RDDT’s Investment Thesis Remains Speculative, Despite The Robust Performance Metrics

Reddit, Inc. (NYSE:NYSE:RDDT) is almost synonymous to the Meme stock craze occurring during the heights of pandemic, with the recent events triggered by Roaring Kitty further fueling its recent recovery.

For now, with the social media platform benefiting from the ongoing meme craze, the stock has also outperformed expectations and the wider market, significantly aided by the robust performance metrics observed in its FQ1’24 earnings call in May 2024.

With the company set to announce their FQ2’24 financial results on August 6, 2024, we shall highlight a few metrics readers may want to look out for.

1. Advertising Opportunities & User Monetization

For reference, RDDT, as a social media platform, relies on advertising and user monetization to generate revenues, with advertising currently being the top-line driver at 98.1% (+0.3 points YoY) of its sales in FY2023 and 91.6% in FQ1’24 (-6.1 points YoY).

Even so, as observed in FQ1’24, it is apparent that RDDT has attempted to diversify their sales, attributed to other revenues’ (content licensing agreements) accelerated growth by +454% YoY compared to advertising at +39.1% YoY.

The same has been observed in its robust multi-year licensing remaining performance obligations of $188.1M, with it providing great insights into its intermediate-term prospects.

At the same time, RDDT has been looking to increasingly monetize its Reddit Premium subscriptions, attributed to the expanding Daily Active Uniques [DAUq] of 82.7M (+37% YoY) and higher Average revenue per unique [ARPU] of $2.94 (+8%).

Combined with the management’s FQ2’24 revenue midpoint guidance of $247.5M (+1.8% QoQ) and adj EBITDA guidance of $7.5M (-25% QoQ), it is apparent that they remain somewhat optimistic about generating profitable growth ahead.

This development is promising indeed, reversing RDDT’s numerous years of cash burn with FY2024 slated to be the year of positive cash flows (finally).

At the same time, readers may look forward to accelerated DAUq and ARPU growth in the upcoming FQ2’24 earnings call, since the management has guided intensified global expansion through Machine Translation tools while appealing to French readers (in testing stage) and Spanish readers (second wave) in 2024.

As a result, we may see RDDT offers another optimistic FQ3’24 earnings guidance, further underscoring its ability to scale its business beyond the US (and English-speaking readers), which currently comprises 82.2% of its overall revenues. Impressive indeed.

2. Growth Premium Appears To Be Rather Aggressive

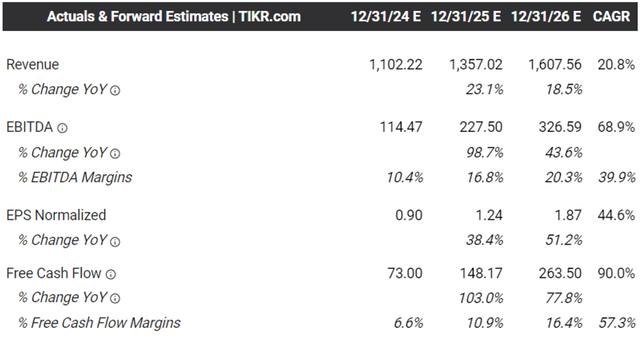

The Consensus Forward Estimates

Tikr Terminal

As discussed above, RDDT has guided robust profitable prospects, with the global expansion likely to be a growth driver over the next few years.

Perhaps this is why the consensus has offered the optimistic forward estimates, with the social media platform expected to report a top/ bottom-line growth at a CAGR of +20.8%/ +44.6% through FY2026, building upon the +48.3%/ +96.3% reported in FQ1’24, respectively.

With the global social media advertising market expected to grow at an accelerated CAGR of +12.4% to $262.62B by 2028, the consensus estimates do not appear to be overly ambitious, for so long that RDDT is able to consistently grow its engagement/ ARPUs globally.

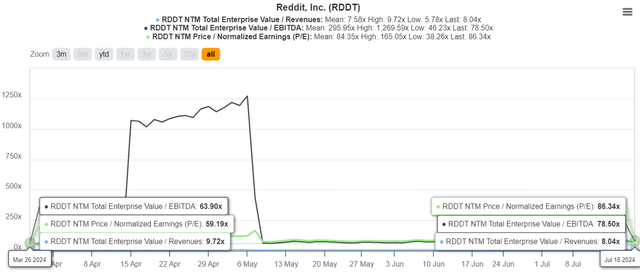

RDDT Valuations

Seeking Alpha

Perhaps this is why the market continues to award RDDT with the premium FWD EV/ EBITDA of 78.50x and FWD P/E of 86.34x, compared to its IPO levels of 63.90x/ 59.19x and the sector median of 7.85x/ 13.48x, respectively.

Even so, readers need to be aware of RDDT’s numerous social media competitors, such as Alphabet’s YouTube (GOOG) trading at FWD P/E of 24.15x with the projected adj EPS growth at a CAGR of +19.4% through FY2026, Meta (META) at 22.95x/ +20.9%, Snap (SNAP) at 57.81x/ +88.1%, the yet profitable Roblox (RBLX), and the private TikTok, Discord, and X (used to be Twitter).

With RDDT priced at a notable premium compared to its peers, we believe that there is a minimal margin of safety here.

While we concur that there are great tailwinds ahead, we believe that with elevated P/E valuations come great expectations, as observed in the recent rotation from growth stocks to value stocks.

With the macroeconomic outlook still uncertain, we are uncertain if it is wise to chase RDDT at these inflated levels, especially since the CBOE Volatility Index are increasingly higher at the time of writing.

As a result, we will be using the more moderate social media peer group P/E mean of ~40x in our fair value calculation for an improved margin of safety, with this number also inline to its peers’ valuations/ growth rates and RDDT’s April 2024 bottom P/E 41.62x.

3. Potential Volatility

RDDT 4M Stock Price

Trading View

It goes without saying that RDDT’s social media platform is one that has been closely associated with meme stocks, such as GameStop (GME) and AMC Entertainment (AMC).

Perhaps, this explains why RDDT is also highly shorted at 18.98% at the time of writing, with the stock’s movement closely mirroring those of its meme stock peers over the past few months.

Therefore, while the social media platform’s fundamental performance may be robust as discussed above, further aided by the extremely healthy balance sheet with net cash of $1.67B (+38% QoQ) and inherent lack of debts, it is undeniable that the stock may remain volatile in the near-term.

It is apparent from these developments that RDDT is only suitable for traders with a keen sense of timing and higher risk appetite, since it is unlikely that the social media platform may decouple from the meme stocks and the retail stock traders in the intermediate term.

So, Is RDDT Stock A Buy, Sell, or Hold?

RDDT 4M Stock Price

Trading View

For now, RDDT has continued to chart an impressive recovery since the April 2024 bottom, with these levels also improved than its IPO levels in March 2024.

Even so, it is apparent that the stock is trading at a premium compared to our fair value estimates of $36, based on the peer group mean FWD P/E of ~40x (as discussed above) and the consensus FY2024 adj EPS estimates of $0.90.

At the same time, there appears to be a minimal margin of safety to our long-term price target of $74.80, based on the consensus FY2026 adj EPS estimates of $1.87.

Combined with the RDDT stock’s highly shorted position, high percentage of retail investor ownership, its correlation to meme stocks, and relatively small float, we are uncertain if it is wise to recommend a Buy here.

This is despite the potential double beat FQ2’24 earnings call, based on a successful French user campaign, higher meme stock activities, and the intensified user engagement surrounding the US election/ the uncertain macroeconomic/ ongoing global geopolitical events.

Lastly, readers must note that RDDT insiders have been cashing out their holdings over the past few months, with $46.4M reported thus far.

At the same time, as with most IPOs, with ~133M shares, or the equivalent $8.75B in value based on the stock prices at the time of writing, subject to the lock-up expiration in August 2024, we may see more profit taking in the near-term.

As a result of the potential capital losses, we believe that it may be more prudent to initiate a Hold (Neutral) rating for the RDDT stock instead.

Interested investors may be better off observing a little longer and only adding upon a deep pullback for an improved margin of safety. Even then, the portfolio must also be sized according to their risk appetite and investing trajectory, since there may be more near-term volatility.

Read the full article here