Ovintiv Inc. (NYSE:OVV) recently raised its full-year production guidance in 2024, and showed an impressive business growth in the last decade. From asset growth to FCF growth and debt reduction, everything seems to indicate that OVV has proven expertise in the industry. I would be expecting new well improvement from multi-frac technology Simulfrac and Trimulfrac, which may have a beneficial effect on free cash flow growth. Besides, recent announcements about reductions in upstream operating and administrative expenses could also accelerate FCF growth in the future. Considering the guidance given for 2024 and previous operations, I think that OVV appears quite undervalued. My DCF model implied a valuation of close to $73 per share, which is not far from the target price given by other analysts.

Ovintiv

Headquartered in Denver, Colorado, Ovintiv conducts exploration, development, and production of oil, NGLs, and natural gas.

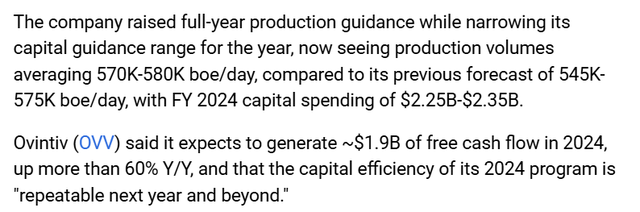

The company’s flagship product is oil, which represented quarterly revenue of $1.19 billion only in the United States, followed by $176 million from the sale of NGLs. In the last quarter, OVV also increased its production guidance, which could bring demand for the stock in 2024.

Source: Press Release

OVV also reports some level of geographic diversification. According to the last quarterly report, USA operations were responsible for $2.9 billion in total sales for the six months ended June 30, 2024. OVV also reported $951 million in revenue in Canada. Market optimization was responsible for the total amount of revenue worth $806 million.

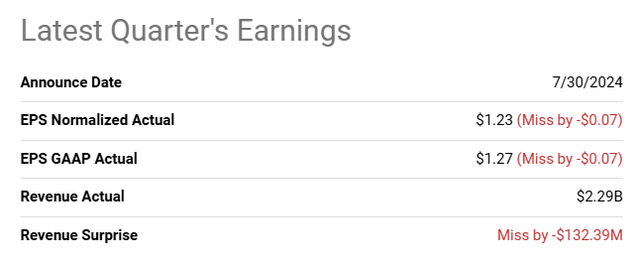

The company’s quarterly earnings were lower than expected. EPS GAAP stood at $1.27, and quarterly revenue was close to $2.29 billion.

Source: Seeking Alpha

I did not like the recent earnings, but OVV reported beneficial long-term performance for the last ten years. In addition, EPS is expected to grow close to 18% in 2025.

Source: Seeking Alpha

Assets Growth, Net PP&E Growth, And Equity Growth

In my view, the company has proven to be delivering value to shareholders since 2015. The total amount of assets increased from $15 billion in 2015 to about $19 billion in 2024. Additionally, the total amount of liabilities did not increase much in the last decade, and the total amount of equity multiplied by 1.6. Besides, management successfully increased its net PP&E from $9 billion in 2015 to around $14.8 billion in 2024. In my view, as soon as more investors have a look at the numbers reported by OVV, we may see demand for the stock.

Source: Seeking Alpha

Unlevered FCF Growth Increase, And Cheap

If we look at the company’s EBITDA and FCF figures from 2015, the numbers look quite ideal. EBITDA increased from $1.7 billion in 2015 to $4.8 billion in 2023, and FCF turned remained positive in 2018, and stood at close to $1.1 billion in 2023, and $655 million in 2024. Further increase in the total EBITDA and FCF reported will most likely lead to stock price increases.

Source: Seeking Alpha

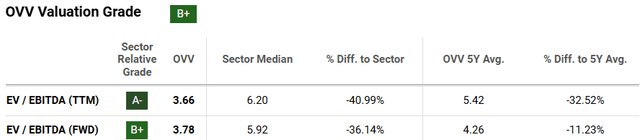

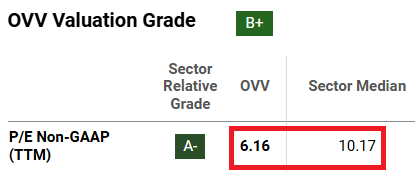

OVV appears to be trading at close to 3x-4x FWD EBITDA, which I do not think is fair given the most recent EBITDA growth in the last 9 years. Competitors trade at more than 6x FWD EBITDA. OVV is also trading at close to 6x TTM earnings. Competitors trade at close to 10x TTM earnings. In sum, OVV appears significantly undervalued as compared to competitors.

Source: Seeking Alpha Source: Seeking Alpha

Investors may say that the company’s net debt is not small, which is true. However, OVV recently reported a significant decrease in the total amount of net debt. In 2015, the net debt/EBITDA ratio stood at 6.7x. Right now, the net debt/EBITDA ratio is significantly lower. Yes, the company is making a lot of efforts. As soon as more investors review the company’s financial shape, I would expect an increase in the total equity valuation.

Source: Seeking Alpha

If we look at the company’s tangible book value per share, there is also significant undervaluation. The current tangible book value per share is close to $29. If we buy today, we are paying close to 1.6x the tangible book value with the proven reserves owned by OVV, and we get a company that reports growing EBITDA and FCF.

Source: Seeking Alpha

The Company Is Buying Its Own Shares, And Review Of The Debt

In my view, directors know better than outsiders the real value of the company. Hence, when companies buy their own shares, I think that companies are close to fair value.

In this case, in the last quarterly report, the company acquired a total of 3.6 million shares for a total consideration of $184 million. Thus, the company bought shares at an average of $51 per share. It means that if we buy today, we are a buying at a price mark that is not far from the company’s buying point.

During the three and six months ended June 30, 2024, the Company purchased approximately 3.6 million shares and 9.0 million shares respectively, for total consideration of approximately $184 million and $434 million respectively.

I took some time to review the company’s total outstanding debt and the interest rate being paid. The company’s unsecured notes include interest between 5% and 8%, and most notes mature from 2025 to 2053. Given the maturity and the interest being paid, I assumed that a cost of capital close to 6.5% would make sense in this case.

- U.S. Unsecured Notes 5.65% due May 15, 2025

- 5.375% due January 1, 2026

- 5.65% due May 15, 2028

- 8.125% due September 15, 2030

- 7.20% due November 1, 2031

- 7.375% due November 1, 2031

- 6.25% due July 15, 2033

- 6.50% due August 15, 2034

- 6.625% due August 15, 2037

- 6.50% due February 1, 2038

- 5.15% due November 15, 2041

- 7.10% due July 15, 2053

DCF Model: $73

In my view, we could expect significant inorganic growth coming from property purchases in Permian with oil and liquids-rich potential. For the six months ended June 30, 2024, the company noted acquisitions worth $195 million. I think that we may see an improvement in the total amount of proven reserves as a result of these acquisitions. As a result, the book value per share may increase, and the expected free cash flow could also increase. In 2023, the company acquired a large amount of equity interest with a combination of cash and equity. The total amount of cash paid was $3.2 billion, which was larger than the total amount of shares issued. Given the size of this acquisition, in my discounted cash flow model, I assumed that we will most likely see new acquisitions in the coming years.

On June 12, 2023, Ovintiv completed a business combination to purchase all of the outstanding equity interests in seven Delaware limited liability companies (“Permian LLCs”) pursuant to the purchase agreement with Black Swan Oil & Gas, LLC, PetroLegacy II Holdings, LLC, Piedra Energy III Holdings, LLC and Piedra Energy IV Holdings, LLC, which were portfolio companies of funds managed by EnCap Investments L.P. (“EnCap”). The Company paid aggregate cash consideration of approximately $3.2 billion and issued approximately 31.8 million shares of Ovintiv common stock, representing a value of approximately $1.2 billion. Source: 10-Q

The company’s outlook for the year 2024 included a planned reduction in upstream operating and administrative expenses. I assumed that this strategy that includes lower expenditures will most likely continue from 2025 to 2029. As a result, investors could enjoy an overall increase in FCF. In this regard, the following lines from the most recent quarterly report appear quite relevant.

The Company will continue to exercise discretion and discipline, and intends to optimize capital allocation through the remainder of 2024 as the commodity price environment evolves. Ovintiv pursues innovative ways to maximize cash flows and to reduce upstream operating and administrative expenses. Source: 10-Q

In addition, I assumed that the company’s efforts to improve well performance and new multi-well pads could maximize returns and resource recovery in the coming years. Besides, with new multi-frac technology Simulfrac and Trimulfrac, I think that we could see an improvement in the operating margin and FCF margins.

My free cash flow expectations are pretty much in line with the FCF reported in the past. I expect an upward trend from $1 billion in 2024 to close to $2.9 billion in 2028 and $3.2 billion in 2029. In addition, with a WACC of 6.5% and EV/2029 FCF of 7x, I obtained a total valuation of $26 billion, and with net debt of $6.9 billion, the implied valuation would stand at $73 per share.

Source: Seeking Alpha

- NPV: $11,166.34 million

- NPV of TV: $15,636.45 million

- Total Value: $26,802.79 million

- Net Debt: $6,984.0 million

- Equity: $19’818 million

- Shares: 270.10 million

- Target Price: $73

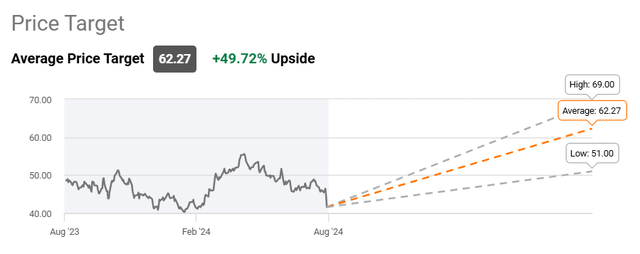

Other analysts offered an average price target of $62 per share. I think that there is optimism in the market.

Source: Seeking Alpha

Risks

I see a significant number of risks coming from changes in the oil price and the energy markets in general. If the oil price decreases, I would be expecting a decrease in the total net sales reported by OVV. As a result, free cash flow expectations could decline, which may lead to lower target prices. In sum, we could see decreases in the stock price.

Prices are market driven and fluctuate due to factors beyond the Company’s control, such as supply and demand, seasonality and geopolitical and economic factors. The Company’s realized prices generally reflect WTI, NYMEX, Edmonton Condensate and AECO benchmark prices, as well as other downstream benchmarks, including Houston and Dawn. Source: 10-Q

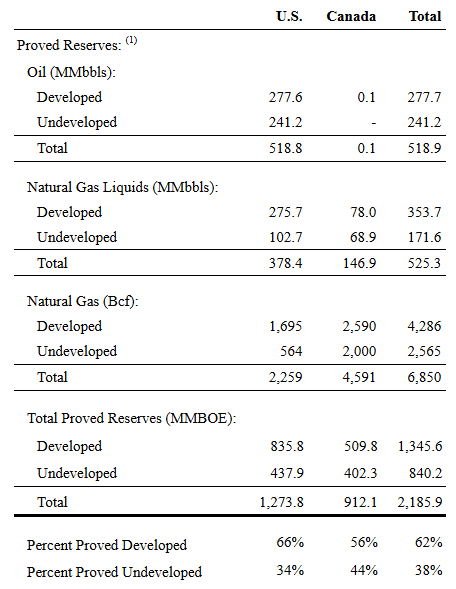

In the last 10-k, the company reported the most recent information we have about the proven reserves owned by OVV. Reservoir engineers could calculate the number of reserves wrong. They may overestimate future production of crude oil.

Source: 10-k

In the worst-case scenario, future production may be lower than expected, which may lead to lower net sales growth and FCF than expected. If analysts see that the company is reducing its total proven reserves, they may also lower expectations about future FCF growth. As a result, shareholders may sell shares, and the stock price could fall.

The company appears to be making a lot of efforts to reduce the total amount of emissions. In 2024, the company published a new 2023 Sustainability Report, which included information about the 40 percent reduction in the Scope 1&2 GHG emissions from 2019 levels. In my view, if the company does not reach its reduction target of 50 percent by 2030, certain market participants may sell their stakes in the company. OVV may also suffer from changes in environmental regulations or increases in the taxes related to the oil and gas industry.

In May 2024, Ovintiv published its 2023 Sustainability Report. The report highlights the Company’s 2023 environmental, social and governance results, and its progress in emissions intensity reductions with the goal to meet its Scope 1&2 GHG emissions target by 2030. As at the end of 2023, the Company had achieved a greater than 40 percent reduction in the Scope 1&2 GHG emissions intensity from 2019 levels and is on track to meet its emissions intensity reduction target of 50 percent by 2030 measured against the 2019 baseline. Source: 10-Q

Conclusion

Exhibiting geographic diversification, OVV delivered impressive business growth in the last decade including asset growth, debt reduction, and FCF growth. Besides, I think that the new multi-frac technology Simulfrac and Trimulfrac could improve well performance and enhance FCF margin growth. Besides, recent news about reductions in upstream operating and administrative expenses delivered for the year 2024 could improve future FCF growth. Putting everything together, I do not really understand the current valuation. The company is trading quite undervalued at the current EV/EBITDA and EV/FCF as compared to other competitors. My discounted cash flow model also included an implied fair price close to $73 per share, which is significantly higher than the current market price.

Read the full article here