Who would have expected that a 40-year-old company that produces powertrain products and solutions would have beaten the S&P 500 return by a multiple of more than ten times with a 260% return in the last year? Yet even at the elevated price that Power Solutions International (OTCPK:PSIX) stock trades for today, it is highly undervalued by the market at just 6x forward earnings.

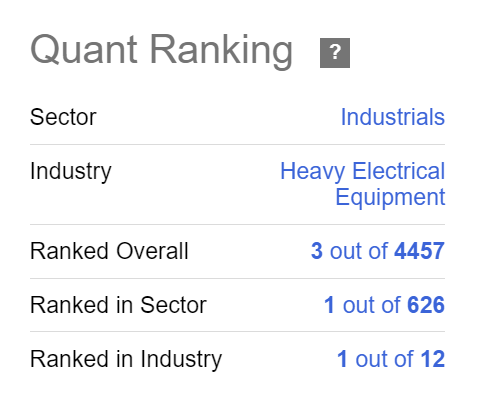

One thing that really caught my eye when I discovered the massive price growth of PSIX, especially in the past two months, is that the SA Quant system (which has proven reliable to pick top growth stocks), rates PSIX #3 overall out of 4,457 total stocks analyzed and #1 out of 626 in the Industrials sector.

Seeking Alpha

When I began to do further research, I discovered that PSIX has turned the corner on profitability in 2024 for the first time since 2020 as noted in the first quarter earnings report announced May 7, 2024.

Dino Xykis, Chief Executive Officer and Chief Technical Officer, commented, “Despite headwinds we experienced in the first quarter 2024, such as supply chain challenges from UFLPA (Uyghur Forced Labor Prevention Act) and demand weakness on some products, the company managed to achieve profitability by prioritizing margin enhancement and efficient management of working capital. We expect sales will improve for the remaining year, driven by strong demand for our power systems products. We are also extremely pleased that we restored positive shareholder equity in the quarter, for the first time since 2020. We also paid down debt $5.0 million in the first quarter of 2024, and an additional $5.0 million in April 2024.”

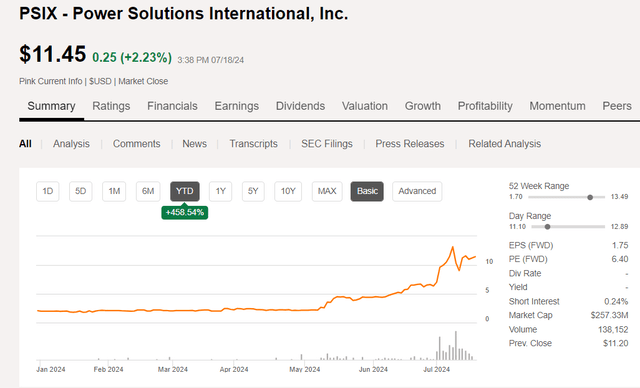

Looking at a YTD price chart, the inflection point from the May earnings report shows how the stock price increased from around $2 per share where it had traded up until the Q1 report came out and then shot higher, now up over 450% on a YTD basis.

Seeking Alpha

Earnings Growth is Fueling Profitability

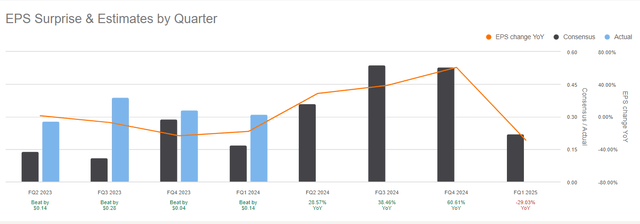

Even though the market has begun to reward the company for its return to profitability, the earnings trend indicates that growth is likely to continue with earnings beats in the last four quarters in a row and future earnings estimates going even higher each quarter through the end of 2024 as shown in the EPS Estimates and Surprises page.

Seeking Alpha

The earnings trend and strong Q1 results, which also included improvement in gross margins, an increase in operating cash flows, and reduction of debt during the quarter all contributed to the big share price increase as investors recognized how undervalued the stock had become.

From the company Q1 press release:

- Net Income increased by 91%, EPS were $0.31, an increase of $0.15 for the Quarter,

- Gross Margin 27.0%, an increase of 6.9% for the Quarter,

- Operating Cash Flows were $15.6 million, an increase of $10.6 million for the Quarter,

- Debt decreased $5.0 million for the Quarter,

- Shareholder Equity restored positive $3.2 million for the Quarter.

Company Overview

Power Solutions International (“PSI”) was founded in 1985 and is headquartered in Wood Dale, Illinois. The company designs, engineers, manufactures and sells engines and power equipment in the US and internationally. Since 2017 they have been a global partner with the Chinese company, Weichai.

Since 2017, PSI has been a valued strategic investment and collaboration partner to Weichai America Corp., a wholly-owned subsidiary of Weichai Power Co., Ltd., the largest car parts and power system conglomerate in China. PSI can access Weichai’s manufacturing facilities and supply chain network, and both companies share best practices in engine research and development as well as manufacturing, procurement and distribution.

The company’s vision statement aims to “envision a future where the company’s engines inspire change.” According to the company website, they have sold more than 1.5 million engines and had revenues of $459M in 2023. The company market cap today is only $257M and the average trading volume is around 60,000 shares per day. The company offers a diversity of power solutions to multiple industries as explained on the website:

PSI’s engine portfolio spans displacements ranging from .97 liter to 88 liters. Powered by advanced controls, our engines are engineered to operate efficiently across a wide array of fuels including natural gas, propane, gasoline, diesel, and biofuels.

We supply engine and other solutions for various stationary and mobile power generation applications including standby, prime, demand response, microgrid, and CHP (co-generation power). Additionally, our engines serve a myriad of industrial needs encompassing forklifts, agricultural and turf machinery, industrial sweepers, aerial lifts, irrigation pumps, ground support and construction equipment.

The company offers extensive manufacturing capabilities in support of their product line.

PSI website

The company currently owns and operates six facilities, 3 in Illinois, 1 in Michigan, and 2 in Wisconsin (the second facility was officially opened on Aril 22, 2024) with a total of 800,000+ square feet of manufacturing space. In addition, the partnership with Weichai gives them a global presence with more than 500 service centers in 55 countries.

The solutions offered by PSI serve multiple end markets including Power Systems, Transportation, Industrial, and New Energy.

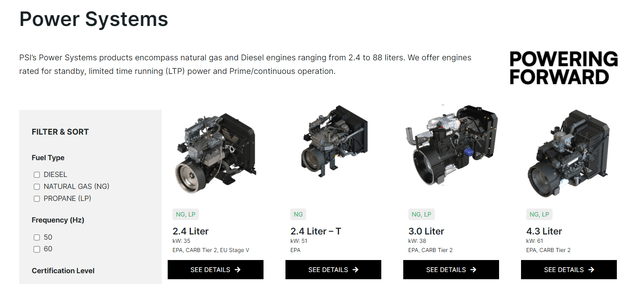

Power Systems

For heavy-duty, mission critical power systems such as electricity generation, PSI offers multiple engines powered by gas, propane, and diesel. The engines offered are rated for standby, LTP (limited time running power), and prime/continuous operation. The end markets for these solutions include oil and gas, telecom, data centers, healthcare, utilities and water treatment, and office/commercial.

PSI website

The solutions offered can include complete packages such as standard and custom enclosures, emergency standby and prime power systems capable of delivering up to 5 MW, and microgrids and oil field power solutions such as wellhead gas-powered solutions.

Industrial Engines

As an OEM supplier, industrial engine solutions support multiple fuel types and offer durable, fuel-efficient solutions for their customers in a variety of end markets.

PSI website

New Energy Solutions

In support of the electrification of everything, PSI offers solutions that provide one-stop integration for customers on the electrification journey.

We offer configurable solutions to the energy, industrial and transportation sectors including low-voltage lithium-ion batteries available between 24 and 120 volts and high-voltage systems in the 500+ volt range. Our solutions can be fully configured to the needs of our customers within their desired system voltage and power storage.

Lithium-ion batteries can be paired with PSI’s internal combustion gasoline and alternative fuel engines within hybrid drivetrain systems or can be used within full electric architectures including Energy Storage Systems which can be utilized to store energy for standby power and other uses. We also offer training and support on usage of these products to our customers.

One example of a recent innovation from PSI was the successful run of a new lithium-ion powered electric motor.

PSI continues to reach milestones in its effort to offer customers an alternative to traditional gas-powered engines. Our engineering team recently successfully demonstrated PSI’s new Lithium-Ion Power Unit – which features an electric motor powered by a Lithium-Ion battery – in a woodchipper.

Through their partnership with Weichai, PSI is able to leverage strategic partnerships with other specialized providers of new energy solutions.

PSI website

Transportation Solutions

PSI also offers a variety of flexible, fuel-efficient solutions to the transportation sector.

PSI’s customers in the transportation sector require versatile, fuel-efficient engines that can still provide the power they need to go from Point A to Point B. Our engines run seamlessly on a diverse array of fuels, such as gasoline, propane (LPG), and compressed natural gas (CNG). This flexibility empowers our customers to select the fuel option that aligns perfectly with their application.Our purpose-built, emissions certified 6.0- and 8.8-liter engines are designed to deliver unparalleled power and performance.

PSI website

In addition, PSI partners with specialized technology providers to deliver clean, efficient power options to the transportation sector.

PSI website

PSIX Stock is Rebounding Due to Data Center Demand

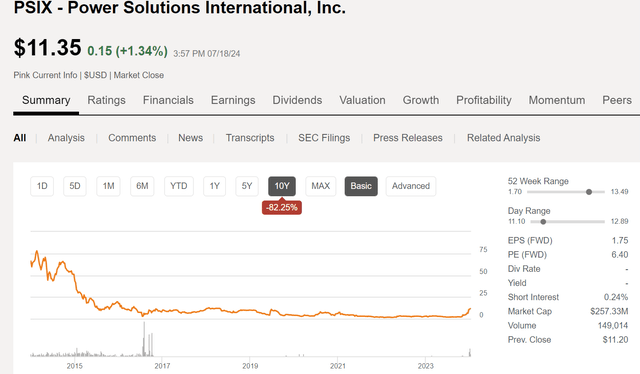

Looking at a 10-year price chart one might start to wonder what happened to cause the stock price to drop from a high of about $80 per share back in 2014 to penny stock territory up until May of this year. For one thing, the stock was delisted from the Nasdaq exchange back in 2017 due to non-compliance and now trades as an over the counter “pink sheet” stock.

Seeking Alpha

In March of this year the company reported mixed results for Q4 and the full 2023 fiscal year (emphasis added).

Sales for the fourth quarter of 2023 were $104.8 million, a decrease of $32.3 million, or 24%, compared to the fourth quarter of 2022, as a result of lower sales of $29.5 million and $16.8 million within the industrial and transportation end markets, respectively, partially offset by an increase of $14.0 million in the power systems end market. Decreased industrial end market sales are primarily due to decreases in demand for products used within the material handling and arbor care markets, as well as being directly affected by the enforcement of the Uyghur Forced Labor Prevention Act (“UFLPA”) which limited the Company’s ability to import certain raw materials at the end of 2023.

Net income in the fourth quarter of 2023 was $8.4 million, or $0.36 per share, compared to net income of $9.3 million, or $0.40 per share for the fourth quarter of 2022. Adjusted net income was $7.5 million, or Adjusted income per share of $0.34 in the fourth quarter of 2023, compared to Adjusted net income of $10.1 million, or Adjusted income per share of $0.44 for the fourth quarter of 2022. Adjusted earnings before interest, taxes, depreciation and amortization (“EBITDA”) was $12.9 million compared to Adjusted EBITDA of $16.3 million in the fourth quarter last year.

However, the company made significant progress in paying down debt in 2023 and offered an optimistic outlook for 2024 due to strong growth in the Power Systems segment.

The Company’s total debt was approximately $145.2 million at December 31, 2023, while cash and cash equivalents were approximately $22.8 million. This compares to total debt of approximately $211.0 million and cash and cash equivalents of approximately $24.3 million at December 31, 2022.

And by the time of the Q1 2024 report, the debt had been further reduced and cash on hand increased from the previous quarter.

The Company’s total debt was approximately $140.2 million at March 31, 2024, while cash and cash equivalents were approximately $33.1 million. This compares to total debt of approximately $145.2 million and cash and cash equivalents of approximately $22.8 million at December 31, 2023. Included in the Company’s total debt at March 31, 2024, were borrowings of $45.0 million under the Uncommitted Revolving Credit Agreement (“Credit Agreement”) with Standard Chartered Bank, borrowings of $25.0 million, $50.0 million, and $19.8 million respectively, under the various Shareholder Loan Agreements, with Weichai America Corp., its majority stockholder, as described in more detail in the Company’s Form 10-Q for the first quarter of 2024.

Gross profit increased by 10% YOY in Q1. Gross margins also improved by nearly 7 percentage points to 27% versus 20.2% in Q1 2023. SGA expenses decreased by 4% compared to the year ago quarter. Adjusted net income nearly doubled versus Q1 2023.

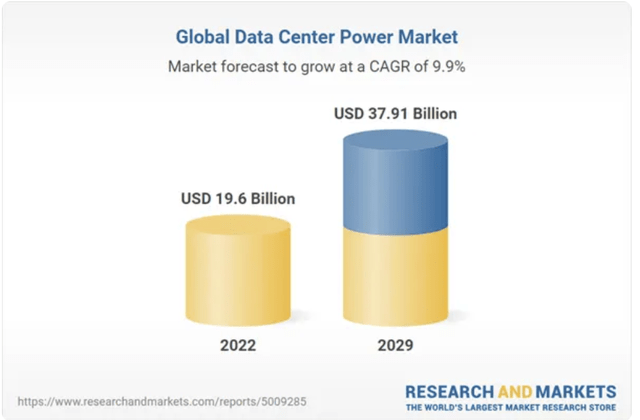

Although overall sales decreased in Q1 2024 compared to the year ago quarter, power systems end market sales increased by $17.3 million during the quarter partially offsetting the decrease in sales in transportation and industrial end markets. With increasing demand for data centers due to the AI revolution spurring spending in that market along with a resurgence in energy markets, the outlook for 2024 is encouraging with respect to further growth in the power systems end market as explained in the press release:

Higher power systems end market sales are primarily due to increased demand for products across various applications, with the largest increases attributable to products used within the packaging market such as enclosures serving the fast-growing data center market as well as oil and gas products and demand response products.

The global data center power market is forecast to grow at a CAGR of nearly 10% from 2024 to 2029 according to this recent report from Research and Markets with power distribution and uninterruptible power supply seeing the greatest increases in demand.

Research and Markets

Power distribution demand is increasing due to an increase in demand for intelligent power distribution units. Companies are moving on to intelligent power distribution units from traditional multi-socket racks with servers and network equipment. These units can measure distributed power parameters and identify environmental factors like temperature and humidity, which are contributing to their growing demand. UPS also holds a significant share in this market on account of the increasing focus of end-user enterprises on ensuring business continuity.

Much of that growth is expected to take place in North America with the US and Canada offering state of the art infrastructure attracting key players in the market.

Financials are Strong and Improving

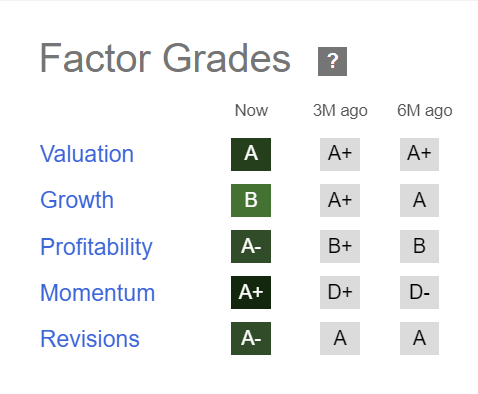

Although net sales are only expected to increase by 3% over 2023, the company has a strong balance sheet with improving financials. The SA quant factor grades confirm that PSIX gets high marks for in all categories, but with especially high grades in Valuation and Profitability.

Seeking Alpha

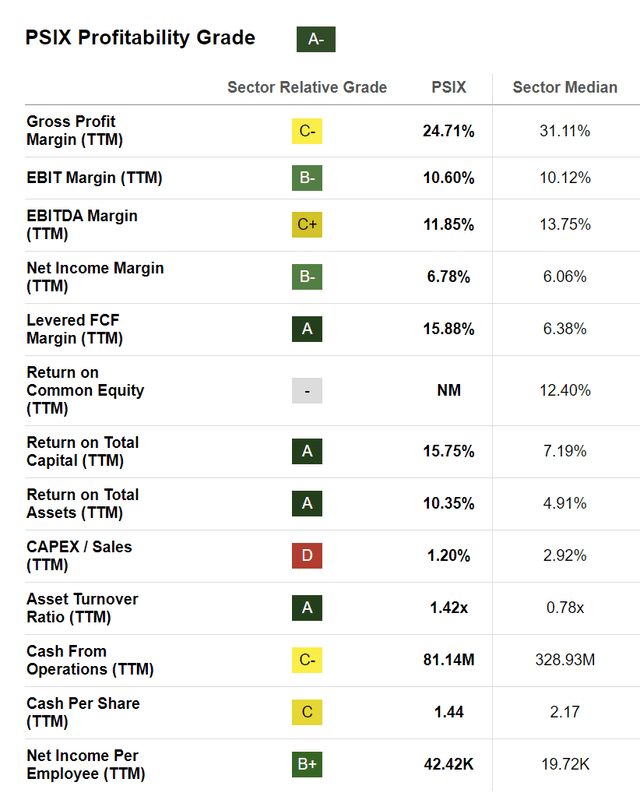

Digging into the specifics on profitability, the only concerns are with gross profit margin and cash from operations for the trailing twelve-month period, which as previously discussed both showed dramatic improvement in Q1.

Seeking Alpha

Risks, Competition, Threats

Risks to the company’s continued growth prospects include a potential slowdown in the global economy, further declines in the industrial and transportation end markets, increased competition for data center power solutions, and potentially a drag on the Chinese economy that could impact the Weichai partnership.

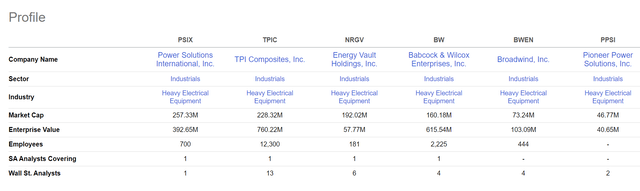

According to the Peers page on SA, some of the companies that might be considered peers to PSI include Broadwind, Inc (BWEN), Pioneer Power Solutions (who received a Nasdaq notice of non-compliance in April), and several others that specialize in renewable energy, none of which are direct competitors in the power solutions markets that PSI serves.

Seeking Alpha

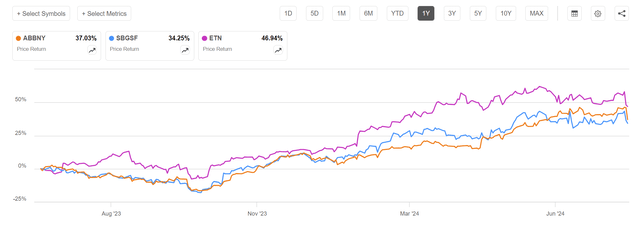

Much larger companies such as ABB (OTCPK:ABBNY), Eaton (ETN), and Scheider Electric (OTCPK:SBGSF) might be considered competitors for data center power solutions, however, PSI offers more specialized solutions that could lead to partnering opportunities with those larger firms in some cases. However, if the trend is any indication all 3 of those larger peers have also delivered strong returns over the past year further illustrating that global data center growth is powering earnings and driving their stock prices higher.

Seeking Alpha

Valuation and Price Target

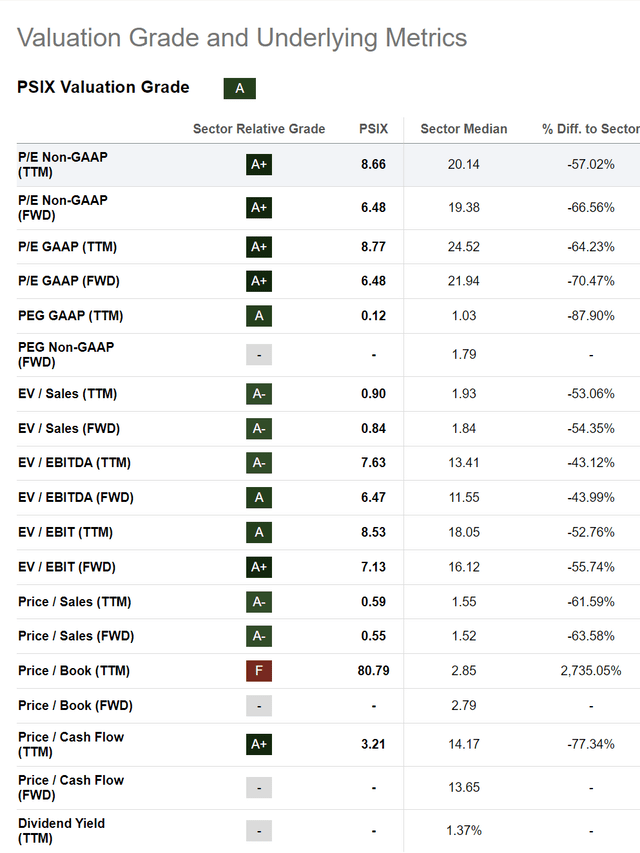

Despite the stock price shooting higher over the past two months, PSIX still trades at a TTM P/E of about 8.6x, which is typically considered very inexpensive for a growth stock where the sector median is closer to 20x. As shown on the Quant valuation grade and underlying metrics for PSIX, the stock gets an A grade due to nearly all of the metrics showing a very good value with the exception of price/book, which is not a very meaningful metric for this stock in my opinion.

More meaningful metrics include the forward P/E, forward EV/EBITDA, and forward Price/Sales metrics, all of which are very low compared to the sector median.

Seeking Alpha

Although there is only one Wall Street analyst currently following the stock (who gives it a Strong Buy rating), that analyst offers some EPS estimates for full year 2024 and 2025 that we can use to develop price targets.

Seeking Alpha

For the 2024 estimate of $1.75 in earnings, at a more reasonable P/E of 15x (still well below the sector median) we arrive at a price of $26.25, more than double the current stock price. The next earnings report is due out August 12 and we should know more then regarding the outlook for 2024 and beyond, but my expectation is that PSIX will report yet another earnings beat and forward EPS revisions will be raised, propelling the stock price even higher.

Editor’s Note: This article was submitted as part of Seeking Alpha’s Best Growth Idea investment competition, which runs through August 9. With cash prizes, this competition — open to all analysts — is one you don’t want to miss. If you are interested in becoming an analyst and taking part in the competition, click here to find out more and submit your article today!

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here