One of the commodities that I’m very bullish on is uranium. As explained in this article, the yellow metal should be quite resistant to recession as it’s demand is pretty price inelastic. However, most uranium miners are still exploring/developing their projects and are years away from production. One of the few exceptions is Ur-Energy (NYSE:URG) as I’ve written in my previous article about the company. Since then, the company has released its Q2’23 results, presenting valuable insights as to how the ramp-up is going as well as some pricing guidance on the contracted pounds after 2023. Overall, URG seems to be one of the less risky bets on uranium equities, as it has already began producing pounds and is based in a safe jurisdiction. In light of this, I maintain my bullish stance on the company.

Q2’23 overview

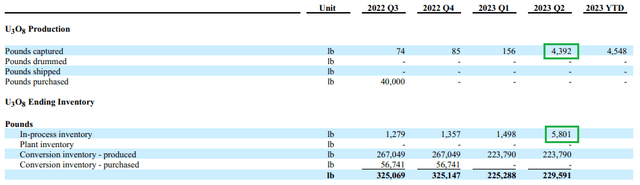

Q2’23 was entirely market by URG’s efforts towards ramping up production. The company didn’t sell any U3O8 during the quarter, as the 100k pounds transaction with the US Department of Energy was completed in the January 2023. Consequently, revenue was only US$39k, consisting of disposal fees. However, expenses grew as URG is expanding its team and ramping up-production. OPEX amounted to US$6M – almost double QoQ and up 74.0% YoY. Commercial production at Lost Creek began to be gradually resumed in May and the company captured 4,392 pounds of U3O8, which were added to inventory in process.

URG’s inventory dynamics (URG)

The ramp-up is now gaining momentum and according to the earnings call, management is targeting production of around 180klbs this year, with the aim to reach 600klbs of annual output next year and eventually increase further as new contracts are being signed:

But again, our goal is not to produce 600,000 this year. Our goal is to produce roughly 180,000 this year. But moving into next year, moving to that 600,000 pound a year range. It’s important for us to get to economies of scale, and that’s why we want to ramp up to that level and continue to move north of that as we were able to sign in additional sales contracts.

– John Cash, CEO of Ur-Energy

In terms of expectations for the remainder of the year, around 180klbs of U3O8 are anticipated to be sold for total proceeds of around US$11.1M. During the earnings call, one more important detail was revealed – the approximate price at which the 600klbs annually, contracted for 2024 and thereafter are to be sold.

We have three multiyear contracts in place with average pricing of about $62 per pound, which will result in revenue of about $220 million. Keep in mind that each contract has a small flex that may result in slightly higher or lower deliveries depending on the buyers’ needs.

– John Cash, CEO of Ur-Energy

It appears that those contracts were signed at significantly above spot prices as the market price was around US$50/lbs at the time the agreements were announced. In addition, this is right around the price assumptions, which URG used in the FS of Lost Creek and Shirley Basin. Now that spot prices have climbed to US$57 per pound, I won’t be surprised any future contracts to be signed at levels towards US$70s/lbs.

Solid financial position

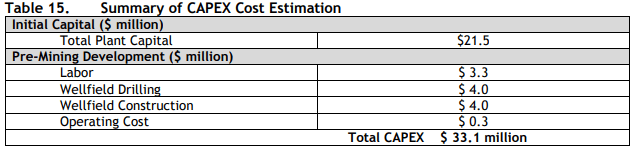

Ur-Energy ended Q2’23 with nearly US$68.0M of cash and equivalents as well as nearly 229.6klbs of inventory, which should be worth approximately US$13.0M at current spot prices. In terms of debt, URG has a little less than US$8.5M of principal outstanding under its state bond loan. This puts the net liquidity position at north of US$70M – enough to meet the US$33.1M of estimated initial capital outlay at Shirley Basin even if some inflation is factored in.

Estimated initial CAPEX at Shirley Basin (Ur-Energy)

Valuation discussion

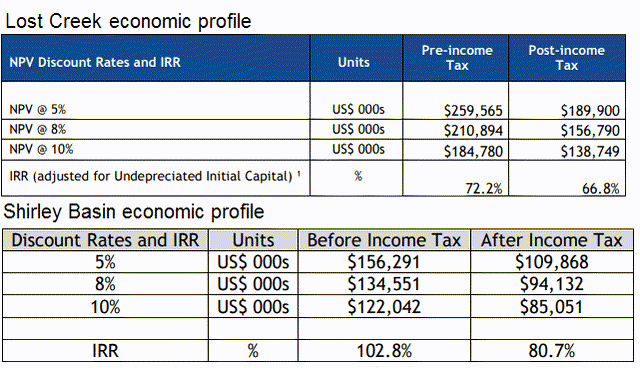

Currently, when considering the net liquidity position of URG, the company is trading at around EV of US$227M, while the combined estimated NPV of Lost Creek and Shirley Basin, discounted at 8% is at around US$251M.

Lost Creek and Shirley Basin economic profiles (Ur-Energy)

While the discount of around 10% of the current EV to the estimated NPV may not seem large enough, there are few factors that make me believe that URG has more upside.

Safe geopolitical profile

URG’s assets are based in the US. The recent events in Niger once again highlighted the importance of political risk. Also, the largest uranium producer – Kazatomprom (KAP:LSE) is also operating in quite tense region, as Kazakhstan has faced riots in 2022. For these reasons, the idea of higher prices for Western origin uranium (as its supply would be considered lower risk) is gaining momentum. This was mentioned also during the earnings call:

So we’re already seeing that bifurcation in the market. And it looks like Western production, U.S. production is worth several dollars a pound more than production from areas that may be exposed to more geopolitical risk. And so we look forward to seeing that more as we go forward.

– John Cash, CEO of Ur-Energy

URG is already producing

Most uranium miners are still developing/exploring their properties, which comes with a plethora of additional risks. Permitting alone, could cause massive delays and push production out a few years, adding uncertainty. This is not the case with URG as Lost Creek is already in production, while Shirley Basin is permitted and construction-ready. URG’s financial position appears more than sufficient to fund the construction of Shirley Basin when such decision is taken. Not the same could be said for the majority of developers/explorers, which have to look for funding at the current environment of rising cost of capital.

Conclusion

Ur-Energy is on track with ramping-up production at Lost Creek and has pretty comfortable financial position, with no risk of dilution in sight. This alone puts the company ahead of most uranium equities as they are years away from production and short on capital. The location of URG’s assets in the US is another advantage, especially in light of the realization of political risk in uranium-rich Niger. Going forwards, the safety of supply may become a factor in pricing, justifying higher prices for Western extracted uranium.

Read the full article here