis on Oaktree remains intact after the Q2 release.

Valuation

Oaktree Specialty Lending has a modest valuation, trading at the following multiples:

-

8.33 times adjusted earnings.

-

16 times GAAP earnings.

-

3.9 times sales.

-

1x book value.

Overall, not an unreasonable valuation based on multiples. Additionally, as I wrote in a recent Tweet, the stock comes out with a $22 price target in a dividend discount model that uses a 6% risk premium and assumes no growth. That’s 10% upside.

The Big Risk

The big risk to watch out for with OCSL is dilution. As Seeking Alpha’s financials page for the stock shows, the share count has been steadily increasing over the years. With the payout ratio at 90%, more dilution could result in lower dividends if earnings don’t grow considerably.

The good news is that Oaktree Specialty Lending doesn’t even need per-share earnings growth to be worth the investment. As long as it can keep the dividend where it is now, it is worth at least $22. To my mind, that makes OCSL a very enticing high dividend play.

Read the full article here