Dating back to 1851, The New York Times Company (NYSE:NYT) is one of the oldest and most iconic companies in the world. Over its life, it has become a major news organization worth billions of dollars. Many years ago, there were concerns about its ability to remain competitive as more news shifted from the traditional newspaper format to online, and as we saw a proliferation of free news content. But management has done a fantastic job of adapting, turning the platform into a primarily subscription-based service with not only its core news segment, but also a sports-focused offering known as The Athletic.

The overall quality and growth record of the company achieved as a result of this transformation has necessitated a premium on shares. That is why, as much as I am a fan of the business from an operational standpoint, I had no choice but to keep the company rated a ‘hold’ when I last wrote about it in December of 2023. When I rate a company a ‘hold’, it is a statement of my belief that shares should see upside or downside that is more or less in line with the broader market. To be honest with you, shares have outperformed these expectations marginally, with the stock up 17.4% at a time when the S&P 500 is up 14.8%. But considering the amount of time we are talking about, that is not a massive disparity.

Looking at the company again, I remain convinced that a ‘hold’ rating is the best that I can justify at this point in time. However, it’s important to be flexible as new data comes in. And it just so happens that, before the market opens on August 7th, the management team at the company is expected to announce financial results covering the second quarter of its 2024 fiscal year. Analysts are anticipating a growth in both revenue and profits. But if the picture ends up looking better than anticipated, it wouldn’t be unthinkable that an upgrade could be on the horizon. But to me, that surprise would have to be quite large.

A look at recent performance

Author – SEC EDGAR Data

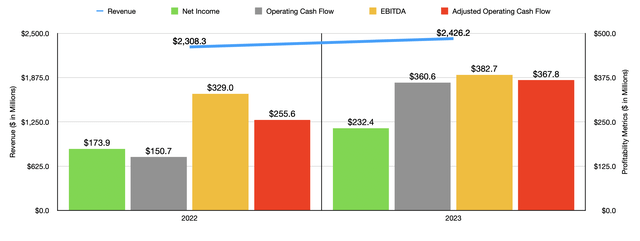

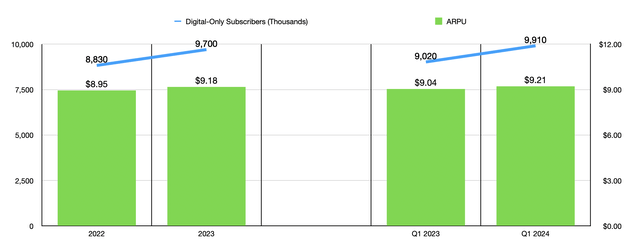

From a purely fundamental perspective, there is no denying that The New York Times Company is doing really well. Take the 2022 to 2023 fiscal years as an example. During 2023, the company generated $2.43 billion worth of revenue. That’s an increase of 5.1% over the $2.31 billion generated one year earlier. This has been driven by consistent impressive growth in the number of digital subscribers to the company’s platform. By the end of 2023, the firm had 9.70 million paid subscribers. That’s 9.9% higher than the 8.83 million reported just one year earlier. Digital only ARPU (average revenue per user) per month managed to rise during this time as well, climbing from $8.95 to $9.18. What’s really great about this is that management attributed this increase to subscribers that were ‘graduating’ from promotional offerings to standard, higher priced ones. Increased prices charged to tenured, non-bundled subscribers, also contributed to this improvement.

Author – SEC EDGAR Data

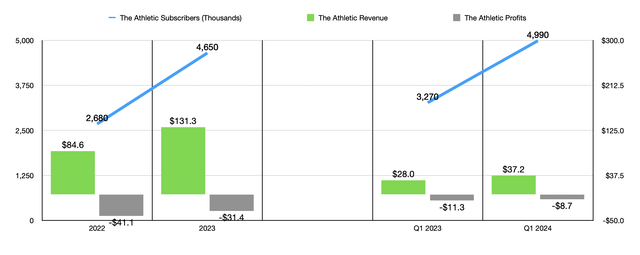

A major source of subscriber growth for the company has been its sports focused offering called The Athletic. This is a company that was originally purchased back in 2022. And from 2022 to 2023, its subscriber base exploded from 2.68 million to 4.65 million. Despite this growth, The Athletic is still only a very small piece of the overall pie for the business. Revenue associated with it in 2023 totaled $131.3 million. That’s well above the $84.6 million reported for 2022. But considering that this still makes it responsible for only 5.4% of the company’s overall sales, the core operations under the firm’s NYTG segment still are responsible for the bulk of the value that shareholders get from the company.

Author – SEC EDGAR Data

With revenue rising, earnings and cash flows have moved up nicely. Net income has grown from $173.9 million to $232.4 million. Other profitability metrics rose in tandem with this. Operating cash flow more than doubled from $150.7 million to $360.6 million. If we adjust for changes in working capital, we get a rise from $255.6 million to $367.8 million. And finally, EBITDA for the company managed to grow from $329 million to $382.7 million.

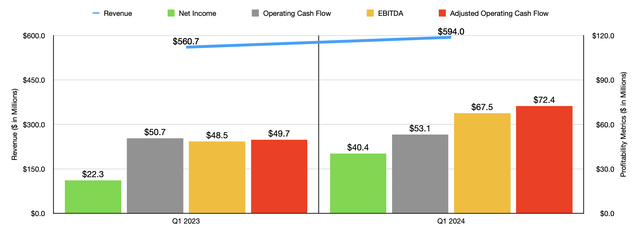

For the 2024 fiscal year, we only have data covering the first quarter. During this time, revenue came in at $594 million. That’s 5.9% greater than the $560.7 million reported one year earlier. Growth to 9.91 million subscribers for the company’s digital offerings translated to a year over year increase in digital only subscriber count of 9.9%. The company also benefited from an increase in ARPU from $9.04 to $9.21. Once again, The Athletic continued to post big improvements in subscriber count, with the platform boasting 4.99 million paid subscribers compared to the 3.27 million reported for the first quarter of 2023. Even with this, however, revenue of $37.2 million represents only a small portion of the company’s overall sales. It is still the NYTG segment that is responsible for the vast majority of the company’s operations.

Author – SEC EDGAR Data

As was the case from 2022 to 2023, The New York Times Company continued to benefit from higher profitability as well. Net income in the first quarter of 2024 was a hefty $40.4 million. That’s nearly double the $22.3 million Reported the same time last year. Operating cash flow grew only slightly from $50.7 million to $53.1 million. But if we adjust for changes in working capital, we get a nice increase from $49.7 million to $72.4 million. And finally, EBITDA for the company grew from $48.5 million to $67.5 million.

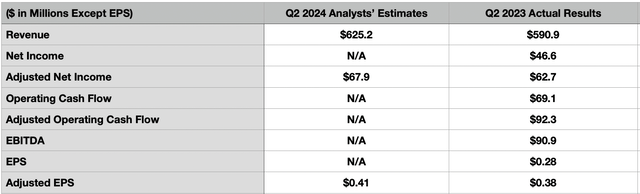

As I mentioned at the start of this article, before the market opens on August 7th, management is expected to announce financial results covering the second quarter of the 2024 fiscal year. We don’t really know what to expect. We do know, however, that analysts are forecasting sales of $625.2 million. That would be 5.8% above the $590.5 million reported for the second quarter of 2023. For its part, management has been quite vague. They did say that total subscription-based revenue should rise by between 6% and 8% year over year. Digital ad revenue should grow at a mid to high single digit rate. Total ad revenue, impacted by weak advertising sales on the print side of things, should rise by only a low single digit rate. And all other revenue should be somewhere between flat and up at the low single digit rate. But none of this gives us a concrete number to go off of. Considering the growth in subscription revenue anticipated, the amount forecasted by analysts is probably in the ballpark.

Author – SEC EDGAR Data

On the bottom line, analysts expect earnings per share, on an adjusted basis, to come in at about $0.41. That would be an improvement over the $0.38 per share generated one year earlier. If this comes to fruition, it would translate to an increase in adjusted net income from $62.7 million to $67.9 million. Unfortunately, analysts have not provided any estimates regarding GAAP earnings. But in the table above, you can see what these looked like for the second quarter of 2023. That table also has other profitability metrics that investors would be wise to pay attention to. In all likelihood, if revenue and adjusted earnings are rising on a year over year basis, most, if not all of these, should grow as well.

Author – SEC EDGAR Data

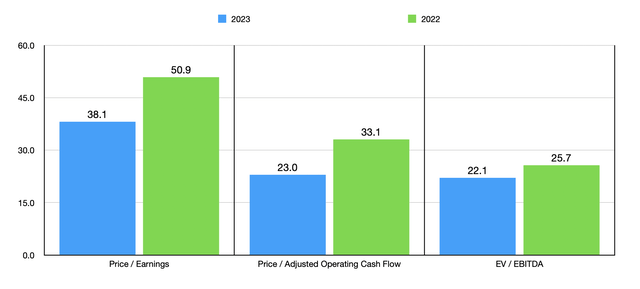

A steadily growing subscription-based company is right up my alley. These are the kinds of firms that I like. Subscriptions offer stable cash flows and the continued growth of the company indicates that additional value will be created as time goes on. However, the market also seems to like these businesses, as evidenced by how pricey shares are. In the chart above, you can see how shares are valued using results from 2022 and 2023. Seeing a company trade at these kinds of multiples is definitely discouraging. Unfortunately, the stock is also pricey compared to similar enterprises. In the table below, I compared it to five such firms. On a price to earnings basis, only two of the five companies were cheaper than it. But this number jumps to four of the five on an EV to EBITDA basis and, on a price to operating cash flow basis, our candidate ends up being the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| The New York Times Company | 38.1 | 23.0 | 22.1 |

| News Corp (NWS) | 79.3 | 13.0 | 14.6 |

| Pearson (PSO) | 18.9 | 14.7 | 6.8 |

| John Wiley & Sons (WLY) | 117.1 | 12.4 | 84.0 |

| Scholastic (SCHL) | 80.1 | 6.3 | 9.2 |

| Gannett (GCI) | 17.7 | 6.2 | 8.6 |

Takeaway

Operationally speaking, The New York Times Company is a truly remarkable firm. The company has defied expectations over the past several years and has grown nicely as a result. The firm has no debt on its books and it enjoys $379.1 million in cash and cash equivalents. This doesn’t even factor in an additional $307.2 million in long term securities. Continued growth and improvements on the bottom line are great to see. And if analysts are correct, further growth is just around the corner. But because of how pricey shares are, I think that further upside relative to the broader market is most certainly limited. And as a result, I have decided to keep the firm rated a ‘hold’ for now.

Read the full article here