Co-authored with “Hidden Opportunities”

Utilities are among the most boring companies among industry classes. There is nothing meme-worthy in their business, they won’t be launching the next must-have product in September, and you won’t see a swarm of influencers on TikTok advertise their services. But there is one thing they do very well, which makes us very interested in their stock – keeping shareholders happy with the regular distribution of profits in the form of dividends.

Utility stocks are often considered bond proxies because they offer investors stable and consistent dividends and lower price volatility relative to the overall equity markets. The preferred securities issued by utilities take the safety several notches higher by offering a highly protected and even larger income stream than the common stock. These securities are seldom discounted, but thanks to these higher interest rates, we see excellent bargains to buy and hold long-term and play defense against recession fears.

Today we will discuss high-yielding preferred shares from three leading North American utility companies.

Let’s dive in!

Pick #1, SCE Preferreds – Yields Up to 6.7%

Southern California Edison (SCE in this article) is one of the largest electric utilities in the United States, serving ~15 million people in a 50,000 sq. mile area of Central, Coastal, and Southern California. SCE is an Edison International (EIX) subsidiary that has provided the region’s electric utility service for 136 years.

In recent quarters, SCE has been making upgrades to increase the safety and reliability of its assets. As of Q2 2023, the company has completed nearly 5,000 miles of covered conductor and estimates it has reduced the probability of losses from catastrophic wildfires by 85%. This has been a substantial effort in the making since 2018. Source

Investor Presentation

EIX has been an excellent dividend steward with 19 years of annual payment raises. With management providing FY 2023 guidance EPS in the range of $4.55 to $4.85, the company’s current common dividend remains comfortable at a 62.7% payout ratio (at the midpoint of the guidance range). EIX management targets a dividend payout of 45–55% of SCE core earnings over the long term, which remains achievable through the 5%-7% CAGR EPS growth the company forecasts through 2025. Common shareholders can expect continued dividend growth from this well-oiled income machine for the foreseeable future.

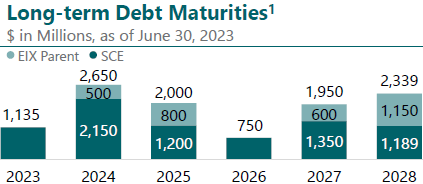

EIX maintains a manageable debt maturity schedule and has over $3.7 billion in liquidity to tackle upcoming maturities. SCE’s long-term issuer rating was recently upgraded to Baa1 by Moody’s.

EIX Investor Presentation

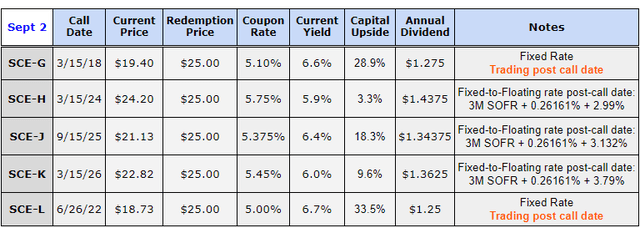

SCE has five classes of cumulative preference shares that pay qualified dividends. These carry Investment-Grade ratings from Moody’s and Fitch and are trading at attractive discounts to par, sporting big qualified yields.

-

SCE Trust II, 5.10% Cumulative Redeemable Fixed-Rate Trust Preference (SCE.PR.G)

-

SCE Trust III, 5.75% Cumulative Redeemable Fixed-to-Floating Rate Trust Preference (SCE.PR.H)

-

SCE Trust IV, 5.375% Cumulative Redeemable Fixed-to-Floating Rate Trust Preference (SCE.PR.J)

-

SCE Trust V, 5.45% Cumulative Redeemable Fixed-to-Floating Rate Trust Preference (SCE.PR.K)

-

SCE Trust VI, 5.00% Cumulative Redeemable Fixed-Rate Trust Preference (SCE.PR.L)

Author’s Calculations

YTD, Edison generated $664 million in net income after paying $753 million in interest expenses and $110 million on EIX and SCE preferred dividends. This Net Income adequately supported the $555 million spent on common dividends. We see EIX continue to grow dividends, which is excellent news for the cumulative preferred investors.

Currently, SCE-G and SCE-L present similarly priced fixed-rate opportunities, with a 6.7% qualified yield and ~35% upside to par. Both are trading post their call dates and offer attractive income at discounted prices.

In SCE, we see a stable business catering to California, where EV adoption is the highest in the country. Continued growth in this trend requires the electric grid to be reliable and durable, positioning SCE to be a continued beneficiary of several federal and state funds to expand its asset base to cater to the growing demand. SCE preferreds present attractive income opportunities.

Pick #2, NI Preferred – 6.5% Yield

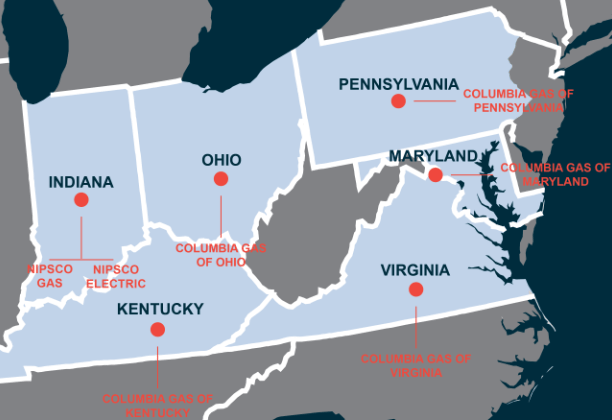

NiSource, Inc. (NI) is a leading natural gas and electric utility company serving 4 million customers across six states in the U.S. NI serves the residents of Indiana, Kentucky, Maryland, Ohio, Pennsylvania, and Virginia through its operating subsidiaries – Columbia Gas and NIPSCO.

The company operates a 100% regulated oil and gas utility, providing price stability, greater geographic control, and long-term certainty to its operations. NI has a long and well-established history in these regulatory environments, providing inflation protection, solid cash flow consistency, and sustainable growth opportunities for the business. Source

NiSource Website

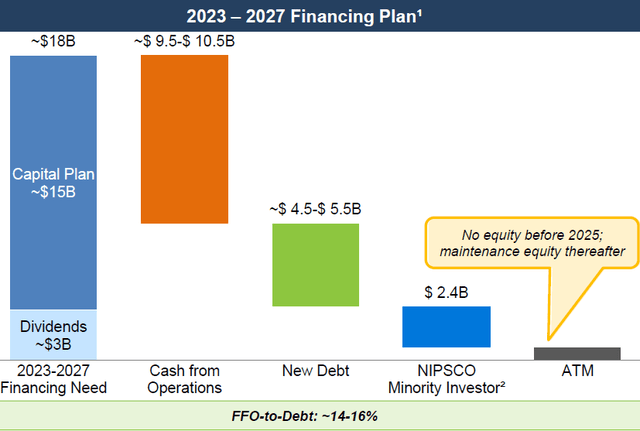

NiSource revealed last year that it is putting into action a 2040 net zero goal to place itself among the industry leaders and improve the safety and sustainability of its operations, phase out coal by 2028, and introduce more renewables into the mix. Below is the financing plan for the next four years. As a result, the company projects $30 billion in planned Long-Term Infrastructure Investments over the next ten years, with $15 billion scheduled through 2027. Source

NiSource Investor Presentation

Aside from the cash from operations and $2.4 billion infusion from BlackRock (to acquire a minority 19.8% equity stake in NIPSCO to invest in Indiana and into energy transition as a long-term partner to NiSource), the company plans to raise $4.5 – $5.5 billion in new debt. NiSource maintains an investment-grade BBB rating. The company’s debt level at the end of Q2 2023 was $12.6 billion, of which $11 billion was long-term debt with a weighted average maturity of 12 years at a weighted average interest rate of 3.9%. The company has net available liquidity of $1.8 billion, consisting of cash and available capacity under the credit facility.

NI has raised common stock dividends annually since 2015. The company’s $0.25/share common dividend comes at a modest 63% payout ratio based on the EPS guidance for the fiscal year. This is well within the company’s 60%-70% target dividend payout ratio. NI estimates a 6-8% annual EPS growth, indicating healthy room for continued dividend growth.

NiSource has one public preferred security, which forms the gist of our discussion today. NI-B is redeemable on March 15, 2024, or any subsequent fifth anniversary of this call date at the $25 liquidation preference.

NI-B will become redeemable in 7 months, and there are three more dividend payments until then (amounting to $1.218/share). We believe NI-B will not be redeemed in the near future due to the capital allocation priorities outlined by the company. As such, this preferred will experience a rate-reset equaling the 5-Yr Treasury + 3.632%. In this elevated interest rate environment of +4% yields on the 5-Yr Treasury, NI-B will secure a +7.6% qualified yield, making it a tremendous income source to lock into for five years.

-

6.50% Rate-Reset Cumulative Redeemable Perpetual Preferred Stock (NI.PR.B)

Author’s Calculations

It must be noted that NI-B can be redeemed by the company only every fifth anniversary of the call date.

NI spends $55 million annually on preferred dividends. This is a tiny fraction compared to the $1.4 billion net cash from operating activities, $361 million annual interest expense, and $381 million common stock dividends for FY 2022. Even with a 17% increase in preferred dividend spend due to the rate-reset next year, we see adequate coverage for shareholders’ income.

NI is a regulated utility provider with stable operations and predictable cash flows. We believe its preferred will remain trading post-call date due to other capital projects being pursued by the company. As such, NI-B presents an attractive fixed-income opportunity to take advantage of elevated interest rates and lock in a large qualified yield for the foreseeable future.

Conclusion

Utilities are essential services that people rely on for their daily lives. They provide basic necessities like water, heat, and electricity, which are crucial for health and well-being. Even during a recession, people need these services to maintain their quality of life.

Due to the inelastic nature of the demand, utilities tend to perform well during recessions and economic downturns. Most companies in this industry pay dividends to shareholders, and their regulated operations provide excellent protection for their profitability. As such, they continue paying and raising dividends despite rising costs.

In this report, we discuss two safer ways to dip into the moat and profitability of utilities to generate regular paychecks. With up to 6.7% yields and sizeable capital upside, these can help you sleep well at night through recessions and other economic pressures.

Read the full article here