I assign a Buy investment rating to Tokio Marine Holdings, Inc. (OTCPK:TKOMY) (OTCPK:TKOMF) [8766:JP] stock.

My opinion is that Tokio Marine can improve its ROE to justify a higher P/B multiple with ROE expansion drivers like the sale of cross-shareholdings, and the increase in buybacks and dividends. As such, I have a bullish view of TKOMY which supports a Buy rating.

The company’s shares are traded on both the Tokyo Stock Exchange and the Over-The-Counter market. The mean daily trading values for Tokio Marine’s OTC shares and Japan-listed shares were $2 million and $200 million (S&P Capital IQ), respectively, for the past three months. Readers can choose to trade in Tokio Marine’s relatively more liquid Japanese shares with US brokerages like Interactive Brokers.

Company Description

TKOMY is “Japan’s largest general insurance group” according to Hennessy Funds’ May 2024 article. As per MS&AD Insurance Group Holdings’ Japanese insurance industry research report, Tokio Marine and its peers, MS&AD Insurance and Sompo Group, in aggregate boast a “90% market share” of the country’s non-life insurance segment.

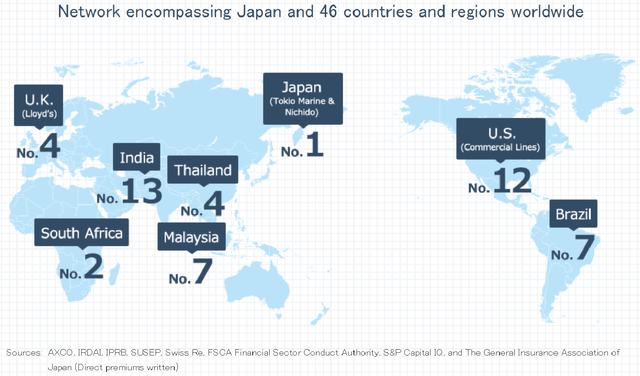

Tokio Marine is also among the leading insurance companies in key international markets, as per the chart presented below.

Tokio Marine’s Market Share Ranking In Specific Overseas Markets

Tokio Marine’s Corporate Website

In its FY 2023 integrated report, TKOMY highlighted that it is the ninth largest non-life insurance company worldwide in terms of earnings contribution. Looking ahead, the company is guiding for a 75:25 profit split between its foreign and domestic business operations for FY 2024 (April 1, 2024 to March 31, 2025).

Note that Tokio Marine refers to fiscal 2023 as the year ended March 31, 2024, and I will be using the company’s definition for the purpose of this article.

Tokio Marine Is Trading At A Discount To Peers

The market currently values Tokio Marine at 2.4 times trailing P/B as per S&P Capital IQ. As a comparison, TKOMY’s peers Zurich Insurance Group AG (OTCQX:ZURVY) (OTCQX:ZFSVF) [ZURN:SW] and The Progressive Corporation (PGR) are now trading at comparatively higher trailing P/B multiples of 3.1 times and 5.5 times, respectively.

Tokio Marine’s significant valuation discount vis-a-vis the company’s peers is likely attributable to the former’s relatively lower ROE. In its July 2024 investor presentation slides, TKOMY disclosed that its latest fiscal year or FY 2023 ROE was 15.0%.

TKOMY also noted in its July investor presentation that other non-life insurance companies have set ROE goals in the high-teens to high-twenties percentage range, based on its benchmarking study. As another comparison, the consensus FY 2024 ROE estimates for Zurich Insurance Group and The Progressive Corporation are 22.8% and 29.6% (source: S&P Capital IQ), respectively.

A fair P/B valuation multiple is equal to [ROE minus Perpetuity Growth Rate] divided by [Cost of Equity minus Perpetuity Growth Rate] as per the Gordon Growth Model valuation formula. Assuming a 15% ROE (TKOMY’s FY 2023 ROE), an 8% Cost of Equity in line with the industry average, and a 3% Perpetuity Growth Rate, Tokio Marine warrants a fair P/B valuation metric of 2.4 times. In other words, the stock’s current valuations are reasonable, taking into account its ROE metric.

In the next section, I touch on Tokio Marine’s valuation re-rating potential, taking into consideration an expansion of its ROE in the years ahead.

Achievement Of 20% ROE Target Will Justify A Higher P/B Multiple

As indicated in its July 2024 investor presentation, Tokio Marine has set a goal of improving the company’s ROE to 20% in fiscal 2026 or in three years’ time.

I take the view that TKOMY will be able to expand its ROE from 15% in FY 2023 to 20% for FY 2026, as there are multiple ROE improvement levers.

One key ROE expansion driver is the reduction of cross-shareholdings, which Tokio Marine refers to as “the sale of business-related equities” in its corporate disclosures.

“Strategic crossholdings between conglomerates” and other companies are a common phenomenon in Japan, as mentioned in Seeking Alpha News’ earlier February 22, 2024 article. In general, these non-core investments tend to be a drag on Japanese companies’ ROEs.

In an investor relations conference held on May 24, 2024, TKOMY disclosed that it had cross-shareholdings or “business-related equities” with a book value of JPY0.4 trillion and a market value of JPY3.5 trillion as of end-FY 2023. This also translated into a business-related equities-to-net assets ratio of above 0.6 times.

Moving forward, Tokio Marine’s target is to sell half of its business-related equities by FY 2026 and completely eliminate its cross-shareholders before the end of FY 2029. This suggests that TKOMY’s business-related equities-to-net assets metric could be lowered to around 0.2 times in three years’ time, based on the company’s internal projections.

The other key ROE improvement lever is the enhancement of shareholder capital return.

At its FY 2023 (company’s definition of fiscal year) analyst briefing on May 20, 2024, Tokio Marine shared that it plans to hike its dividend per share distribution by +29% to JPY159 in FY 2024 and allocate JPY200 billion to share repurchases for the new fiscal year. This means that the stock boasts reasonably decent forward FY 2024 dividend and buyback yields of 2.6% and 1.7%, respectively.

In summary, the decrease in cross-shareholdings and the increase in capital returned to shareholders will shrink TKOMY’s equity base (denominator of ROE equation) and boost its chances of meeting its 20% ROE goal. If I assume a 20% ROE, an 8% Cost of Equity and a 3% Perpetuity Growth Rate, Tokio Marine’s target P/B multiple as per the Gordon Growth Model is 3.4 times, or 42% above its current P/B ratio of 2.4 times.

Variant View

Tokio Marine’s shares might not experience a positive valuation re-rating if its ROE doesn’t improve.

One scenario is that Tokio Marine’s equity base doesn’t shrink that much due to a lower-than-expected level of buybacks and a smaller-than-expected amount of cross-shareholdings reduction.

Another scenario is that TKOMY’s future earnings (numerator for ROE equation) decline significantly, which more than offsets the shrinkage of the equity base (denominator for ROE equation) through capital return and the sale of business equities.

Final Thoughts

Tokio Marine is currently trading at a discount to its peers based on the P/B valuation metric. My view is that the stock’s P/B ratio can expand from the current 2.4 times to 3.4 times in the future, with an increase in its ROE from 15% in FY 2023 to 20% in FY 2026. This explains why I have rated TKOMY as a Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here