Investment update

Following my last publication on Ormat Technologies (NYSE:ORA) the stock is +14% but still rangebound. The report, titled “High earnings not as attractive compared to capital required to grow”, illustrated several economic headwinds, namely:

- It is reinvesting heavily for growth, but the company’s economic value is clamped due to its capital hungry nature and low returns on business capital.

- Had added ~100MW of capacity in 2024 by that time.

- The market expected a 31% YoY growth in earnings and 28% decrease in EBIT from FY’22 numbers with consensus eyeing 13% sales growth in both FY’23 and FY’24.

Given ORA’s strong points I believe it has resilience but the investment debate is marred with challenges, from valuation to comparable economics. Analyzing the cash ORA could reasonably produce out to FY’28E leads me to believe the stock remains a hold.

Alas, I remain hold on ORA due to 1) fundamentals [compressed ROICs, capital hungry model, growth not translating to value], 2) forward estimates [I am ~50bps behind consensus at the top-line to FY’26E], and 3) valuations suggesting limited scope for a capital accumulation rate above what can be achieved elsewhere with investments of similarly priced risk. Net-net, reiterate hold.

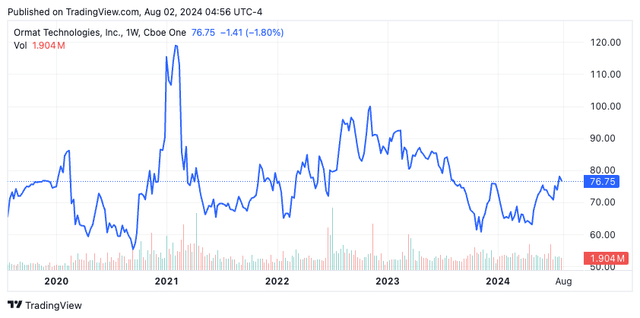

Figure 1.

Tradingview

Run-down leading into Q2 ’24

ORA is set to file Q2 ’24 earnings later this month (August 2024) and there are a few points to consider leading into this. Firstly, going to its Q1 numbers, we can glean multiple insights:

- Sales were +21% to $224mm with divisional growth in all 3 operating lines. It pulled this to ~$79mm gross (+3.6%) and adj. EBITDA of ~$141mm (+14.4%). Critically, electricity was +12% to $191mm and its ‘products’ business was up ~147% to $25mm. This could be one to watch in Q2 ’24 in my view, given the ramp it is on – management said it had ~$130mm backlog in the segment and of Q1. You have that + the ~65% growth in energy storage revenue. Again, I’d be checking these figures in the upcoming earnings report.

- It added ~10MW of capacity during the quarter bringing ’24 total to 110MW which was backed by ~+800bps growth in electricity generation. It’s highly relevant that management commented on the “increase in the demand for electricity and energy storage segments” it continues to observe – this reaffirming growth targets of ~2.1–3.3GW in total portfolio capacity by FY’26E.

- To this effect, it has completed its 20MW/hr facility in East Flemington and had 6 storage projects in development in Q1. This will add ~335MW to total storage. Keynote to watch in Q2 – management said it expects its Bottleneck facility (California) of ~320MW to begin operating by Q2. So I’d be checking where this is up to.

- Management also projected FY’24 revenues of $910mm at the upper end (~+8%) with ~$35-$45mm in energy storage. It looks to adj. EBITDA of ~$545mm on this at the upper estimate. The upside risk is management revises these higher – this could warrant investors paying the currently high multiples leading into the update.

In addition to the recent developments, the following factors are helpful in framing the picture for Q2 in my estimation:

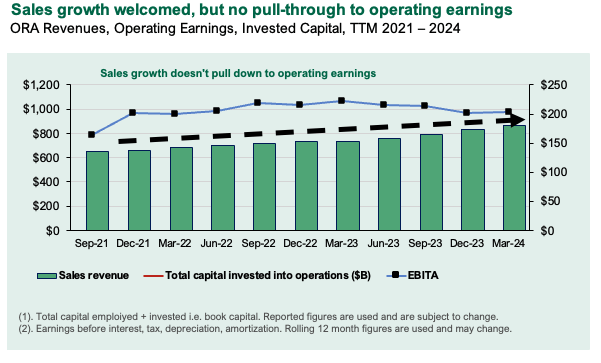

- Sales growth is persistent but doesn’t pull down to operating earnings – I’m surprised to see this given the sector enjoys high margins, but 3yr pre-tax growth is -2% and 5yr is -3.4%. In fact, 10yr sales CAGR of 4.5% produces ~2.4% compounding growth in operating earnings. My view is this is a risk moving forward, as the stock is priced at ~41x trailing EBIT as I write. Even outsized growth makes it difficult to work into that multiple.

Figure 3.

Company filings

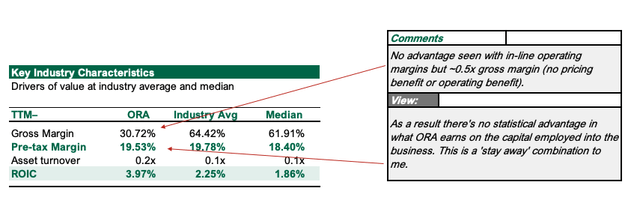

- Compared to the industry, no business advantage is seen against peers – this is illustrated with in-line operating margins at ~19% but ~0.5x the gross margin (indicating no pricing benefit or operating benefit). As a result, there’s no statistical advantage in what ORA earns on the capital employed into the business. I touched on this in my last analysis – this is a ‘stay away’ combination to me.

Figure 4.

Company filings, Seeking Alpha

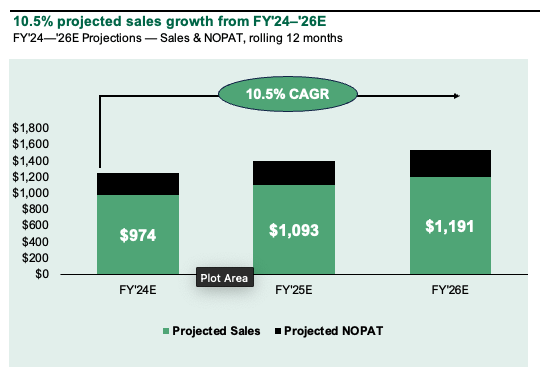

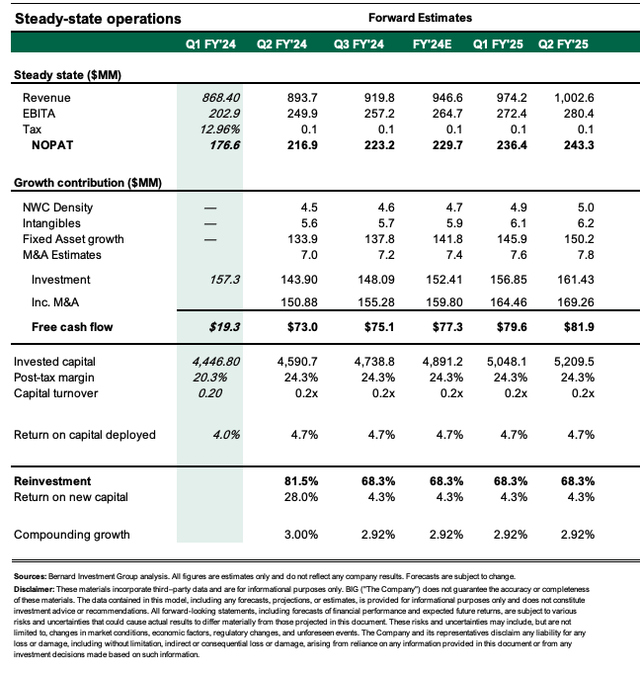

- My forward estimates from FY’24–’26E [see: Appendix 1] imply ~10.5% compounding growth in sales. This is ~50bps behind consensus estimates, but my view is the company may have difficulty in adding capacity at the same cadence in the back end of the year. Leading into its Q2 earnings, I want to see 1) if ORA is on track to this growth in ’24, 2) if there’s a chance for a revision to the upside, and 3) if not, what this means to valuations.

Figure 5.

Author’s estimates

Bar set high for valuation expansion

Whilst I’m acutely aware these businesses need their own framework of analysis, we can’t sit here and ignore basic valuation principles either. We usually employ a 12% hurdle rate against all equity evaluations but the economics of energy businesses (both ‘conventional’ and renewable) are such that business returns are relatively slack (<10% on avg.) and usually a function of fixed pricing mechanisms, offtake agreements, legislature and so forth. The most important factor (as in any highly tangible business) is a proper recovery of our underlying – including capital + return on capital.

Valuation insights

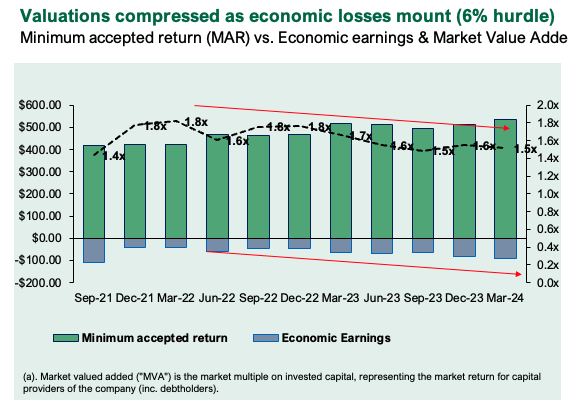

- Consequently, we use a 6-7% threshold as the economic opportunity cost for this industry. The issue is, ORA’s operating assets aren’t meeting this hurdle. The responding economic losses are deepening – with investors contracting the multiple from ~1.8x EV/IC to ~1.5x since FY’22 – despite the fact more than $942mm has been put back into the business since FY’21.

- Still, investors valued each $1 of incremental capital at ~1.8x – i.e., producing ~$1.80 in market value per $1 of investment. This appears fair based on historical numbers.

Figure 6.

Company filings, author calculations

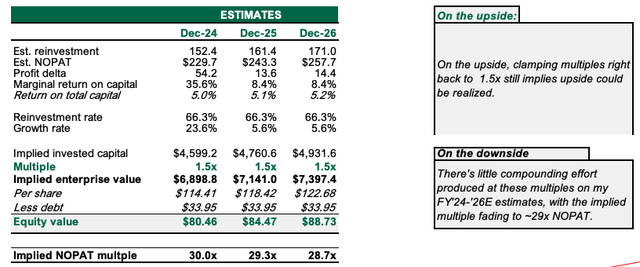

- On the upside, clamping multiples right back to 1.5x still implies a small upside could be realized. My FY’24 numbers [see: Appendix 1] imply the business is worth ~$80/share today at 1.5x EV/IC, roughly where it trades today. But it all relies on the multiple, vs. fundamentals. On the downside, there’s little compounding effort produced at these multiples on my FY’24-’26E estimates, with the implied multiple fading to ~29x NOPAT. Consequently, my view is ORA is worth ~$80/share today.

Figure 7.

Author’s estimates

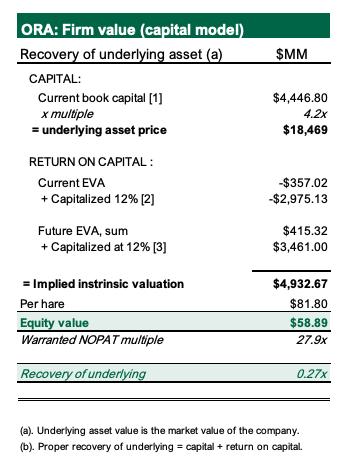

- More critically, on an economically weighted basis, i.e., observing the potential cash that could be stripped out of the business by a private owner above a 5% hurdle (compressed here to represent the starting yields on most investment-grade corporates of similar risk) implies we’d receive ~0.3x recovery of our underlying (including a loss of capital). This doesn’t stack up and supports a reiterated hold rating leading into its Q2 numbers.

Figure 8.

Author’s estimates

Risks to the thesis

The upside risks to the thesis are if ORA comes in with financials well above expectations. That means >11% annualized sales growth, and ROICs >6%. Momentum is currently low leading into the event (including fundamental momentum) which means it could surprise to the upside. Statistically speaking, this could be beneficial as expectations may be low. This is countered by the high valuations, however. If ORA comes in with this sort of numbers, it may justify a ‘higher for longer’ valuation multiple and get the stock above $85/share. I give this scenario a 25% probability weighting.

Investors must realize these risks in full before proceeding any further.

In Short

Alas, leading into Q2, investors should pay close attention to 1) annualized sales growth of ~11%, 2) returns on all invested capital >5% [reflecting management’s capital allocation decisions], and 3) any revisions to sales growth to the upside. My view is there is a probability for ORA to surprise to the upside, which is good as price momentum is currently low. But valuations offset this and dampen prospective investment returns – investors must continue to pay >38x NOPAT to see it trade reasonably higher from here. Net-net, reiterate hold.

Appendix 1.

Author

Read the full article here