Since 2020, the restaurant industry has faced multiple waves of woes. Initially, lockdown policies caused immense sales declines amongst many restaurants, causing many to resort to debt to offset lost sales. As those pressures waned, the industry faced a sharp increase in food and labor costs, creating declines in restaurants’ profit margins. As a result, a significant and growing number of restaurants and franchises have gone bankrupt this year. Growing strains in consumer discretionary spending could be the final nail in the coffin for many restaurants.

Of course, some sit-down restaurants have defied the numerous headwinds. Texas Roadhouse (NASDAQ:TXRH) is trading near its all-time high and nearly twice its pre-COVID level. To a large extent, publically traded restaurants, including Texas Roadhouse’s nearest peer, Darden (DRI), have fared better than small-business restaurants due to superior access to capital, allowing them to benefit from the declining competition from failed privately owned restaurants. Indeed, in valuing stocks like Texas Roadhouse, it is crucial to consider they’re not necessarily benefiting from “peak” restaurant demand but a falling number of sit-down restaurants.

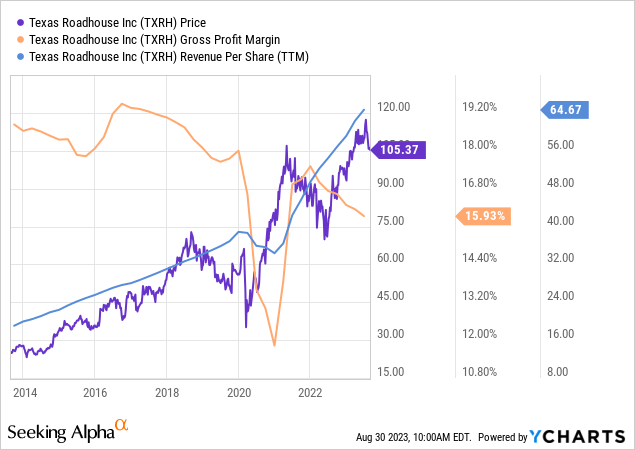

Despite headwinds, Texas Roadhouse has had tremendous sales per share growth over recent years. The stock is highly valued at a forward “P/E” of 22.6X, implying many investors expect the company to continue to expand rapidly. While it is true that the company has had great historical performance, I believe that industry headwinds will eventually meet the company, potentially jeopardizing its high valuation today.

The Restaurant Re-Hiring Boom is Over

Since ~2021, the restaurant industry has struggled with significant supply-side constraints caused partly by the mass layoffs in 2020. As demand began to normalize, the industry faced a massive shortage of workers, leading to significant declines in profit margins. This is the primary issue causing mass restaurant closures today, as these companies cannot keep raising prices at the same pace as costs. Although Texas Roadhouse has seen solid EPS growth over this period, that is primarily due to sales growth. The company’s gross margins have continued to deteriorate relatively rapidly. See below:

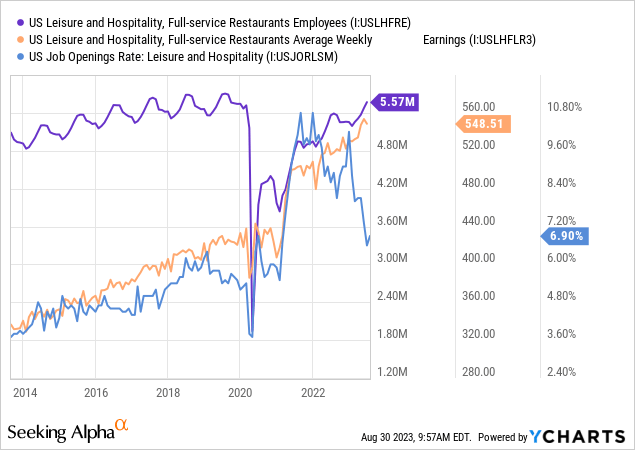

The core cause behind this trend is the sharp increase in labor costs. Job openings in the industry rose dramatically in 2021, bringing pay much higher. Today, full-service restaurant employees are nearly at pre-COVID levels, and job openings are returning to normal. See below:

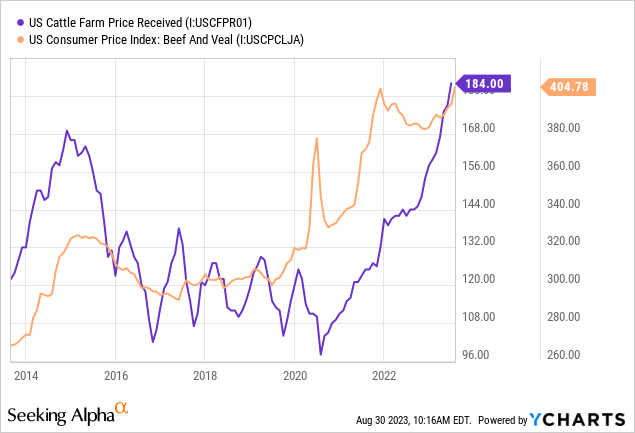

In the short term, labor costs for Texas Roadhouse should continue to grow as job openings are still elevated. That said, this factor pressuring the company’s costs should not continue past 2024 since most restaurant positions are likely nearly filled. However, meat, specifically beef prices, will likely continue to soar. Drought conditions throughout the US have increased cattle farming costs, leading to much lower herd numbers as farmers look to reduce overhead. As a result, cows and beef are becoming increasingly short-supplied, causing prices to rise far faster than general inflation. See below:

Drought conditions persist throughout most of the vital cattle-producing areas of the US. Unfortunately, the longer these conditions remain, the longer it will take for the market to normalize since it takes years for a few years before a cow is slaughtered. Obviously, many factors are at play regarding this issue; however, it appears very likely that this issue will push Texas Roadhouse’s costs even higher, even if labor pressures are starting to slow. To maintain profit margins, the company is looking to increase menu prices again; however, doing so will likely increase its economic exposure.

Overall, I believe many positive factors benefiting Texas Roadhouse, such as significant sales growth, same-store sales, and other backward-looking measures, do not tell the full story. The primary cause of the firm’s strong sales growth is not expansion or higher demand but significant price increases to combat cost growth. Its gross margins have declined significantly, only to be offset by reductions in operating expenses to sales levels, causing its operating margin to be relatively constant since 2020. However, efforts to lower operating overhead will likely not continue, meaning its operating margins are liable to decline going forward, given its gross margin continues to wane.

Texas Roadhouse Demand May Be Peaking

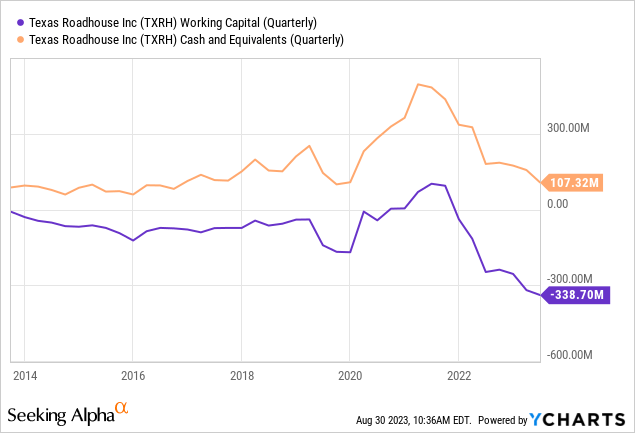

Since ~2021, Texas Roadhouse has managed to offset supply-side pressures with substantial post-pandemic demand recoveries. The general trend since 2020 has been a decline in private, particularly small business, restaurants, indirectly benefiting publically traded restaurants with far superior access to capital, allowing them to navigate 2020 more efficiently. Texas Roadhouse has no long-term financial debt; however, its total liabilities (primarily lease obligations) have tripled since 2018 to $1.4B (from $400M). Additionally, its cash position has dwindled while its working capital has fallen into negative territory. See below:

Over the next year, Texas Roadhouse has $338M more in current liabilities than in total current assets, implying some need for improved liquidity. Its TTM operating cash flow is $500M and may decline should its operating margin slip, as I expect, indicating it may need external financing to meet its short-term obligations. More importantly, it leaves the company in a very poor position should restaurant demand decline, mainly because it’s increasingly in “luxury” status as its menu prices rise faster than wages and inflation.

The general trend since 2020, and even prior, is a decline in restaurant traffic, offset by higher fast-food demand. Texas Roadhouse has largely defied this trend, partially due to its focus on higher-quality dining experiences. Of course, as many restaurants close, those that survive will naturally see higher traffic, at least in the short term. As its smaller competitors slowly died off, Texas Roadhouse quietly became the largest steakhouse chain in the US, partially because its size gives its supply chain and cost advantages. Still, given the restaurant market is declining, Texas Roadhouse has limited upside because the decline of its competition primarily fuels its growth. As its market share grows, its ability to grow further becomes more limited.

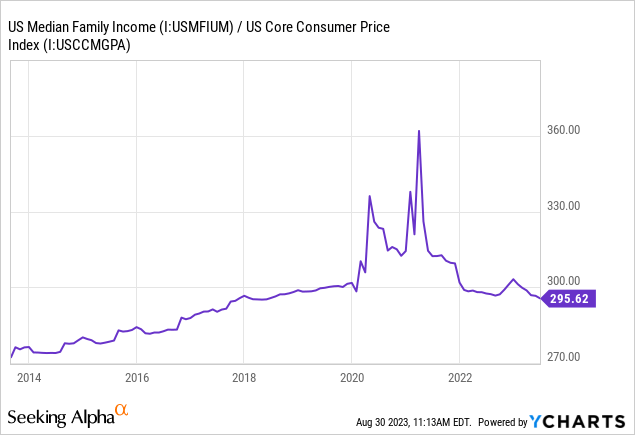

Of course, the company’s sales may also benefit from the post-COVID rebound. As restrictions ended, there was a surge in the number of people looking to return to steakhouses as many people understandably wished to enjoy those things they could not in 2020-2021. That occurred despite the ongoing sharp decline in inflation-adjusted median family incomes and the above-inflation menu price growth at Texas Roadhouse. Currently, median family incomes compared to core consumer prices are roughly around 2017 levels. See below:

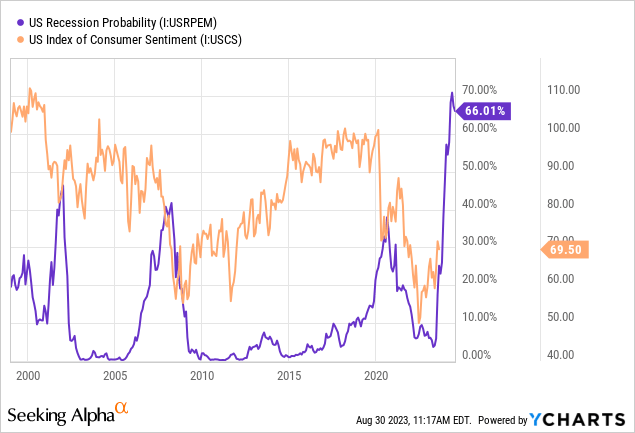

This trend does not account for the likely fact that prices experienced by people may not be fully reflected in the consumer price index. If experienced inflation is higher than “CPI inflation,” a household’s discretionary spending capacity would be lower. Further, as discussed in recent articles, technical models that predict recessions are showing significant red flags today, with the “Mishkin Esterlla” model showing a higher recession risk than in 2007 and 2000. See below:

Clearly, the typical US consumer is not in a robust financial position. Since 2021, credit card debt levels have soared as many people use debt to maintain spending levels despite falling real family incomes. That trend is likely causing Texas Roadhouse to appear less cyclically exposed than it truly is temporarily.

Put simply, many people want steak after being deprived in 2020 and are prioritizing that over financial stability. Subjectively, I expect this trend to continue until it cannot since the turbulent experience in 2020 certainly caused many people to value experiences over saving money. That said, in the event of a recessionary unemployment increase, that trend may rapidly grind to a halt as incomes fall even faster than inflation. Further, upcoming federal student loan repayments should also lower discretionary consumer spending; however, Texas Roadhouse customers may be less exposed to that demographic than many.

The Bottom Line

On the one hand, I believe Texas Roadhouse is a fundamentally solid company with a management focus that has allowed it to benefit indirectly from the headwinds in the restaurant market. As its smaller competitors struggle with costs, it has generally managed to reduce operating overhead sufficiently while encouraging customer activity enough that its EPS has continued to rise. Further, although consumer spending power has weakened and may continue to, the company has benefited even more from a surge in post-pandemic dining activity due to its reduced competition.

Still, I believe most factors benefiting Texas Roadhouse are likely far more temporary than most expect. Behind the scenes, the company is fighting significant COGS growth and probably cannot continue lowering operating overhead to keep that issue from harming its EPS. Further, the firm’s working capital level is very poor, exposing it to a recessionary demand decrease.

On that note, I do not expect steakhouse demand to continue to be so elevated in the long term as household savings levels continue to decline while credit card debt grows. In some sense, the consumer economy, specifically for restaurants, appears to be in a “party like it’s 1999” mode as demand is high despite substantial headwinds. At some point, potentially requiring an unemployment spike, the party will inevitably end as many people’s savings and debt levels reach extremes.

The fundamental issue with TXRH is its operational position and excessively high valuation. With a forward “P/E” of 22.6X, nearly twice that of most consumer discretionary stocks, investors appear to have unreasonable expectations regarding its future growth potential. Its valuation implies the company’s EPS will continue to expand quickly for years to come without any significant hiccups. In my opinion, its EPS is far more likely to decline over the coming year as it struggles with COGS increases and potentially a recessionary decline in discretionary consumer spending activity. Further, its growth potential is likely limited because it is absorbing market share in a generally declining market.

In my opinion, because it is highly exposed to both supply-side and consumer risk factors, I believe TXRH is a solid short opportunity today. I expect its forward “P/E” to fall to at least 14X, giving it a price target of $65 – 38% lower. I believe such a decline does not require a recession but simply a more realistic growth outlook for the company. Of course, the stock may remain elevated or continue to rise without a recession, so it is not a riskless short bet. The stock does have momentum that could push it higher, but as consumer spending pressures mount, I do not believe expectations surrounding the company can remain so exuberant. TXRH’s implied volatility is also extremely low today at 19%, indicating put options may be an undervalued way to bet against it.

Read the full article here