Investment action

I recommended a buy rating for Thomson Reuters (NYSE:TRI)(TSX:TRI:CA) when I wrote about it two months ago in June, as I expected organic EPS to grow robustly given the strong adoption of AI products. Based on my current outlook and analysis, I recommend a buy rating. TRI organic growth profile continues to trend in my expected direction, and with the step-up in GenAI investments that is resulting in new innovative products, I continue to see organic growth improving.

Review

TRI reported earnings two days ago, where it saw reported revenue growth of 5.6% and organic growth of 6.2%, with total revenue reaching $1.74 billion. The Big 3 segments (Legal Professionals, Corporates, and Tax & Accounting Professionals) organic growth remained robust at 7.8% (vs. 7% in 2Q23). Splitting them, Legal Professionals saw 7% organic growth; Corporates saw 8% organic growth; and Tax & Accounting Professionals saw 10% organic growth. That said, adj EBITDA margin contracted by 300bps from 40.1% in 2Q23 to 37.1% in 2Q24, of which the Big 3 segments saw a bigger compression from 45% in 2Q23 to 40.9% in 2Q24. However, adj. EPS of $0.85 still came in better than consensus forecast of $0.82.

With the healthy organic growth performance, management raised its FY24 reported revenue growth guidance from 6.5% to 7% to 7% (organic revenue growth raised from 6% to 6.5% to 6.5%), of which the Big 3 segments are now expected to grow organically by 8% (from the prior guide of 7.5% to 8%). Reinvestment into the business is implied to step up, as management reiterated their adj. EBITDA margin guide of 38% (43% for the Big 3 segments) despite the raised revenue guide.

Author’s work

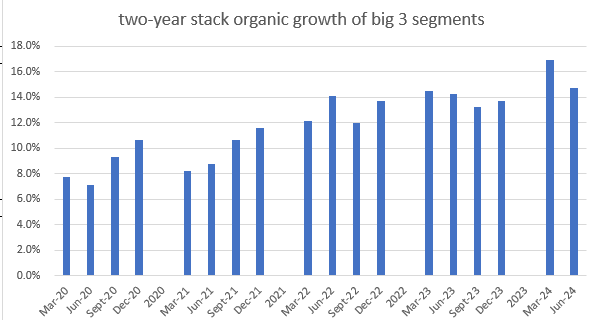

TRI remains one of my favorites as long as the business continues to drive improvement in its organic growth profile. Although organic growth did step down from the 9.9% seen in 1Q24 to 7.8% in 2Q24, I think the growth trend remains a positive one. To smooth out any seasonality impact, a better way to assess the organic growth improvement is to look at the two-year stack, and the trend continues to be an improving one. Currently, the big 3 segments account for 82% of total revenue and are growing at a much faster rate than the overall business. As such, from a percentage mix perspective, TRI should continue to see accelerating organic growth when the big three segments become a larger part of the business. Very encouragingly, the strong growth in the big 3 segments is driven by double-digit growth in TRI’s flagship products (e.g., Practical Law, Confirmation, SurePrep, Pagero, and Indirect Tax), which means there is room for growth to further accelerate to >10%.

Adoption of GenAI products continues to support strong growth (you may find my views on TRI’s GenAI products in my previous post). This is evident from the performance in the Legal segment, where GenAI functionalities have been one of the key drivers that drove the 100bps improvement in organic growth vs. 2Q23. Management expects GenAI functionality demand in this segment to accelerate in the coming quarters, and I believe this is likely to happen as TRI has stepped up their GenAI product initiatives. From a capital allocation perspective, the expected budget has increased from $100 million in 2023 to more than $100 million in 2024 (per 1Q24 earnings call). From an innovation perspective, TRI continues to be on the ball by rolling out new products. In the quarter, TRI launched two additional GenAI products:

- CoCounsel Drafting is a legal drafting solution in Microsoft Word that enables clients to leverage Practical Law content and customers’ own data. This should drive up work efficiency for users as it cuts down on the time to switch between windows.

- CoCounsel Checkpoint, which is a chat-based tax research solution, Notably, this is the first GenAI product that TRI launched for the Tax & Accounting segment, further convincing me that TRI can roll out and integrate GenAI capabilities across product segments.

These new productivity-enhancing products should see strong adoption, as TRI’s research found that AI-powered tech tools can save up to four hours per week. Another notable aspect of the CoCounsel product series is that TRI is implementing an enterprise-wide model. I prefer this pricing model vs. per-seat pricing, as any price increase will be less prominent. Given the step-up in productivity, I would expect TRI to have significant pricing power (or, in management’s words, they can capture significant efficiency gains realized by clients).

Valuation

Author’s work

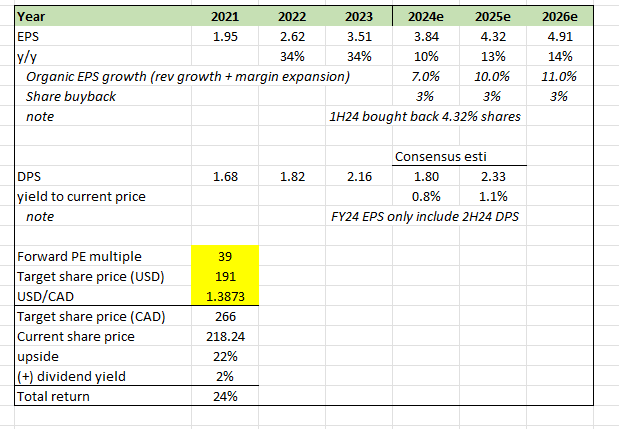

My expectation for the TRI EPS growth outlook remains largely the same as in my previous model, as organic growth continues to be robust and expectation expect it to accelerate over the foreseeable future. I did revise FY24 EPS organic growth down from 8% to 7% as TRI step up investments in FY24. As of 2H24, the pace of share buyback continues to track above my full-year expectation of 3% buyback. The two areas that I have adjusted in my model are DPS and valuation multiples. For DPS, since 2Q24 is over, I have adjusted to only include 2H24.

Because of the recent market sell-down, TRI’s valuation has become attractive relative to peers (listed below), now trading in line with peers (just 3% premium to peers’ average of 38x forward PE), where it has historically traded at ~14% premium. As I don’t see any structural negative change to the business that should change how TRI should trade relative to peers, I am expecting TRI’s valuation to go back to a 14% premium eventually (in fact, TRI is now structurally better given the improving organic growth profile). Be reminded that TRI traded up to a 21% premium just two months ago, so going back to a 14% premium is surely plausible.

Author’s work

Risk

Near-term EPS may be slower than I modeled as TRI steps up in GenAI investments. Management did note an additional margin contraction in 3Q24 to 34%. The good news is that this should drive growth eventually when TRI rolls out new products, so EPS growth is delayed but not impaired. Another risk is that FindLaw (10% of the Legal segment revenue), an online legal information solution for consumers and small businesses, is still performing very poorly. If macro conditions remain poor, underlying demand may get worse, especially since this is a product for consumers and small businesses.

Final thoughts

My recommendation is a buy rating as TRI continues to see robust organic growth, underpinned by the strong performance of its Big 3 segments. Despite a slight deceleration from the previous quarter, the two-year stacked growth trend remains positive. TRI’s focus on investing into GenAI should continue to support growth ahead.

Read the full article here